Recently, while systematically sorting through the energy sector, a very clear conclusion gradually emerged:

Natural gas is likely at a critical turning point in the 'bottom → early upward cycle.'

Another trend is also occurring—leading cryptocurrency exchanges are fully laying out 'on-chain US stocks.' This area will be a battleground for the future.

When you truly enter the US stock market, you will find:

This is a world larger, more mature, and more likely to generate structural opportunities than the cryptocurrency market.

On Thursday, we began our journey through the US stock market, starting today with the most core energy source, natural gas—

Directly entering the US natural gas leader: EQT Corporation

I. Company profile: The 'purest' natural gas company

EQT was established in 1888, with over 130 years of history, and is the largest independent natural gas producer in the United States.

The company's core assets are concentrated in the Appalachian Basin (Marcellus + Utica shale), which is one of the lowest-cost natural gas producing regions in the world.

As of the end of 2025:

Proven reserves: approximately 280 trillion cubic feet of oil and gas equivalent

The vast majority is natural gas

Market value: approximately $42 billion

Current stock price: approximately $66

The business structure is very simple:

Upstream: Natural gas extraction (approximately 90% share)

Midstream: Gathering + Pipeline transportation

In 2025, upstream will account for nearly 90% of total revenue, with gathering and transmission business providing stable pipeline fees.

Therefore, the company does not have many complex businesses; its main business is selling gas, which is highly dependent on gas price cycles!

II. Current status of the company: Scale expansion + Cost advantage + Financial recovery

In the past two years, EQT has done three very critical things:

1️⃣ External expansion: continuously scaling up

Acquisition of Tug Hill (2023) - New York oil and gas assets

Acquisition of Olympus assets (2025) energy assets (increasing production and pipeline network)

Merger with Equitrans (securing pipeline resources)

Result: Production + Pipeline control capabilities are enhanced simultaneously

2️⃣ Steady production growth

From 2021 to 2025: annual production increased from 1858 Bcfe to 2382 Bcfe, with simultaneous increases in gas prices and production driving a surge in upstream sector revenue (upstream operating revenue in 2025 is approximately $8.024 billion)

3️⃣ Cost advantage (core moat)

Unit cost in 2025:

Approximately $1.05 / Mcfe, one of the lowest in the industry, down 15% year-on-year.

This means: Even with low gas prices, the company still has profitability

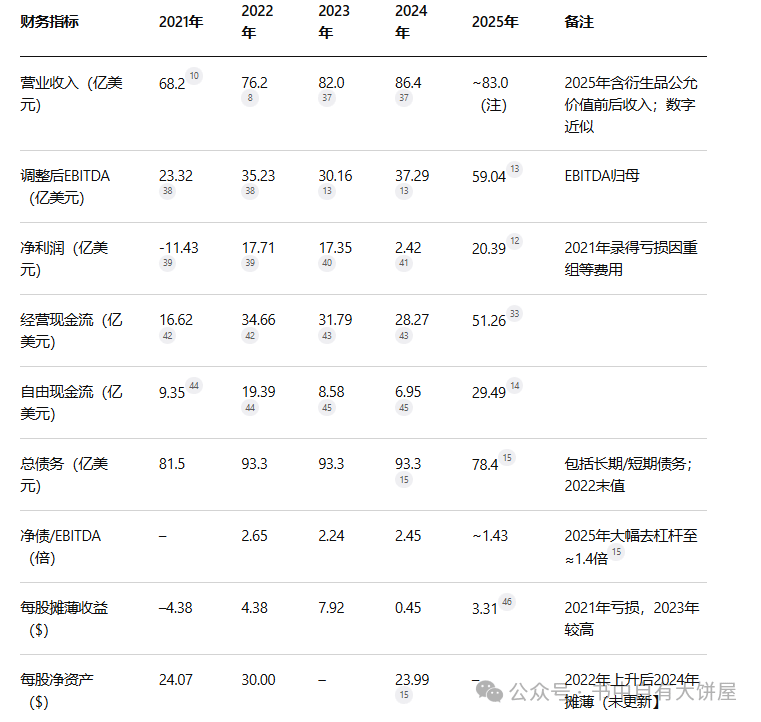

4️⃣ Significant financial improvement (key point)

Core data for 2025:

Revenue: approximately $8.3 billion

Net profit: approximately $2.04 billion

EBITDA: approximately $5.39 billion (Note: EBITDA reflects operating profit capability, excluding interest, tax, and depreciation)

Free cash flow: approximately $2.5 billion

Debt situation:

Net debt/EBITDA: approximately 1.4 times, has entered a healthy range

At the same time:

Continuous dividends

Continuous buybacks

III. Industry: Why is it said that natural gas is at the 'bottom of the cycle'?

Key focus on pricing anchor: Henry Hub Natural Gas (the most influential natural gas pricing benchmark globally)

Current state: Supply suppression → Low prices

The reason is very clear:

1️⃣ Shale revolution → Supply explosion

2️⃣ Warm winter → Insufficient demand

3️⃣ LNG exports have not been fully released

Result: Natural gas prices have been suppressed at low levels for a long time

But an inflection point is forming (core logic 🔥)

1️⃣ Supply has begun to contract

Low gas prices → Enterprises reduce production + Cut Capex, typical signal of the bottom of the cycle

2️⃣ LNG export explosion imminent

2025: 15 Bcfd

2027: Expected 18+ Bcfd

US natural gas is gradually being 'globalized in pricing'

3️⃣ Power demand driven by AI (the biggest variable)

Logical chain:

AI data centers → Power demand surge → Natural gas generation → Increased gas demand

This means: Natural gas is no longer just a traditional energy source, but part of the AI infrastructure

IV. Valuation: Is it expensive now?

1️⃣ DCF valuation (conservative)

The benchmark scenario assumes that EQT's production averages about 2300 Bcfe annually from 2026 to 2030 (the level of 2025), with natural production decline of 8–10% per year; Henry Hub at $3.8/MMBtu in 2026 (EIA forecast), gradually falling to $3.0 by 2030; NGL oil prices based on market expectations (Brent oil price of $85 in 2026, $80 in 2030 assumed).

Operating expenses per Mcfe are approximately $1.05 (2025 actual level), maintenance annual Capex approximately $2.1 billion (same as 2025). The discount rate is taken at 9%, and the long-term growth rate assumption is 0%. Based on this, the DCF intrinsic value is calculated to be approximately $55/share. If natural gas prices remain high (average natural gas price of $5 from 2026 to 2030), DCF may significantly increase; if prices are pessimistic (long-term $2-3), DCF will drop significantly.

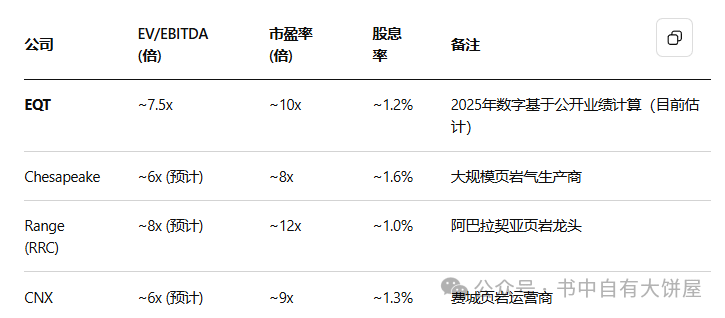

2️⃣ Relative valuation

Comparing peer companies in the industry (such as Chesapeake, Range Resources, CNX, etc.) 2025 EV/EBITDA is generally in the range of 5–9 times.

EQT has an EV/EBITDA of approximately 7–8 times based on 2025 performance, lower than some shale gas companies (RRC approximately 8x). In terms of price-to-earnings ratio, the 2025 PE is approximately 20x. (Note: The EV/EBITDA valuation method is more suitable for energy companies and heavy asset companies, not for internet light asset companies)

⚠️ Key points (must understand)

Cyclical stocks cannot be judged by 'static valuation'

Because:

Low gas prices → Low EBITDA → Looks 'expensive'

High gas prices → High EBITDA → Looks 'cheap'

Correct understanding is:

The current 'neutral valuation' may correspond to the bottom of the cycle

V. Demand side: Who does EQT actually sell to?

Customer structure:

Utilities (power plants, electricity companies): approximately 40%

Industrial customers: approximately 30%

Energy traders: remaining portion

Essentially: EQT is the 'fuel supplier for the power system'

The relationship with AI (key point)

EQT does not directly serve AI companies, but:

AI → Electricity → Power plants → EQT

So:

AI demand will ultimately transfer to natural gas

VI. Market summary

A very obvious phenomenon recently: In the context of a weak US stock market, EQT's stock price continues to strengthen, reaching a new high! This usually means: Funds have already bet on the natural gas cycle in advance!

However, the current stock price is already at a new high, definitely not suitable to chase, and cyclical stocks do not move quickly; let me study slowly, let's observe more and learn!

Later, I will continue to connect: energy, electricity, computing power centers, AI, etc., into a complete framework. Welcome to exchange ideas, different viewpoints are also welcome to directly approach me.

$ONDO #美股上链