The next inflation wave might not start where most people are looking.

It might start early in fertilizer.

While markets focus on interest rates, oil, and geopolitics, a quieter constraint is building underneath: global fertilizer supply.

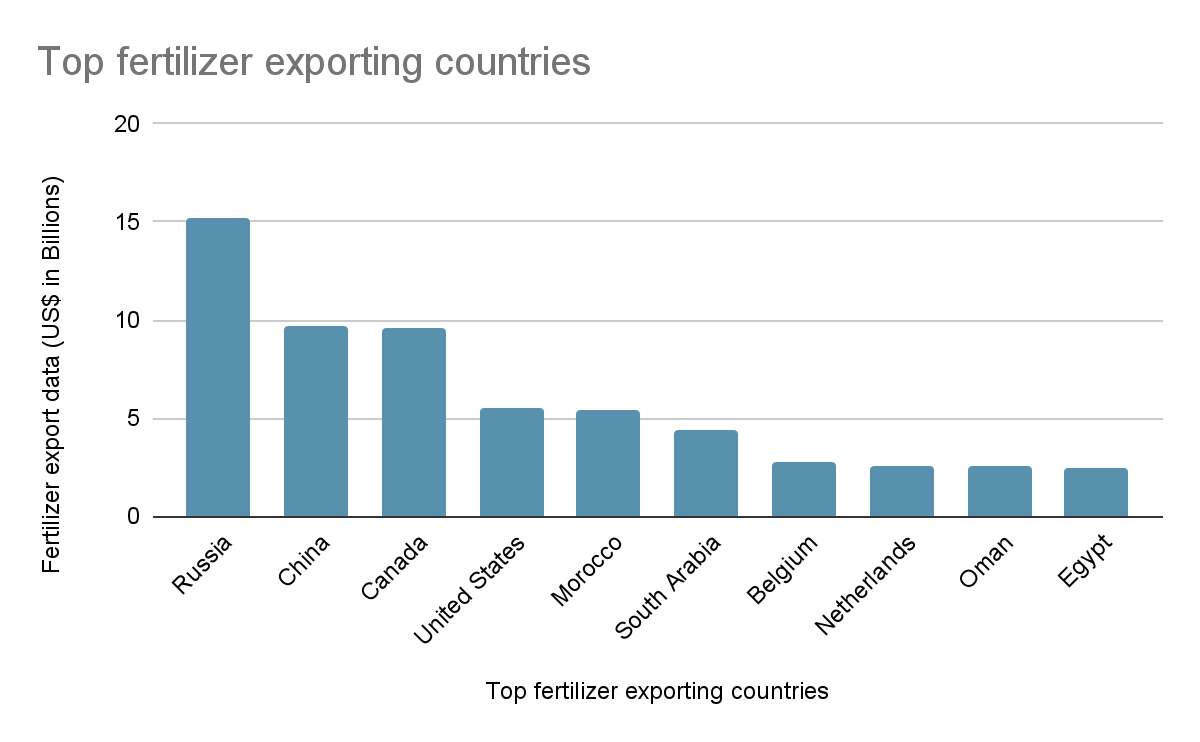

Russia alone accounts for roughly 16.6% of global fertilizer exports, with China contributing another ~10%. Alongside key players like Canada, Morocco, and Saudi Arabia, a relatively small group of countries controls the majority of global supply.

Even more important is what they supply.

Russia, Belarus, and surrounding regions play a major role in exporting critical nutrients like nitrogen, phosphorus, and potash, the building blocks of modern agriculture. In some cases, these regions account for ~18–19% of global nutrient supply.

That concentration matters more than it seems.

Because fertilizer is not optional.

It directly determines crop output.

Studies suggest that without nitrogen fertilizers, crop yields can fall by roughly 12–20%, with certain crops experiencing even sharper declines.

That introduces a key dynamic.

This is not a linear system.

A 10% disruption in supply does not mean a 10% drop in output. It can translate into double-digit declines in yields, depending on how and when shortages hit.

And timing is everything.

Fertilizer demand is seasonal. If supply disruptions coincide with planting cycles, farmers do not get a second chance to correct it later.

Which means the real impact does not show up immediately in markets.

It shows up months later, in reduced harvests, tighter supply, and eventually higher food prices.

By then, the cause is no longer obvious.

Prices rise. Headlines follow.

But the trigger was already set in motion earlier.

Another layer to this is how inflation is experienced globally.

Food carries a meaningful weight in inflation baskets worldwide, lower in developed economies, but significantly higher in emerging markets where it dominates household spending.

So even moderate supply shocks can have outsized real-world impact, especially in regions that are most sensitive to food price changes.

This is where second-order effects begin to matter.

Higher food prices lead to increased pressure on household spending, which shifts monetary policy expectations and triggers broader macro reactions across markets.

All originating from something most people are not watching.

Fertilizer.

Markets often react to what is visible.

But the more important signals are usually quieter, building in supply chains, logistics, and inputs long before they show up in price charts.

This might be one of those signals.

Not immediate. Not obvious.

But potentially shaping the next phase of inflation.

#Inflation #SupplyChain #globaleconomy