Dubai real estate: party is over. The sector that was a crowded trade a year ago is now steadily moving into distressed territory.

Dubai real estate: party is over. The sector that was a crowded trade a year ago is now steadily moving into distressed territory.

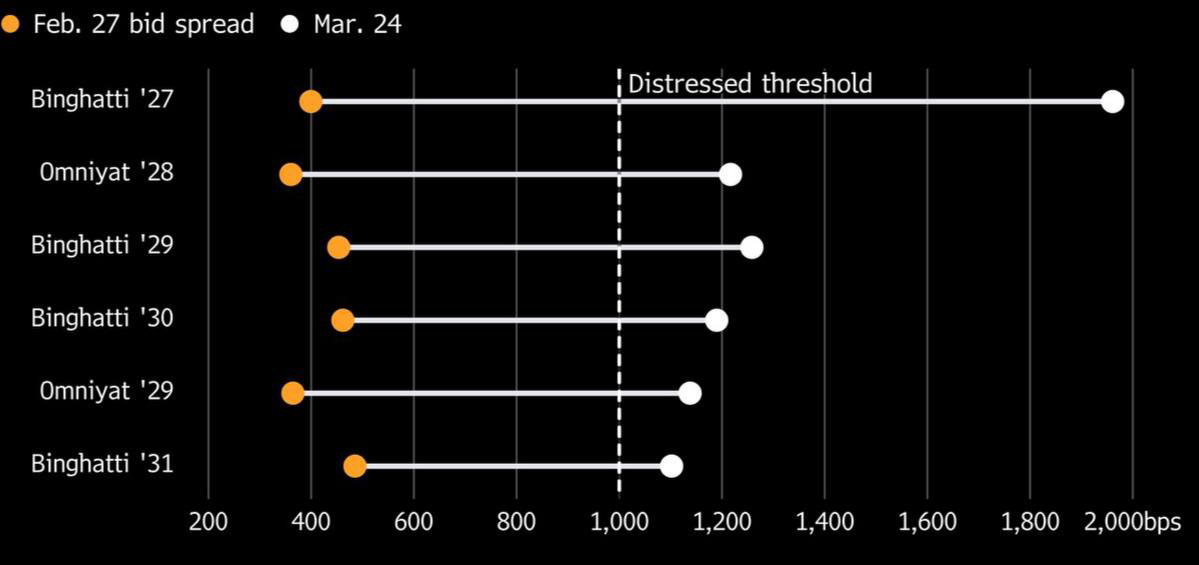

Six dollar sukuk issuances from Binghatti and Omniyat are trading with a spread above 1,000 bps to the risk-free rate. This is a deep stress marker. The market is pricing not just geopolitics, but systemic credit quality risk.

Key points on the setup:

🔻Refinancing Risks. This is the main pain point. The primary market for the region is effectively closed due to escalation. Developers have become accustomed to living in conditions of infinite liquidity expansion, but now they have hit a wall of maturities worth $8 billion until 2030. If you can't refinance, your sales in Dubai don’t matter.

🔻Sub-investment grade under scrutiny. Spreads for Sobha and Arada have already soared to 700–800 bps. This is classic contagion. Hedge funds have aggressively entered short-selling, understanding that local buyers will not be able to maintain levels in such an external environment.

🔻Narrative vs Reality. Developers' statements about 'stable sales' and 'zero cancellations' are damage control. For institutions, operational performance is not as important as access to capital. Fitch has already placed ratings on review (Rating Watch Negative). This is a signal to exit for those still in high-yield positions.

The situation looks like an asymmetric downside. Even if the conflict calms down, the risk premium in the region has already been recalibrated and will not return to early 2024 levels in the coming quarters. Real estate bonds in the UAE have ceased to be a 'safe haven.'