Introduction: The Paradox of Monetary Value

A green piece of paper, costing less than 10 cents to produce, can exchange for goods and services worldwide. This is the paradox of the modern monetary system.

When discussing stablecoins, we must first answer a more fundamental question: Why can a piece of paper become a global reserve currency? Why is the dollar accepted worldwide, even though it has no intrinsic commodity value?

To understand why stablecoins have value, we must first understand why the US dollar has value. Because stablecoins—especially dollar-pegged stablecoins—are essentially replicating and extending the credit mechanism of the US dollar on the blockchain. Understanding the foundation of the dollar's value is not only crucial for grasping the modern monetary system, but also the starting point for comprehending the value logic of stablecoins.

The forms of currency used by humanity have roughly gone through three stages: commodity money (such as shells and grain), metallic money (such as gold coins and silver coins), and credit money (such as paper money and digital currency). Each evolution represents a redefinition of the source of currency value. The dollar is a typical representative of credit money, its value foundation has completely detached from the constraints of the physical world, and is instead built on social consensus and institutions.

When the scale of economic activity surpasses the supply constraints of physical currency, human society must seek more flexible value carriers. Credit money emerged, replacing 'weight' with 'trust' and 'scarcity' with 'institution'.

However, trust is neither free nor eternal. The dollar's ability to maintain its global status relies on a complex credit support system. Understanding this system is key to grasping the operational logic of the modern monetary system and to understanding how stablecoins rebuild trust mechanisms in the digital world.

So, how is this credit support system established? It needs to start from the essence of fiat currency.

The essence of fiat currency and the trust mechanism

The source of currency value has three levels: commodity value, exchange value, and credit value. As a fiat currency, the dollar has completely detached from commodity value and is entirely based on credit value. This represents a significant turning point in the history of currency evolution.

The history of currency evolution is a continuous process of abstraction of 'value carriers'. Early forms of currency, such as shells, grains, and livestock, were both currency and actual usable goods. With the advent of gold, silver, and other precious metals, though they also had industrial uses, their value as currency mainly came from scarcity and divisibility. Moving to paper money and digital currency, the currency itself has almost no commodity value; its value entirely relies on the issuer's credit.

The historical trajectory of the dollar is a microcosm of this evolutionary process.

From 1879 to 1933, the dollar was fixed to gold, with 1 ounce of gold equaling 20.67 dollars, its value still having gold as physical support.

From 1944 to 1971, the Bretton Woods system was established, linking the dollar to gold (35 dollars = 1 ounce of gold), with other currencies linked to the dollar, making the dollar the center of the global monetary system, while gold remained the ultimate anchor.

Since 1971, after Nixon closed the gold window, the dollar has completely decoupled from gold, and its value is entirely based on credit without any physical backing.

Interestingly, although the modern monetary system has entered the era of fiat currency, historical inertia still leaves a deep imprint in institutional design. Under the Bretton Woods system, global monetary authorities held large gold reserves, a phenomenon referred to as the 'Bretton Woods Gold Mystery'. At that time, apart from the U.S., other countries had no legal obligation to hold gold, yet central banks still showed a strong inclination to hold gold. This behavior is driven by the institutional memory and enduring habits of central bankers, reflecting a primitive trust in physical assets inherited from the gold standard era.

The core of credit money is 'trust', but trust is not unconditional. It requires a mechanism to establish and maintain it: legal enforcement is the foundation, institutional guarantees provide reliability, historical performance reinforces trust, and network effects create a positive feedback loop.

For the dollar, this trust has surpassed the legal enforcement of a single country and expanded to the global market. As a global reserve currency, the dollar has gained global trust. This trust is the foundation of dollar hegemony and is key to understanding the value logic of stablecoins.

The establishment of the dollar's hegemony

The dollar's status as a global reserve currency was not established overnight, but is a historical process. Understanding this process helps elucidate the source of the dollar's credit and how stablecoins replicate the dollar's credit mechanism in the digital world. This process has not been smooth.

In 1879, the U.S. officially adopted the gold standard, fixing the exchange of dollars to gold. During World War I, European countries consumed large amounts of gold reserves, while the U.S. was the main supplier of war materials, accumulating a significant amount of gold. By the end of the war, the U.S. had become the largest holder of gold in the world.

In July 1944, representatives from 44 countries met in Bretton Woods, New Hampshire, to rebuild the post-war international monetary system. At that time, the United States held about 75% of the world's gold reserves and accounted for more than 50% of global GDP, making it the only country capable of supporting the global monetary system.

The Bretton Woods system established a 'dual peg' mechanism: the dollar was pegged to gold (35 dollars = 1 ounce of gold), with the U.S. promising to exchange gold at this price at any time; other currencies were pegged to the dollar, maintaining fixed exchange rates with the dollar. The dual peg mechanism made the dollar the center of the global monetary system, and the dollar became the 'world currency'.

However, the Bretton Woods system has a fundamental structural problem: the Triffin Paradox. In order to provide sufficient liquidity to the world, the U.S. must continuously export dollars and create trade deficits. However, the accumulation of deficits erodes the credibility of the dollar being linked to gold. When the world's trust in the dollar exceeds the supporting capacity of U.S. gold reserves, the system will collapse.

During the Vietnam War, U.S. fiscal deficits increased significantly. The trade deficit continued to expand, leading to a large outflow of dollars. Central banks began to exchange dollars for gold, causing the U.S. gold reserves to decrease rapidly—from about 20,000 tons in 1944 to about 8,000 tons in 1971.

The U.S. must provide sufficient dollar liquidity to the world while maintaining the commitment to exchange dollars for gold. However, these two goals contradict each other in the long term. When the contradiction escalates to an irreconcilable point, the U.S. chose to abandon the gold peg.

On August 15, 1971, President Nixon unilaterally announced the closure of the 'gold window', ceasing the conversion of dollars to gold. This was one of the most important turning points in modern monetary history.

The Nixon Shock marked the first complete 'abandonment of metallic currency' in human history. From that moment on, the dollar—and all major currencies—became purely credit currencies without any physical backing.

After decoupling from gold, the dollar faces a key question: how to maintain global demand for the dollar? Without sufficient demand for dollars, the value of the dollar will collapse.

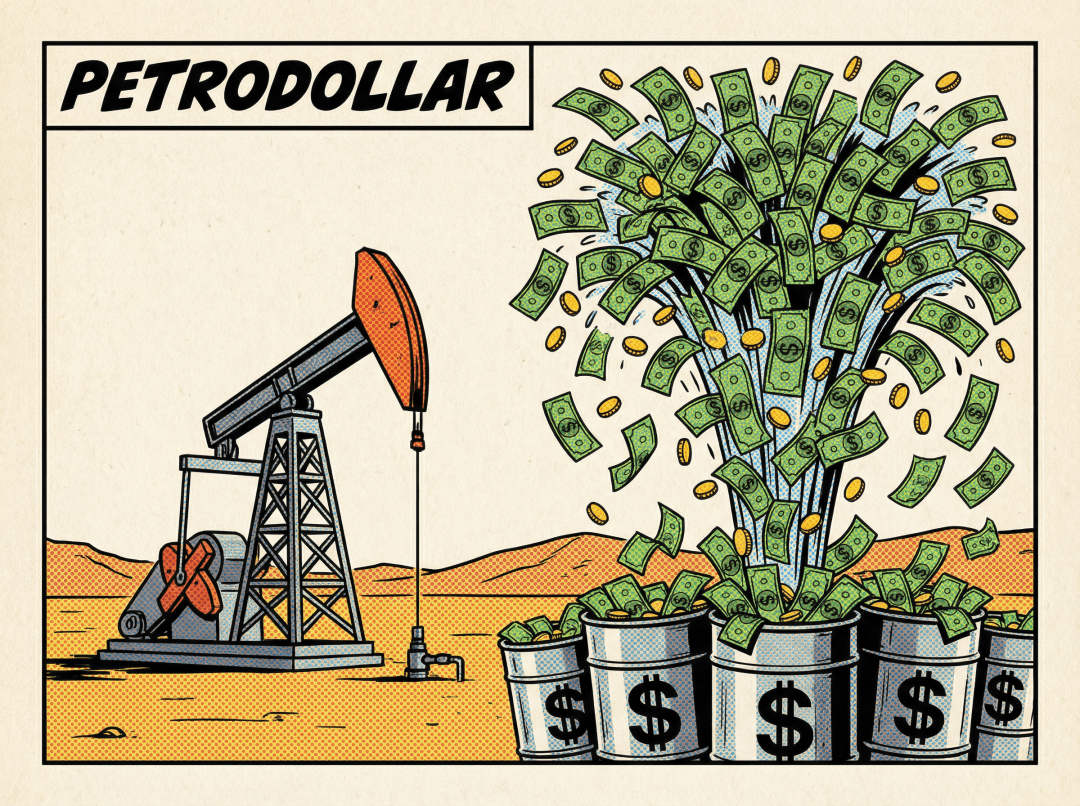

The U.S. found a new anchor: oil. In 1973, OPEC (Organization of the Petroleum Exporting Countries) announced an oil embargo, causing global oil prices to soar. The U.S. seized this opportunity and, in 1974, reached a series of key agreements with Saudi Arabia: oil trade must be settled in dollars.

The petrodollar cycle mechanism works like this: countries need to use dollars to purchase oil; oil-producing countries receive large dollar revenues; these dollars flow back to the U.S. to buy U.S. Treasuries and other financial assets.

The U.S. uses these funds to maintain a global military presence and financial system. This cycle creates stable demand for the dollar.

The petrodollar mechanism tightly binds the value of the dollar to the lifeblood of the human economy—energy. As long as the world needs oil, countries must reserve dollars. Through the petrodollar mechanism, the U.S. has achieved a rigid constraint that forces the demand for its currency to extend from domestic legal enforcement to global economic activities.

The petrodollar system is not just an economic agreement but a product of geopolitical dynamics. The U.S. protects oil-producing countries through military power, and oil-producing countries use dollars for settlement in return. This interdependence reinforces the status of the dollar.

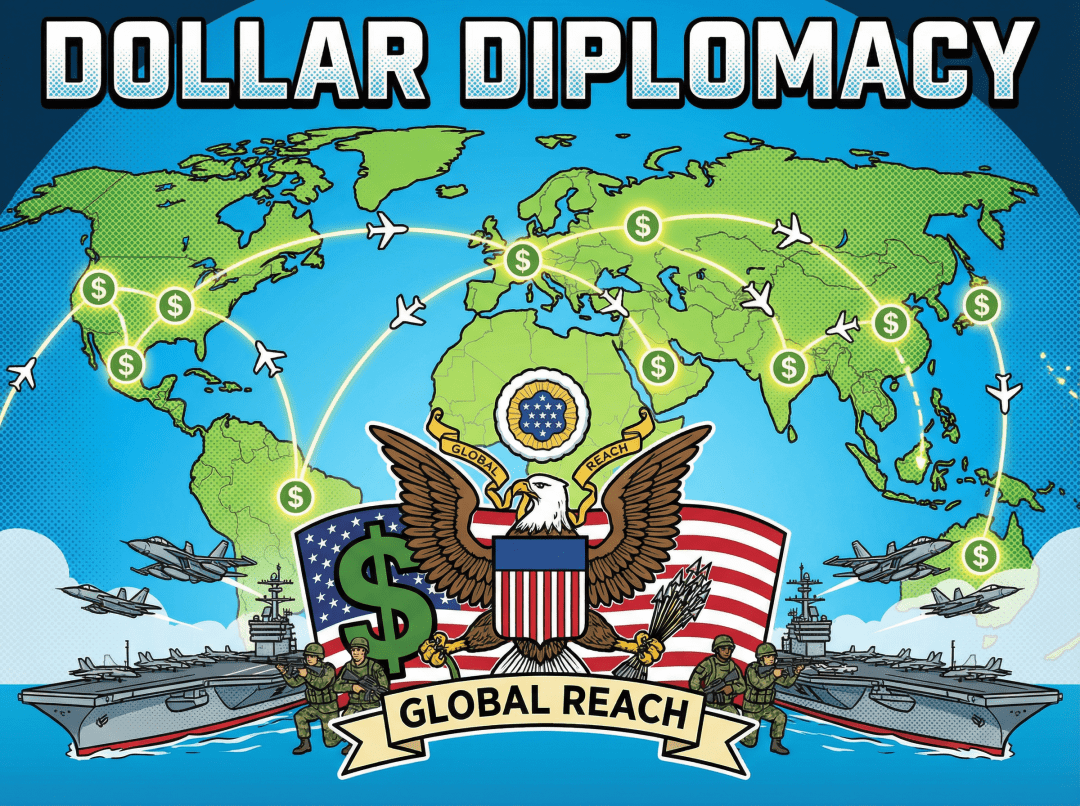

In fact, maintaining dollar hegemony relies on U.S. military power. This is the inevitable logic of the modern international monetary system. The U.S. has 11 aircraft carrier battle groups and military bases in over 140 countries. Military presence not only protects U.S. global interests but also safeguards the dollar-centered global financial system.

The world's most important trade routes—such as the Strait of Malacca, the Strait of Hormuz, and the Suez Canal—are all protected by the U.S. Navy. Military protection ensures the smooth flow of global trade and secures the dollar's status as the trade settlement currency.

Global financial centers like New York, London, and Tokyo, all under the military umbrella of the U.S., allow global capital to gather in these centers and trade using dollars.

The U.S. military deterrent makes any actions challenging the dollar's status face huge risks. Although deterrence is not direct, it indeed provides the final guarantee for the dollar's credit.

The three pillars of dollar credit

The dollar's ability to maintain its status as a global reserve currency relies on a complex support system. This system can be summarized in three pillars: government credit, economic strength, and financial system. Each pillar is indispensable and together forms the basis of the dollar's credit.

Government credit is the basis of fiat currency value. The credit of the U.S. government is mainly reflected in the U.S. Treasury bond market.

The U.S. Treasury market is the largest and most liquid sovereign bond market in the world, with its total size exceeding $27 trillion by 2024. U.S. Treasuries are not only core reserve assets for countries but also the pricing anchor for global financial markets. Holding dollars grants the right to purchase U.S. Treasuries, thus obtaining relatively stable interest income and extremely high asset security.

The U.S. system of checks and balances, rule of law tradition, and democratic elections provide institutional guarantees for government credit. Although political battles are intense, the institutional framework remains relatively stable, which gives the international community confidence in the long-term debt repayment ability of the U.S. government. Although the U.S. has historically suspended gold convertibility, it has never truly defaulted on its debts. Historical records reinforce the market consensus on the dollar as a 'risk-free asset'.

The U.S. rule of law tradition, especially the protection of private property rights, encourages global capital to invest in the U.S. and transact in dollars. Capital believes that property rights in the U.S. will be legally protected. The depth and liquidity of the U.S. Treasury bond market are important supports for the dollar as a global reserve currency.

Economic strength is the material foundation of currency credit. The stronger the economy, the more stable the currency's credit.

The U.S. GDP accounts for about 25% of the global economy; although the share is declining, it remains the largest single economy in the world. Economic scale provides the dollar with vast usage scenarios and value support.

Silicon Valley tech companies and Wall Street financial institutions represent the forefront of global technological and financial innovation. The dollar is not only a means of payment but also the settlement language of technological and financial innovation. The U.S. has a global leading advantage in key industries like technology, finance, and defense, which not only creates huge economic value but also positions the U.S. in a key role in the global supply chain, reinforcing the status of the dollar.

The U.S. economy has shown strong resilience in various crises. After the 2008 financial crisis, the U.S. economy was the first to recover; after the pandemic hit in 2020, the U.S. economy also demonstrated strong resilience. Economic resilience gives the market confidence in the long-term value of the dollar. Economic strength and innovation networks provide continuous value support for the dollar.

The hegemonic status of the dollar depends not only on 'who is using it' but also on 'how it circulates'. The U.S. has built an extremely efficient and hard-to-surpass financial infrastructure.

SWIFT, as a messaging platform, connects over 11,000 financial institutions globally and is the core of global financial communication standards and cross-border payment instruction transmission. CHIPS, as a private clearing system, processes an average daily value of $1.9 trillion, providing an extremely high liquidity efficiency of 29:1 in dollar cross-border clearing. Fedwire is a real-time gross settlement system of the central bank, processing an average daily value of $4.5 trillion, providing immediate finality for large payments.

SWIFT's statistics for 2025 show that the dollar's share in global payments remains above 47%, and in international payments that exclude intra-Eurozone transactions, it reaches as high as 58.8%. The extremely high network effects create strong path dependence: switching to another currency requires not only changing the pricing system but also rebuilding a matching clearing network with equivalent efficiency.

New York is the largest financial center in the world, with the deepest capital market. Global capital gathers, trades, and allocates here, with the dollar being the foundational currency. The Federal Reserve's monetary policy not only impacts the U.S. economy but also influences the global economy. When the Fed raises or lowers interest rates, global capital flows are affected, making the dollar the benchmark for global asset pricing.

The U.S. possesses the deepest and broadest financial market in the world. From stocks, bonds, to derivatives and commodity futures, a wide variety of financial products are available. The depth of products allows holders of dollars to invest in various assets and obtain returns, further reinforcing the dollar's value. The depth and breadth of financial infrastructure create a competitive advantage that makes the dollar difficult to replace.

In addition to these three pillars, military power is the invisible guarantee of the dollar's credit. Although it is not a direct source of credit, it provides security for the other three pillars: protecting global trade routes, ensuring the smooth circulation of the dollar as a trade settlement currency; safeguarding financial centers to provide a secure environment for global capital; and providing deterrence, making any actions challenging the dollar's status face huge risks.

The deeper logic of fiat currency value: network effects and path dependence

The three pillars of dollar credit explain why the dollar has value, but the deeper logic of fiat currency value goes beyond this. This logic can also explain why stablecoins—digital extensions of the dollar—have value.

The core of currency value is 'acceptance'. The more people accept a currency, the higher its value. This is the source of network effects.

When a currency is used by more people, the number of goods and services that can be purchased with that currency increases, enhancing the currency's practicality. The stronger the practicality, the more people are willing to use it, forming a positive feedback loop.

Once a currency becomes the dominant currency, it is difficult to replace. This is because conversion costs are high: changing the pricing system, updating the payment system, and rebuilding trust. Path dependence further solidifies the status of the dominant currency.

Switching from the dollar to another currency incurs huge conversion costs. This includes not only technological costs (updating systems) but also learning costs (understanding new currencies) and risk costs (uncertainties of new currencies). Conversion costs lead the market to prefer continuing to use the dollar.

As the global reserve currency, the dollar has formed a strong network effect. Over 80% of international trade is settled in dollars, and over 60% of foreign exchange reserves are in dollars. Network effects and path dependence make the dollar's status difficult to shake.

Of course, maintaining dollar hegemony is not free; the U.S. must bear enormous costs. U.S. military spending accounts for about 40% of global military expenditures, exceeding $700 billion annually. A significant portion of this spending is used to protect global trade routes and financial centers, providing security for dollar hegemony.

To provide the world with dollar liquidity, the U.S. must continuously create trade deficits. The U.S. needs to exchange real goods and services for dollars held by other countries. The 'deficit' is essentially the cost of maintaining dollar hegemony.

Maintaining financial infrastructure like Wall Street and clearing systems requires substantial investment. These investments ensure the efficient circulation of the dollar but also entail ongoing costs.

Although these costs are enormous, they are still worthwhile compared to the benefits brought by dollar hegemony (such as seigniorage and financial dominance). This also explains why the U.S. is willing to bear these costs to maintain the dollar's status.

However, dollar hegemony faces new challenges: the demand for currency in the digital world. As global economic activities increasingly occur on the blockchain, how can the dollar maintain its status in the digital world? The answer is stablecoins.

Stablecoins: The expansion of dollar credit in the digital dimension

Understanding the dollar's value foundation clarifies how stablecoins replicate and extend this credit mechanism in the digital world. In the blockchain ecosystem, stablecoins play a key role in completing the currency loop of the crypto economy. They typically anchor to the dollar at a 1:1 ratio, bringing the credit value of traditional dollars into the digital world. As of November 2025, the global circulation of stablecoins has reached approximately $304.36 billion, becoming an important cornerstone supporting daily settlement.

Stablecoins are not merely digital tokens; they are digital extensions of dollar credit. When users hold USDT or USDC, they are holding a form of 'on-chain dollar debt', whose value is supported by the dollar collateral held by the issuer.

To maintain a stable 1:1 exchange rate, leading stablecoin issuers have established extremely robust balance sheets, primarily composed of high-quality liquid assets. Tether's total exposure to U.S. Treasuries in Q3 2025 was approximately $135 billion, along with about $9.9 billion in Bitcoin and approximately $12.9 billion in precious metals (gold), with excess reserves of about $6.8 billion, maintaining over 1:1 sufficient collateral. Circle's total exposure to U.S. Treasuries in November 2025 was approximately $68.2 billion (including repos), with cash and deposits of about $9.6 billion (held in systemically important banks), and reverse repos of about $49.7 billion, maintaining over 1:1 sufficient collateral.

Tether's report for Q3 2025 shows that its exposure to U.S. Treasuries has made it the 17th largest holder of U.S. debt globally, surpassing sovereign nations like South Korea. Circle, on the other hand, shows a stronger compliance tendency, placing most of its reserves in regulated overnight reverse repurchase agreements and top bank deposits.

These robust reserve assets enable stablecoins to rapidly penetrate the cross-border payment market. The traditional agency model has structural inefficiencies, which stablecoins effectively address.

Traditional SWIFT cross-border remittances typically take 1 to 5 working days and involve multi-level agency account verifications. In contrast, stablecoin transfers based on Solana or Ethereum Layer 2 can be completed in seconds to minutes, providing 24/7 service. In traditional cross-border payments, intermediary fees, exchange rate spreads, and operational costs often total 3% to 5% of the transaction amount, with small remittances being even higher. On-chain fees for stablecoin transfers are often negligible (as low as $0.01 on Solana), and the overall cost can usually be reduced by more than 70%.

Every stablecoin transfer is traceable on-chain, eliminating the uncertainty of 'funds in transit'. At the same time, automatic settlement, custody, and conditional payments achieved through smart contracts provide unprecedented flexibility for corporate financial management.

The mark of stablecoins moving from the margins to the mainstream is the improvement of the regulatory framework. In 2025, the United States passed the (GENIUS Act) (Payment Stablecoin Act), which fundamentally changed the game rules of the industry.

The legislation stipulates that compliant payment stablecoin issuers must maintain a 1:1 reserve, with reserve assets strictly limited to U.S. Treasuries, physical cash, custodial deposits, specific repurchase agreements, and Federal Reserve reserve requirements.

The regulatory framework has brought stablecoin issuers into the category of 'narrow banks', enhancing the robustness of the system.

As the rules became clearer, traditional financial institutions began to enter the market on a large scale. By 2025, about 80% of jurisdictions around the world had announced new digital asset plans, and financial institutions began to view public blockchains as compliant settlement layers.

Stablecoins are no longer seen as a threat to financial stability, but as a tool to maintain the influence of the dollar. By locking stablecoin reserves in U.S. Treasuries, the U.S. government has created new rigid demand for U.S. debt globally through the private sector.

Behind this lies a deeper issue. In the era of pure credit money, the Triffin Paradox evolves into 'Triffin 2.0': the global demand for collateral 'safe assets' (mainly U.S. Treasuries) grows far beyond the U.S. economy's ability to provide these assets without jeopardizing fiscal sustainability. The rise of stablecoins has alleviated this contradiction to some extent.

Stablecoin issuers are 'non-discretionary' buyers of U.S. Treasuries, providing stable demand for short-term government bonds. According to a speech by Federal Reserve officials in November 2025, stablecoins have reduced the U.S. government's financing costs by attracting non-U.S. buyers. By the end of 2024, stablecoin issuers held about $166 billion in U.S. Treasuries, which is expected to reach $250 billion to $500 billion by the end of 2025, becoming important marginal buyers of short-term U.S. debt.

In contrast, major central bank reserves amount to about $7.5 trillion, remaining relatively stable or slightly decreasing, serving as long-term reserve assets with limited contributions to short-term liquidity. Money market funds total about $6 trillion, continually growing and competing with stablecoins in short-term instruments.

Under the stablecoin mechanism, stablecoins are not just currency; they have become digital circulation tools for U.S. Treasuries, greatly improving the turnover efficiency of U.S. debt as global collateral.

Conclusion: From a piece of paper to a string of code

Returning to the paradox at the beginning: a green piece of paper, with a production cost of less than 10 cents, can exchange for goods and services from around the world. The answer is 'acceptance'.

The value of the dollar comes from 'acceptance', not from commodity value. When the whole world accepts the dollar, it has value. This acceptance is built on the three pillars of government credit, economic strength, and financial system, gradually established through historical processes, and maintained through network effects and path dependence.

The value of stablecoins also comes from 'acceptance'. Dollar-pegged stablecoins (like USDT and USDC) replicate the credit mechanism of the dollar on the blockchain. They inherit the dollar's credit value by anchoring to dollar assets at a 1:1 ratio. When we hold USDT, we hold 'on-chain dollars', whose value comes from the dollar's credit foundation.

However, stablecoins are not just a simple copy of the dollar. Through blockchain technology, stablecoins achieve a more efficient circulation method: 24/7 operation, seamless cross-border transactions, low fees, and peer-to-peer transfer. The technological advantages give stablecoins unique value in the digital world.

The value of the dollar has shifted from a physical anchor (gold) to a geopolitical anchor (oil), and now to today's technological anchor (stablecoins and on-chain credit). The compliance of stablecoins in 2025 marks the dollar's transformation from a sovereign tool to a global digital public good.

Ultimately, if we do not understand why a piece of paper can become a global reserve currency, we cannot truly understand why a string of code (stablecoins) can carry value in the digital world. The logic behind both is interconnected: they are both products of 'trust' and 'acceptance', relying on network effects and path dependence.

In the upcoming articles, we will delve into how stablecoins complete the currency loop of the crypto economy, how they change the global payment landscape, and how they reshape monetary concepts. However, all these discussions are based on one premise: stablecoins are digital extensions of dollar credit, and their value logic is inherited from the dollar.

Understanding this makes the logic of the modern monetary system clear.