New investors entering the market, unable to understand company financial reports and technical analysis, and uninterested in stable low-return assets such as government bonds, money market funds, and bonds, choose stock funds as a way to earn high returns easily.

However, this investment behavior seems extremely foolish to me.

First, we must understand that the interests of fund companies and their clients are not aligned. When you purchase a product from a fund company, you hand over your money for them to manage, believing that as a customer, they have an obligation to make you money. In name, it is like this, but in reality, you are merely a source of profit for them, as the bulk of the fund company's profits comes from management fees.

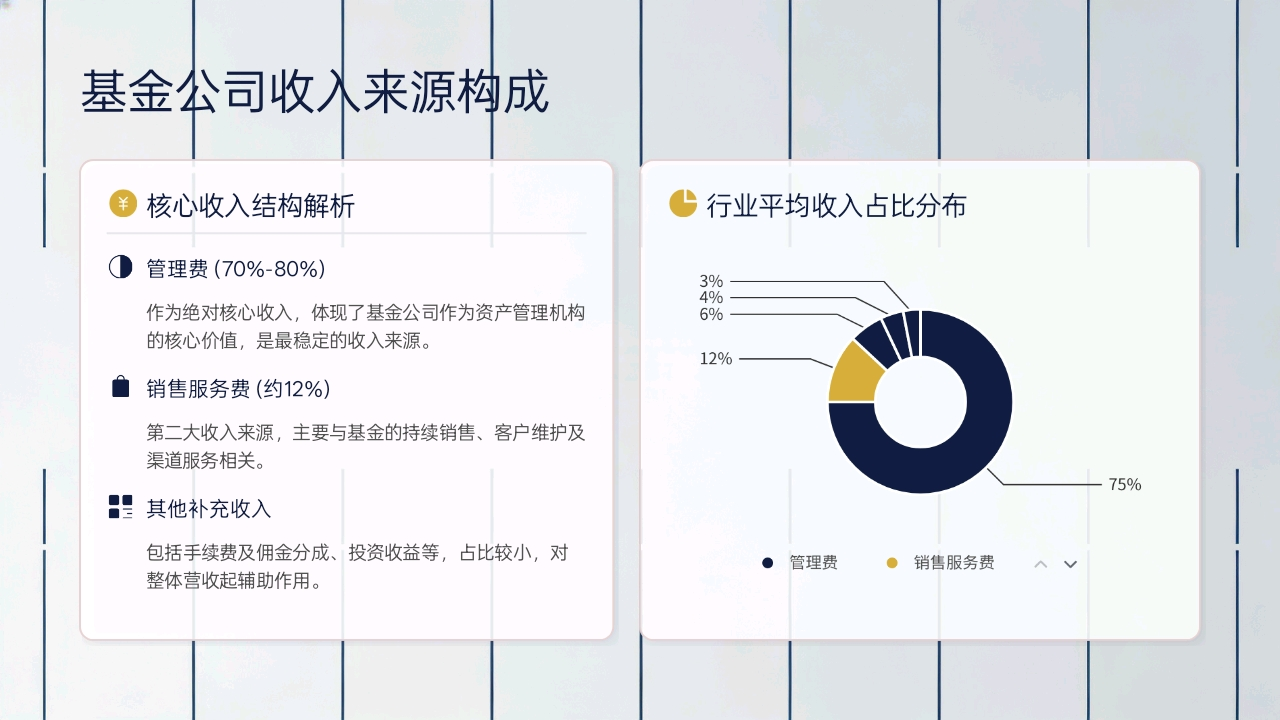

Domestic public mutual fund company income is primarily from management fees (about 70%-80%), followed by sales service fees (about 10%-15%), along with handling fees and commissions, investment income, and others, totaling about 5%-20%. - This is data from China Economic Net.

The following is the typical structure and details of the industry from 2023 to 2025:

Core income ratio (industry average)

Management fee: It is the most stable source of income for mutual fund companies; it is accrued daily based on the net asset value of the fund. The more products the fund company sells and the larger the market value, the more profit they receive, and it is a guaranteed profit. Regardless of the fluctuations in the fund's net value, the holders must pay this fee.

Sales service fee: accounting for 10%-15% of the mutual fund company's income, mainly Class C shares, which means that the money you invest in the mutual fund project has not yet compounded interest but has already been partially taken by the fund company to give to the sales end. Due to the different project standards and fee structures of various fund companies, one-time fees: subscription fees for newly issued funds usually go to the sales end; initial commission is approximately 0.2%-0.5% of the raised amount, reaching up to 1% in bear markets or strong channels; trailing commissions are paid from the management fee based on the retained amount; sales service fees are accrued based on the fund's net asset value, running parallel to management fees. Differences: scale, channel, and product type affect bargaining power, with equity funds usually higher than ETFs/money market funds; bank channels account for a higher proportion, making it difficult to accurately judge specific expenditures due to different chosen channels, but you can't escape this cost.

The average value is approximately: management fee 1.2%/year, trailing commission ratio 30%, resulting in a payment of about 0.36%/year at the sales end (within the management fee); if there is a sales service fee of 0.2%/year, the total annual ongoing cost at the sales end is about 0.56%/year.

Of course, there are also handling fees and commissions, which are around 3%-8%. This part includes trading commissions and subscription/redemption fee sharing, fluctuating with the market and trading volume. This means that after paying the first two fees, you still have to pay once more!

Many people may say that mutual fund companies are professionals who understand financial reports and can bring good returns to investors!

Is it really like this?

A well-known pharmaceutical industry fund manager, Ge, managed the Zhong Certain Pharmaceutical Fund, which indeed brought significant returns during the pandemic. However, after the pandemic ended, it has retraced 68% from its peak in 2021, more than halving, and it has not recovered since. If you were standing guard at a high position, how many years would it take for you to break even? And even if the fund retraces, the fees you should pay remain unchanged!

Of course, if you only think it’s about her alone, you can also look at the chip industry’s Cai and the related funds in the liquor industry; the situation is the same, from profits to huge losses, with no exceptions!

Ultimately, these fund managers and fund companies are also people; their investment capabilities may not be extraordinary, but they just happened to ride the wave of industry development. They gain prestige during the boom, and when the boom period ends and returns to calm, they incur no losses, collecting management fees as usual, while investors helplessly watch their accounts shrink.

Munger's core view on actively managed funds can be summarized as: "After deducting management fees and transaction costs, most actively managed funds do not perform as well as index funds; a 2% annual fee can eat away nearly half of the returns over the long term. This is simply legal robbery." "Moreover, they can’t even outperform the S&P 500 index fund."

Investing your funds in the stock market is like giving your money to others to develop; this process itself is risky. Giving your money to a mutual fund company is essentially entrusting your money to an intermediary, who then gives your money to others while ensuring that they do not have insider trading or collude with listed companies, fully responsible for your own money. Do you think this is reliable?