Stove chooses to provide a permissionless protocol interface in an open-source, non-profit, zero protocol fee manner to map regulated, real custodial US-listed stocks onto the chain in a 1:1 form.

The stock tokenization market is entering a new evolutionary stage.

After experiencing early explorations centered around trading experiences and product forms, the industry begins to show some more fundamental changes—stock tokens are no longer just viewed as 'assets that can be traded on-chain' but are gradually understood as foundational asset modules that can be repeatedly called, composed, and embedded in higher-level financial structures. The new changes are highly similar to the early DeFi development path from trading to infrastructure.

In fact, the Stove Protocol recently announced by HabitTrade can be regarded as a representative example in this direction. Unlike previous solutions centered around platforms or single products, Stove chooses to provide a permissionless protocol interface in an open-source, non-profit, zero protocol fee manner to map regulated, real custodial US-listed stocks onto the chain in a 1:1 form.

This path does not focus on optimizing a specific trading scenario but attempts to answer a more long-term question: when stocks truly enter the on-chain system, how should they exist to be continuously used in broader financial applications.

To some extent, the emergence of this type of protocol paradigm marks the transition of stock tokenization from past competition centered around 'product forms' to an evolutionary path centered around 'protocol forms'. Under the new structure, stock tokens can be abstracted as verifiable, composable, and extensible foundational asset modules, opening up new spaces for more complex financial applications and cross-protocol collaboration.

The development path and trends of stock tokenization

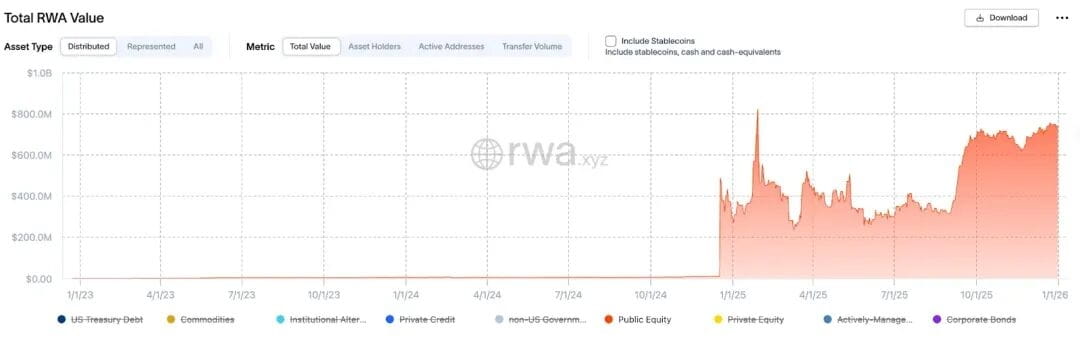

Stock tokenization is becoming one of the most significant sub-directions of growth in the RWA track by 2025. Since the end of 2024, this field has entered a rapid expansion phase, with data from rwa.xyz showing that the scale of related assets has grown from nearly zero to about $780 million, reflecting the accelerating market demand to bring publicly traded company equity into the on-chain system.

Structurally, the core of stock tokenization lies in the 1:1 mapping of real assets, transforming traditional publicly listed company stocks into a digital asset form that can continuously exist and circulate on-chain, enabling 24/7 operation and global accessibility, introducing a scarce and stable real credit anchor into the crypto ecosystem, and providing a more certain value foundation for DeFi.

Although stock tokenization is not a new concept—after DeFi Summer, projects like Synthetix and Mirror have provided stock price exposure on-chain through synthetic asset models, and centralized platforms like FTX have also explored tokenized US stock trading—these early models essentially remained at the level of 'price exposure', neither corresponding to the holding and custody of real stocks nor providing legal or economic control over the underlying assets, exposing systemic risks in the event of oracle failures, collateral volatility, or extreme market conditions, thereby limiting their expansion to a broader user and institutional level.

Real asset support has become the core of this round of growth.

In this market cycle, the significant growth of stock tokenization fundamentally stems from a paradigm shift: the industry begins with the premise of holding and custody of real stocks off-chain and issues corresponding tokens on-chain at a 1:1 ratio. Compared to earlier solutions that primarily provided 'price exposure', this path supported by real assets establishes a clearer, verifiable correspondence between on-chain tokens and real-world assets, achieving substantial improvements in safety, compliance explicability, and institutional acceptability, laying the foundational conditions for their entry into a broader financial system.

First-generation paradigm: exploratory period

The core significance of the first generation of token stocks is that stocks can be tokenized and circulate on-chain. This phase is more reflected as 'on-chain stock trading products', opening up the imagination for this field.

Structurally, the typical form at this stage is an issuance model led by third-party compliance institutions: the project party does not directly assume the role of a broker but collaborates with licensed securities institutions, allowing the latter to complete the purchase and custody of stocks in the traditional market, subsequently issuing on-chain tokens at a 1:1 ratio, and attempting to support their use across multiple chains or platforms.

xStocks launched by Backed Finance belongs to the practitioners under the above ideas, mapping the corresponding stock rights as on-chain tokens for users to trade or use in combinations through cooperation with compliant brokers such as Alpaca Securities LLC. This model is relatively flexible in structure, but its compliance boundaries and expansion capabilities highly depend on the specific jurisdiction and the regulatory qualifications of the partners.

Second-generation paradigm: compliance and financial structure phase

As the market enters a more realistic expansion phase, the narrative focus of coin stocks begins to shift: from an early emphasis on on-chain trading experience to a gradual shift towards structural designs that are closer to traditional financial operating logic, including clear compliance frameworks, legal relationships, and connectivity with existing securities systems.

At this stage, the first to emerge is a closed-loop solution led by licensed financial institutions. This path is usually covered by brokers or financial platforms for stock trading, custody, and related financial product issuance processes, providing users with trading exposure related to stock prices within a compliance framework. Taking Robinhood's Stock Tokens as an example, it primarily operates in the European market based on the MiFID II regulatory framework, adopting a structure similar to Contracts for Difference (CFDs), where users participate in the economic results formed by price fluctuations, while the stocks held off-chain are mainly used for overall risk management and hedging. This model has clear advantages in regulatory communication and compliance explanations and is also easier to embed in the existing financial system.

Another path comes from structured finance-oriented solutions. For example, Ondo Finance carries securities-like assets through regulated funds or SPVs and tokenizes the corresponding rights or shares into the on-chain. This design emphasizes clarity of legal structure, risk isolation, and institutional acceptability, allowing on-chain assets to connect with traditional asset management systems under compliance.

At the same time, the market is also beginning to see explorations closer to the on-chain native brokerage model. Represented by StableStock, it relies on HabitTrade's real trading and settlement capabilities to attempt a tighter integration of stock trading, custody, and on-chain asset representation under compliance, enabling the on-chain system to more directly bear the execution results of the real securities market.

As the market heat for solutions like StableStock surges, the underlying infrastructure capabilities begin to be re-evaluated. HabitTrade has supported US stock trading with stablecoin settlement since 2021, long establishing a foundational channel between on-chain funds and traditional capital markets, covering key aspects such as trade execution, settlement, and custody. Only after compliance and structured finance became industry consensus did these underlying infrastructure capabilities gradually reveal their long-term strategic value, no longer viewed merely as components serving a single product or short-term traffic.

The second-generation token stock solutions present a relatively consistent feature: as compliance and institutional acceptability significantly improve, their overall structure still mainly revolves around platforms or specific financial products. Stock tokens are more embedded in established systems; their usage boundaries, composition methods, and expansion paths are often limited by the design logic of existing financial structures.

The rapid growth of this stage has fully validated the feasibility of real asset mapping on both technical and compliance levels, but from an overall architecture perspective, most solutions are still in a transitional form. The current path mainly addresses 'how to achieve tokenized expression and fundamental trading under compliance' rather than 'how to allow stocks to exist on-chain as financial foundational assets in the long term.'

In the absence of mature hedging, capital management, and risk transmission mechanisms, the pricing and liquidity of on-chain stocks still struggle to achieve endogeneity with the real market, and their price discovery has not truly anchored on the trading and clearing rhythm of underlying stocks. This creates structural ceilings for related assets when accommodating higher frequency and more complex financial activities.

Even emphasizing '1:1 mapping', the correspondence between on-chain tokens and real stocks still reflects more of a connection in terms of performance and legal aspects rather than a complete integration of financial structures. Assets have been completed on-chain, but the financial structures surrounding assets have not yet migrated synchronously, which is a key threshold that stock tokenization needs to cross for further evolution.

Third-generation paradigm: the turning point of protocolization

As previously analyzed, when stock tokens are still primarily viewed as tradeable targets, without being able to be repeatedly called, collateralized, composed, or used for risk management, their growth potential is inherently limited. To truly bridge the structural gap of 'assets are on-chain, but financial structures are not yet on-chain', stock tokenization requires a set of underlying protocol standards that can be reused.

Under the above constraints, the third-generation token stocks begin to emerge: the industry's focus gradually shifts from 'platform products' to 'public protocols', from 'transaction-oriented' to 'ownership and rights-oriented'. In the new structure, Stove emphasizes the openness of the ecosystem more— the protocol itself does not concentrate participation qualifications among a few institutions or platforms but retains collaboration space for different types of participants, including compliant execution parties, developers, and application protocols.

Therefore, the emergence of Stove is not just an addition of a realization method but more like a paradigm-level turning point signal: stock tokenization is beginning to be seen as a financial infrastructure proposition rather than a design issue of a single crypto product. This aligns closely with the direction that HabitTrade has continued to cultivate since 2021, focusing on underlying capabilities such as compliance execution, settlement, custody, and issuance rather than relying on product models driven by short-term traffic.

If the core question of the first two generations of paradigms was 'how to bring stocks on-chain', then the third-generation path represented by Stove answers a more fundamental question: when stocks truly exist on-chain, how should they exist.

Stove Protocol: Building an open standard for stock tokenization as a public good

As mentioned above, the first two generations of stock tokenization solutions focused more on exploring 'how to make stocks a tradable on-chain product', while Stove Protocol's entry point is clearly more foundational. It attempts to address not just a specific trading experience but also focuses more on two more fundamental questions: whether on-chain users can truly access the real stock assets themselves and whether these assets can be continuously used in broader financial applications.

In Stove's design, real stocks are still purchased and held off-chain by licensed brokers, with on-chain tokens existing merely as programmable representations of corresponding rights, maintaining a 1:1 mapping relationship with real stocks. Unlike previous solutions focused on platforms or products, Stove does not engage in trade matching, does not bear spread risks, nor sets protocol fee rates, but abstracts key capabilities such as minting, redeeming, and settlement into a set of standardized interfaces, opening them up to the entire Web3 ecosystem in an open-source, non-profit manner.

This design means that stock tokens can be repeatedly called by different types of on-chain protocols under compliance. For users, this makes on-chain stocks not just a simple target for buying and selling but capable of truly carrying economic results such as price changes, dividends, and corporate actions; for developers and protocols, it lowers the participation threshold, allowing them to build financial scenarios like lending, composition, or capital management around the same type of stock assets without having to repeatedly solve custody, settlement, and consistency issues.

The system architecture of Stove Protocol

From the results, the core goals of Stove Protocol can be summarized in two points:

Allowing on-chain users to directly trade regulated, real custodial stock assets and ensuring economic results align with off-chain stocks;

By adopting an open protocol approach, lowering the participation threshold for stock tokenization, enabling more applications, protocols, and developers to build stock-related scenarios on a unified standard.

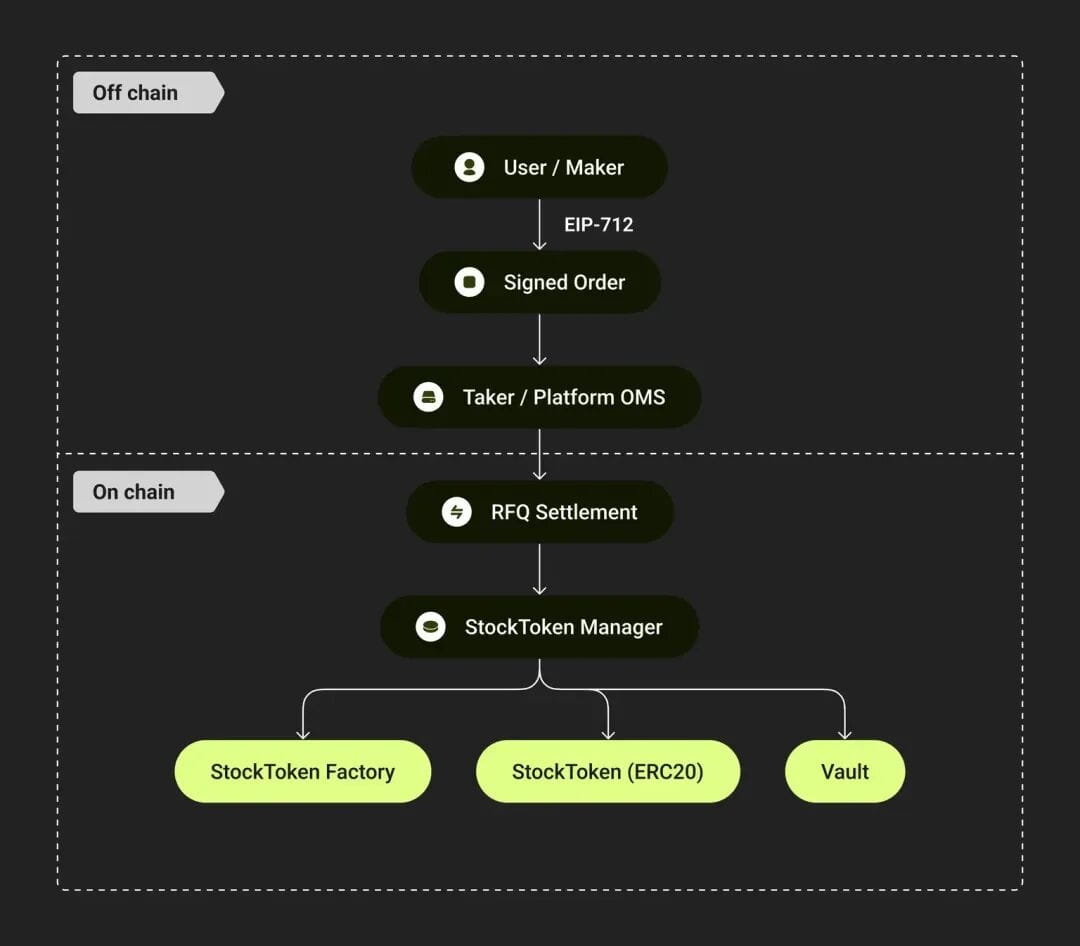

Around this goal, the Stove system did not simply adopt a direct connection model of 'off-chain custody + on-chain issuance' but decomposed stock tokenization into several decoupled yet verifiable key links: trading intentions and real market execution happen off-chain, while asset mapping, settlement, and state recording take place on-chain. The protocol itself does not act as a trading counterparty nor participate in traffic competition but focuses on introducing real securities market execution results to the on-chain system in a verifiable manner.

Precisely because it is not bound to specific platforms or applications, Stove is more like providing a set of reusable foundational standards for stock tokenization. In this positioning, the protocol modularizes and opens up key capabilities such as order settlement, token lifecycle, asset generation, corporate actions, and fund custody through a unified interface, allowing stock tokens to no longer be limited to a specific product form but have the potential to be continually called by different projects.

RFQ Settlement

RFQ Settlement is the core module in Stove Protocol that connects off-chain compliant execution with on-chain asset settlement, used to achieve verifiable and auditable on-chain settlements under the premise that real stocks must be traded and held by licensed institutions.

Since stock trading cannot be directly matched on-chain, Stove does not adopt AMM but introduces the RFQ (Request-for-Quote) model, splitting the trading process into two phases: users generate and sign orders off-chain, expressing verifiable trading intentions; compliant execution parties complete stock buy and sell in the real market and then submit the results to the chain for settlement.

On-chain contracts are responsible for verifying order signatures, parameters, and execution results, triggering the minting or burning of tokens upon successful validation, ensuring that the on-chain asset state always remains consistent with real stock holdings. Trade execution stays off-chain, while settlement and state changes occur on-chain, thus achieving a balance between compliance, gas costs, and transparency.

RFQ Settlement does not participate in matching and does not extract protocol fees; all settlement logic is executed based on deterministic rules, existing merely as a bridge layer for the on-chain system to reliably receive off-chain execution results. This is also a key reason why Stove can adapt to the operational logic of the real stock market while maintaining the attributes of an open protocol.

Token Factory & Manager

StockTokenFactory and StockTokenManager together constitute the asset layer of Stove Protocol, ensuring that stock tokens remain consistent with the real-world status of stocks throughout their entire lifecycle from creation to exit.

We see that in the stock tokenization scenarios, real assets do not exist statically. Events such as listings, stock splits, dividends, code changes, and delistings continue to occur. If these changes cannot be systematically mapped on-chain, '1:1 mapping' can only remain in its initial state and is difficult to establish in the long term. Therefore, Stove explicitly separates the generation logic and operational management of tokens, incorporating the lifecycle of stock tokens into protocol management through a Factory + Manager combination.

StockTokenFactory is responsible for creating deterministic, predictable token instances for each stock. Based on the CREATE2 mechanism, each stock token address can be uniquely derived from parameters such as stock codes and exchanges, allowing external protocols to verify whether a token corresponds to a specific stock asset without trusting third parties, thus avoiding duplicate issuance or hidden replacements. Each token adopts a zero-decimal structure, semantically corresponding directly to 'one share of stock'.

StockTokenManager is responsible for the state consistency of tokens in long-term operation. It uniformly manages token minting and burning, interfacing with RFQ Settlement, executing mint or burn in each legitimate settlement, ensuring that on-chain supply always matches off-chain real positions. At the same time, the Manager is also responsible for mapping corporate actions such as stock splits, dividends, code changes, and delistings onto the chain through standardized processes, constraining key operations through time-lock mechanisms to reduce asymmetrical risks brought by sudden changes.

In this design, each stock token exists within a clearly defined state machine: from normal circulation to triggering corporate actions, to delisting, all key nodes are completed through on-chain calls and leave verifiable records. This provides users with an expected asset end path and delineates clear risk boundaries for external protocols.

Through the combination of StockTokenFactory and StockTokenManager, Stove upgrades stock tokenization from a one-time mapping to a long-term operational, auditable, and reusable asset infrastructure. This also constitutes the core difference between Stove Protocol and most 'stock token products': the former builds a standardized asset layer rather than just a set of token targets for trading.

Corporate Actions module

In the stock tokenization system, what truly determines its long-term establishment, repeated use, and entry into more complex financial scenarios often comes from a premise condition that is easily overlooked: when real-world stocks continue to change, whether the on-chain tokens can still continuously and accurately represent the same asset.

Stock splits, mergers, dividends, code changes, and delistings, among other corporate actions, are completed in collaboration by exchanges, clearing institutions, and brokers within the traditional financial system, which is a prerequisite for stocks to exist as financial assets in the long term. If these changes cannot be systematically mapped onto the chain, the so-called '1:1 mapping' will only hold at the moment of issuance and will gradually become invalid over time, with stock tokens degrading into static certificates rather than sustainable assets.

This is also why in many existing or transitional stock tokenization solutions, corporate actions are often treated as marginal issues—relying on manual operations, centralized announcements, or post-event corrections. This approach may maintain some viability when the scale is still small and the use cases are singular, but once tokens are used for lending, composition, or long-term holding, their uncertainties will be quickly amplified and evolve into systemic risks.

Against this backdrop, Stove Protocol has regarded corporate actions as a core premise that must be positively addressed in stock tokenization since its design inception. The goal of the Corporate Actions module is to ensure that on-chain stocks can maintain consistency with the real-world status of stocks at any point in time, allowing stock tokens the potential for long-term existence and repeated use.

Under this module, key corporate actions such as stock splits, mergers, cash dividends, code changes, and delistings are all included in the unified processing flow of the protocol and strictly correspond with the execution and clearing results of brokers in the real market. Whether it is an adjustment to the number of holdings or the distribution of economic benefits, the results can be clearly reflected on-chain rather than relying on manual interpretations or platform credits.

To prioritize state consistency, the Corporate Actions module requires that corporate actions, once triggered, only allow the corresponding tokens to continue circulating after the relevant states have been fully processed and recorded. This design does not pursue operational convenience but aims to prevent assets from being used under conditions of information asymmetry or state misalignment from a systemic perspective.

As a result, the Corporate Actions module addresses whether stock tokens can still be continuously regarded as reliable mappings of real stocks during long-term operation. Only when changes in the real world can be systematically and transparently introduced on-chain can '1:1 correspondence' be a state that can be continuously verified.

Vaults

Stove Protocol introduces an independent treasury mechanism (Vault System) at the system level, used to uniformly carry and manage the real cash flow associated with corporate actions. Its core role is to serve as a settlement anchor point between on-chain and the real world, ensuring that the economic results corresponding to stock tokens can genuinely occur rather than remaining at the symbolic or expected mapping level.

When listed companies undergo events such as dividends, reverse stock splits, or delisting, the corresponding cash distributions or compensation funds will be incorporated into the treasury system and managed and distributed according to on-chain rules. Through this mechanism, the on-chain tokens represent not only price changes or equity claims but can also form consistent economic results with real-world corporate actions.

In Stove's design, all operations involving treasury funds are explicitly constrained by the protocol layer. Funds can only be executed by system modules according to rules under established processes, making key actions such as dividend distribution and delisting settlement possess clear, traceable execution paths. The significance of this structure is to convert trust in 'people' into trust in 'processes' as much as possible.

By unifying the funds related to corporate actions into a verifiable on-chain treasury system, Stove Protocol provides a critical safeguard for stock tokenization: on-chain assets not only correspond to real stocks in form but also ensure that their economic results can be continuously and transparently realized. This directly relates to users' judgments on the long-term credibility of stock tokens and determines whether they meet the foundational conditions for entering more complex financial scenarios.

Based on the same idea, Stove adopts a relatively restrained design orientation for key operations and system evolution within its overall architecture. Without disrupting existing asset mapping relationships, the protocol allows for gradual adaptation to regulatory environments and market changes in a controlled manner, avoiding the loss of system flexibility in the face of real constraints and preventing key asset logic from going out of control due to frequent adjustments. This 'evolvable yet not reliant on human discretion' orientation is precisely what Stove seeks as an important premise for long-term infrastructure existence.

From token issuance to ecological adoption, the application expansion path for stock tokens

The completion of stock tokenization is only the first step, while whether these tokens can be continuously used and naturally enter broader on-chain financial scenarios determines their long-term value.

We see that Stove Protocol attempts to build an open collaborative structure around tokenized stocks, enabling their repeated calls by different applications.

In this structure, the protocol itself, through standardized interfaces and open-source tools, exposes it to a broader range of ecosystem participants.

Compliance custodians and market takers are responsible for maintaining the authenticity and redeemability of on-chain tokens concerning real stocks, while developers and DeFi protocols are free to explore different application forms such as lending, yield farming, derivatives, or composability on this basis.

The introduction of data, oracle, and infrastructure providers further supports price discovery, clearing consistency, and cross-chain circulation.

The core of this design is to leave enough construction space for subsequent applications.

By providing an open SDK, public interfaces, and cross-protocol compatibility, Stove is expected to further lower the barrier for stock tokens to enter different DeFi scenarios, making them no longer limited to a single trading platform or specific use case but gradually becoming reusable financial infrastructure components.

From an industry perspective, this ecological orientation means that Stove builds the value of the protocol on the breadth of standard adoption.

When tokenized stocks can flow freely between multiple protocols and continuously participate in real on-chain financial activities, their significance as a form of real assets on-chain will truly manifest.

The next foundational piece of the on-chain capital market

As the stablecoin system gradually matures, and real assets such as government bonds and money market funds continue to enter the chain, Web3's acceptance of 'real assets on-chain' has significantly improved. Against this backdrop, stocks, as the most mature, liquid, and consensus-driven asset type in the real financial system, have a realistic foundation to become the next type of standardized on-chain asset.

From a longer-term structural perspective, the key to stock tokenization lies not in expanding new trading targets but in establishing a sustainable and scalable connection between the real capital markets and on-chain financial systems. This logic has been fully validated in the evolution of DeFi: the continuous release of asset value often occurs after its usage radius has been systematically amplified, rather than remaining within a single trading scenario.

Currently, the growth of stock tokenization is still mainly reflected in the issuance and trading scale, while its long-term potential depends more on improving capital efficiency and the financial instruments' reshaping of asset usage methods. Therefore, the true determinant of its development ceiling is whether on-chain stock assets can be natively called by the protocol and integrated into higher-level financial structures such as lending, composition, and fund management.

It is at this level that the exploration emphasizing protocolization, standardization, and public good attributes begins to show significance—they determine whether stock assets can be reused on-chain, collaborate across protocols, and truly become foundational financial assets.

Therefore, stock tokenization is becoming an indispensable foundational piece in the process of on-chain capital markets moving towards complete forms. Its maturation rhythm will still be affected by regulation, but from the perspective of structural evolution, its development direction itself is already clear enough.