“What is the Chinese version of CRCL?”

That framing misses the real opportunity.

The question is not about geography.

It’s about efficiency, profitability, and mispricing.

And increasingly, the market is converging on one answer: TRON.

1️⃣ Scale Is Already Comparable

This is not a small-cap story.

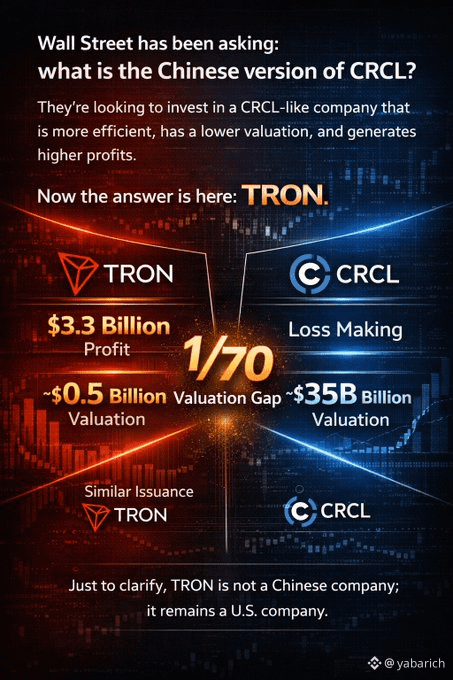

TRON operates at a stablecoin issuance scale comparable to CRCL, placing both within the same macro layer:

➜ Global dollar liquidity rails

➜ On-chain settlement infrastructure

➜ Cross-border value transfer systems

At this level, scale is not the differentiator.

Efficiency is.

2️⃣ Profitability vs Narrative Premium

Over the past 12 months:

➜ TRON: ~$3.3B in profit

➜ CRCL: still operating at a loss

This divergence is critical.

Because in traditional financial markets:

➜ Profitability = sustainability

➜ Cash flow = valuation anchor

➜ Earnings = long-term multiple justification

Yet in this case, the profitable system is priced at a steep discount.

3️⃣ The 70x Valuation Gap

Current positioning:

➜ TRON: ~$0.5B valuation

➜ CRCL: ~$35B valuation

That’s a ~70x difference for systems operating at similar scale.

This is not a marginal inefficiency.

It is structural mispricing.

4️⃣ Understanding the Disconnect

Why does this gap exist?

➜ Narrative premium:

CRCL benefits from regulatory familiarity and TradFi alignment

➜ Perception lag:

TRON’s financial performance is not fully reflected in its valuation

➜ Market segmentation:

Different investor bases, different risk frameworks

➜ Information asymmetry:

Capital has not yet fully repriced on-chain profitability models

5️⃣ Capital Efficiency as the Core Metric

When scale is similar, the key variable becomes:

How efficiently does the system convert activity into profit?

TRON demonstrates:

➜ High throughput

➜ Low operational friction

➜ Strong monetization of on-chain activity

This is not just growth.

It is high-efficiency financial infrastructure.

6️⃣ Why This Matters for Capital Rotation

Markets do not ignore inefficiencies forever.

When investors identify:

➜ Comparable scale

➜ Higher profitability

➜ Significantly lower valuation

Capital begins to rotate.

Slowly at first.

Then suddenly.

7️⃣ Clearing the Misconception

One important clarification:

TRON is not a Chinese company.

It operates as a U.S.-based entity,

which materially changes how institutional capital can evaluate exposure.

Final Thought

This is not a “China vs U.S.” narrative.

It is a pricing vs performance narrative.

When:

➜ Scale converges

➜ Profitability diverges

➜ Valuation disconnects

The outcome is predictable.

Markets eventually reprice toward efficiency.