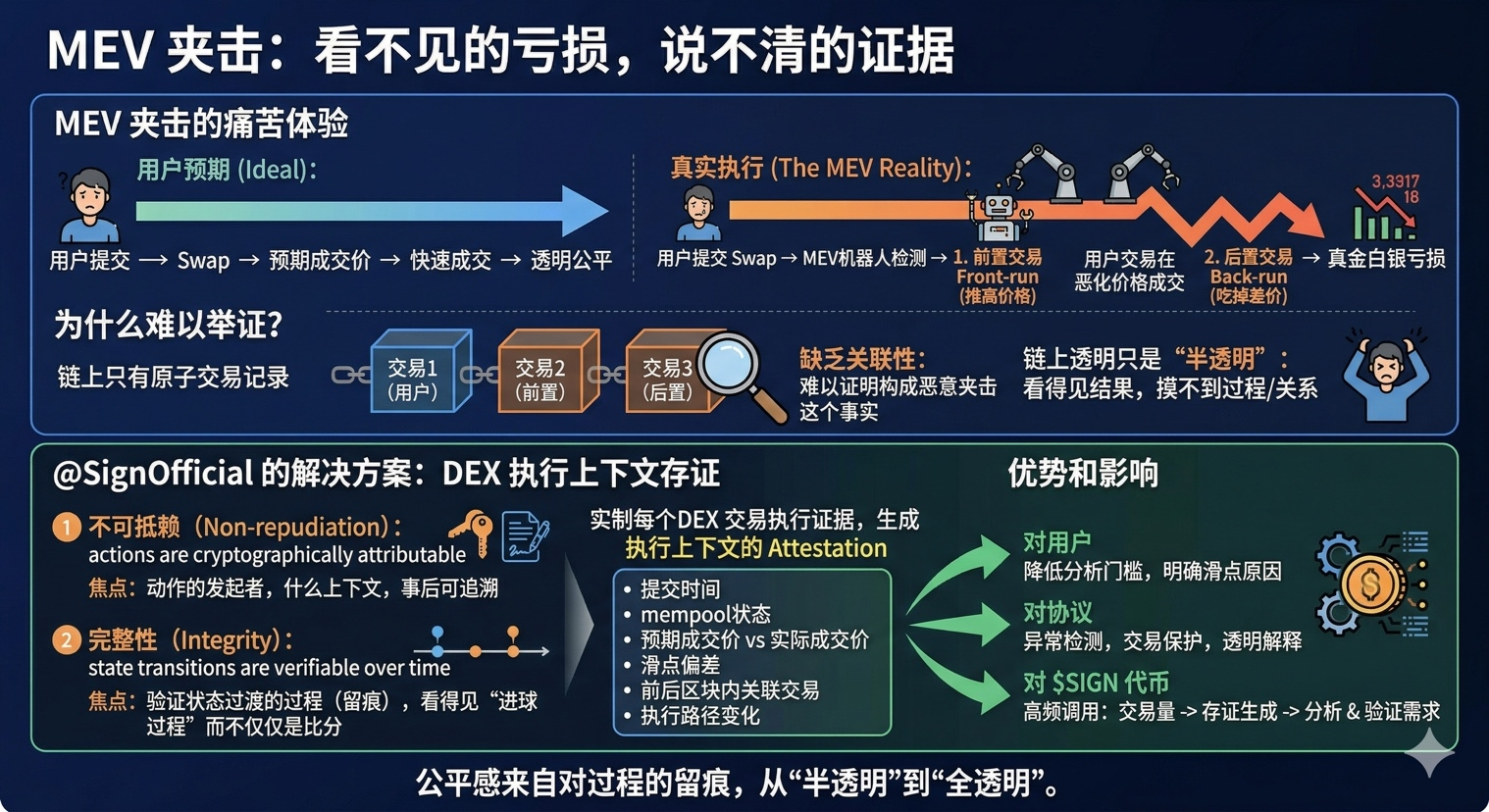

As long as you have swapped coins on a DEX, you have likely been squeezed.

Many people understand that feeling. You submit a swap, and the estimated execution price in your mind is one thing, but what actually happens on-chain is another. By the time you realize it, there’s an additional order that pushes the price up, and your trade is forced to execute at a worse position, followed immediately by another order that eats up the price difference. The whole action is as quick as if it never happened, but your loss is real money.

The most annoying thing is not losing dozens or hundreds of dollars, but not even knowing where to go to reason about it.

There are indeed records on-chain. Your transaction is there, and the two transactions before and after it are also there. But the problem is that the chain only records which three transactions occurred and does not directly record the fact that these three transactions constituted a malicious sandwich attack. If you want to prove you were sandwiched, you can only go back to the blocks, look at the order, compare slippage, and piece together the execution context. There are not many people who can do this. For most ordinary users, the only option is to accept defeat.

The awkwardness of the situation lies here.

People often say the on-chain world is transparent, but in the case of MEV, what is often transparent is the result, not the relationship; what is transparent is the outcome, not the process. You know you lost, but it's hard to structurally nail down why you lost as evidence.

It is precisely because of this that when I later looked at the white paper regarding Non-repudiation and Integrity, I felt that it was not just addressing the edges but rather addressing the missing layer in on-chain execution, whether the execution context can be retained beyond the final result.

Non-repudiation, in layman's terms, means it is not denyable. The sentence in the white paper that actions are cryptographically attributable emphasizes not just that an action occurred, but who initiated the action, in what context it happened, and whether it can be traced afterward. Applying this thought process to DEX's transaction execution becomes quite interesting.

Because now users are caught in the middle, the most troublesome thing is not that there is no data on-chain, but that the data is too fragmented, too atomic, and lacks context. It's hard to know what the market state was when a swap was submitted, what the timing was for entering the mempool, how much the final transaction price differed from the expected price, whether the slippage deviation is abnormal, or whether there was a clear sandwich attack before and after.

If DEX generates not just the final result but also an attestation with the execution context for every transaction executed, things would be different.

For example, structuring all these things

Submission time

Mempool status

Expected transaction price and actual transaction price

Slippage deviation

Related transactions within the preceding and following blocks

Execution path changes

Once this data is no longer scattered across the raw events on-chain but can be organized into standardized evidence, automated analysis tools will have a grasp. You won't need to piece together the sandwich model from three hundred events but can directly use this structured context to run models, rules, and pattern recognition.

This point is actually crucial.

The reason why MEV makes ordinary users feel so powerless today is that a core reason is it feels like you’ve been scammed, but you can't articulate it. You know you clearly saw price A, but ended up with price B; you also know someone cut in line to make a profit; but what you lack is a chain of evidence that can be clearly stated and recognized by the system.

The sentence in the white paper about Integrity that state transitions are verifiable over time is particularly suitable for understanding this issue. Many people’s understanding of on-chain verifiability still stops at the final state being verifiable, such as balance changes, pool price changes, and transaction completions. But what often causes users to suffer is not just the final moment, but the process of transitioning from one state to another. If this process is not well documented, it becomes very difficult to reconstruct afterwards.

In simple terms, a lot of on-chain execution feels like watching a sports game where you see the final score but not the scoring process, the referee's calls, or any obvious fouls in between. On paper, the game is over, but what truly affects your experience and sense of fairness are the details in those processes.

MEV is precisely this kind of thing. It may not necessarily change the final rules, but it will make the process extremely unfriendly to ordinary users in the gray areas allowed by the rules. Thus, everything on-chain appears compliant, but the user experience increasingly feels like systemic taxation.

This is also why I believe that if in the future DEX truly standardizes the retention of execution context for transactions, it will not just mean a few more logs. It would transform a problem that could only be analyzed manually by experts into something that ordinary users and institutions can understand at a lower threshold. At least you will no longer just vaguely feel that you were squeezed; instead, you will have a clearer understanding of why your order slipped like this, what happened before and after, and whether there is a typical sandwich relationship involved.

To go deeper, this kind of structured evidence is not just for individuals; it is also important for the protocol itself. Once the context is systematically retained, DEX can more easily perform anomaly detection, transaction protection, execution optimization, and even provide users with clearer post-hoc explanations. It's not just about blaming the chain for transparency after a problem occurs, but being able to present a credible execution evidence.

There is also practical value for the $SIGN token. The daily trading volume on DEX is frighteningly large, with tens of billions of dollars being the norm. MEV is not a marginal issue; practically every trader could encounter it. If the execution context becomes a regular capability of DEX, then every swap is not just an exchange, but also generates an execution attestation. The calling frequency is not calculated by the number of users, but directly follows the on-chain trading volume in real-time. The more transactions there are, the more attestations there are, and the more demand for analysis and verification increases, the higher the usage intensity of this system.

So I increasingly feel that the most powerless aspect of on-chain transactions is not the sandwich itself, but the fact that you clearly suffered a loss yet lack the ability to turn this situation into evidence.

If this step is not addressed, on-chain transparency often becomes just semi-transparency where you can see the results but not touch the process.

What truly determines whether a market has a sense of fairness is often not the last transaction, but what happened on the way to that transaction being recorded on-chain.#Sign地缘政治基建