Most of the time when people talk about Central Bank Digital Currencies they sound far away. You hear about banks and pilot programs and policy frameworks and it all sounds very important but it is hard to understand. It is like something is being built at the top of the system away from how people actually use money every day. There is always this gap between the institutions that design the system and the individuals who are supposed to use it.

That gap is where things usually get complicated.

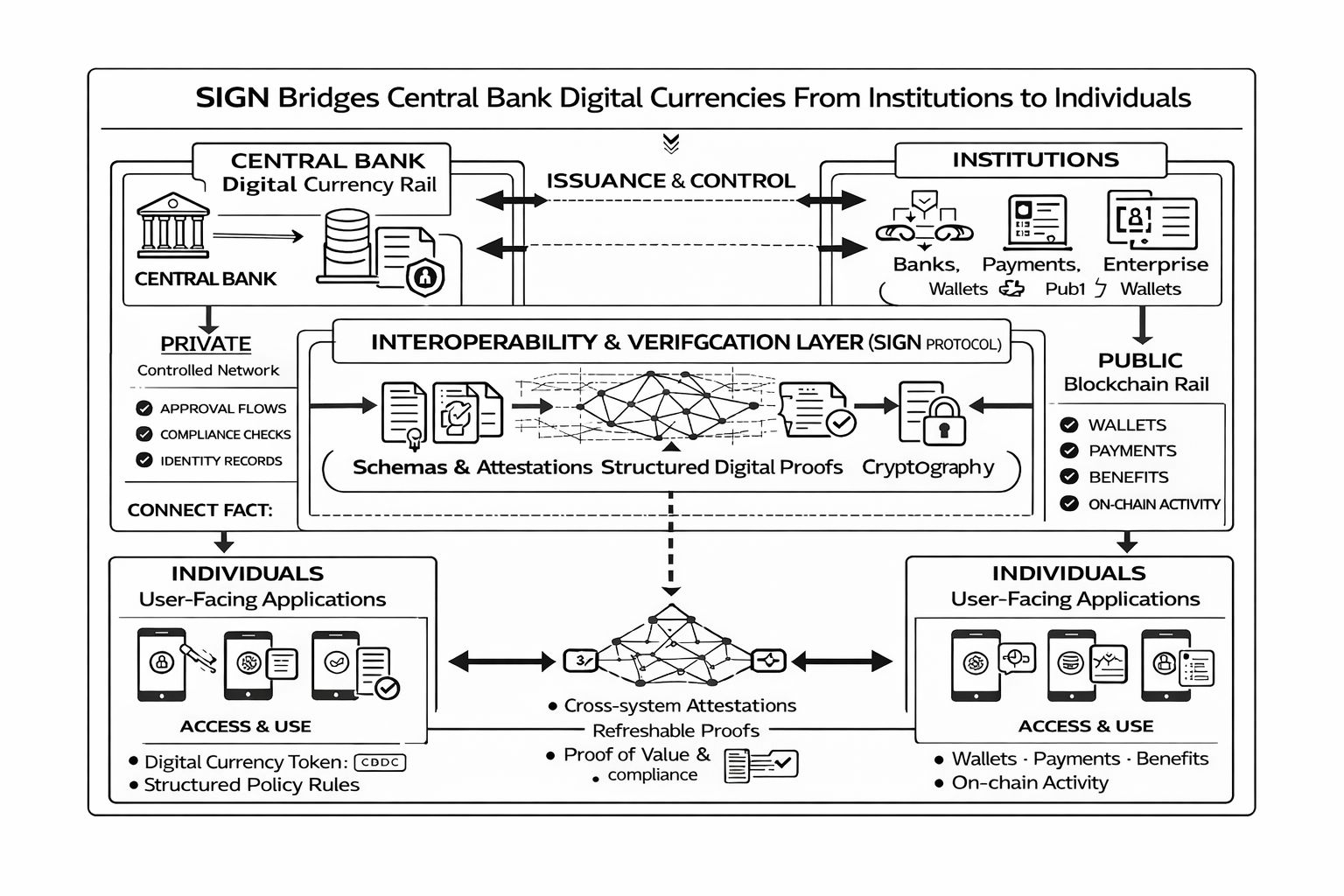

Because Central Bank Digital Currencies at their core are not just money. They are systems of control and distribution and verification that are backed by the state. A Central Bank Digital Currency is a liability of a central bank it is essentially digital cash issued by the state, not a private company.. Even if the money itself is digital the way it moves still depends on a lot of different layers. There are banks and payment providers and wallets and compliance checks. The infrastructure between when the money's issued and when it is used is where friction builds.

That is the problem.

Most Central Bank Digital Currency designs are strong when it comes to the layer but they are weaker when it comes to how that system connects to individuals in a flexible and verifiable and scalable way. You can issue money but how do you control who gets access under what conditions and with what level of transparency without making the system rigid or overly centralized?

That is where $SIGN starts to fit in but not in the way people usually think.

$SIGN is not trying to replace Central Bank Digital Currencies or compete with them. It positions itself as the layer that sits between parts of the system. More specifically, as a shared evidence and verification layer that connects institutional rails with more open and user-facing environments.

This is where things get interesting.

Because bridging Central Bank Digital Currencies is not about moving money from one place to another. It is about proving that the movement is valid. Who approved it under what rules whether compliance checks were passed and whether the state of that money's still consistent across systems.

SIGN approaches this by turning those steps into records.

Of relying on internal databases or fragmented logs it uses attestations, which are structured and signed proofs that record actions and approvals and conditions in a way that can be checked across systems. That means when value moves from a Central Bank Digital Currency rail to a more public or user-facing layer it does not lose context. The proof travels with it.

You can break this into layers to see where the shift happens.

At the level SIGN acts as an interoperability layer between different money systems. It supports both rails, like blockchains and private rails like permissioned Central Bank Digital Currency environments. The key is that it standardizes how evidence is recorded. Every action, issuance, transfer, approval can be tied to a claim that does not depend on a single system to validate it.

At the developer level this removes a lot of complexity. Instead of building custom bridges that only move value developers can build systems that move value with context. That includes compliance data and identity checks and approval flows and audit trails. It makes -system interaction less about trust and more about verification.

At the user level the change is subtle but important. Of interacting with isolated systems individuals become part of a connected flow. The money they receive is not just transferred it comes with proof of origin and conditions and validity. That matters more when Central Bank Digital Currencies start being used for things like subsidies and benefits and regulated payments, where eligibility and traceability're critical.

Still it is important to step and stay realistic.

Now most Central Bank Digital Currency systems are still in the early stages. Many are being tested in controlled environments and large-scale deployment is slow by design. Globally central banks are still exploring trade-offs around privacy and control and interoperability. SIGN in comparison is building the layer before those systems fully mature.

So the full picture has not played out yet.

The direction is becoming clearer.

Digital money is no longer being built as a system. It is becoming a mix of public rails, institutional control and user access, compliance and flexibility.. In that kind of environment the hardest problem is not issuing money.

It is connecting systems without losing trust.

That is the role SIGN is aiming to play.

Not as the issuer.

Not as the wallet.

As the layer that makes sure everything in between can be verified.

Whether that becomes essential depends on how Central Bank Digital Currencies evolve. If they remain siloed the need is limited.. If they start interacting across systems across borders across different levels of control then something, like this stops being optional.

Starts looking like infrastructure.