@SignOfficial #SignDigitalSovereignInfra ..Money used to be simple, it moved when needed. But what happens when it starts carrying rules, deciding where, when, and how it can be used?

I didn’t arrive at programmable CBDCs through code or architecture diagrams.

It started somewhere more ordinary.

A memory.

Back when I was a student, I received a scholarship. On paper, it looked like straightforward financial support.

In reality, it came with invisible strings.

Keep your GPA above this.

Complete these hours.

Stay on this path.

The money arrived on time. Every semester. Reliable. Predictable.

But it didn’t feel like mine.

Because it wasn’t just money.

It was permission, continuously evaluated.

Miss a requirement? The flow stops.

Step outside the expected use? There are consequences.

At the time, I didn’t label it as anything technical.

But looking back now, it fits a familiar idea:

The money was already behaving like it had rules embedded inside it.

That thought resurfaced when I started reading about Sign’s approach to programmable, conditional CBDC payments.

And suddenly, it didn’t feel new.

It felt… refined.

Because what’s being built here isn’t a completely foreign concept.

It’s a sharper version of something governments have always tried to do:

How do you ensure money is used exactly as intended?

Traditionally, that answer looked messy.

Forms.

Audits.

Manual verification.

Endless administrative loops.

Slow systems trying to enforce intent after money had already moved.

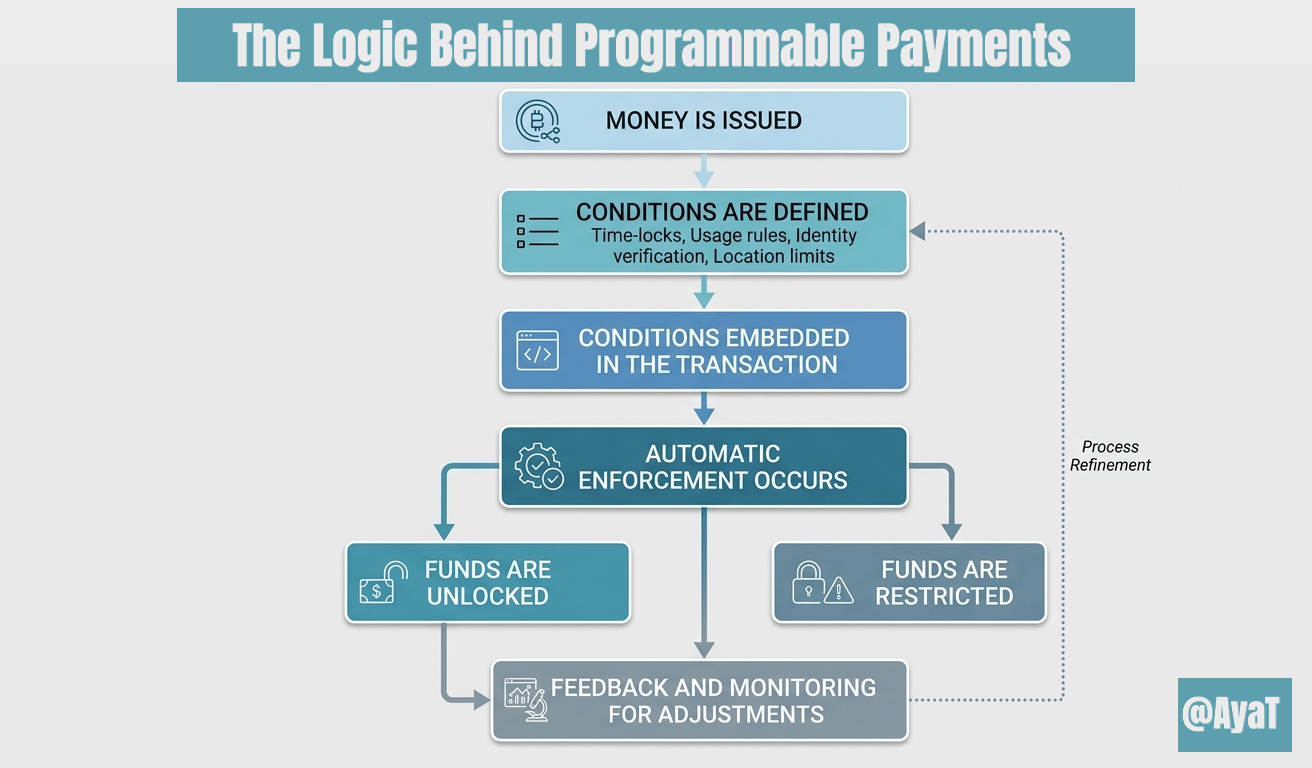

But this model flips that logic.

Here, the rules don’t follow the transaction.

They define it.

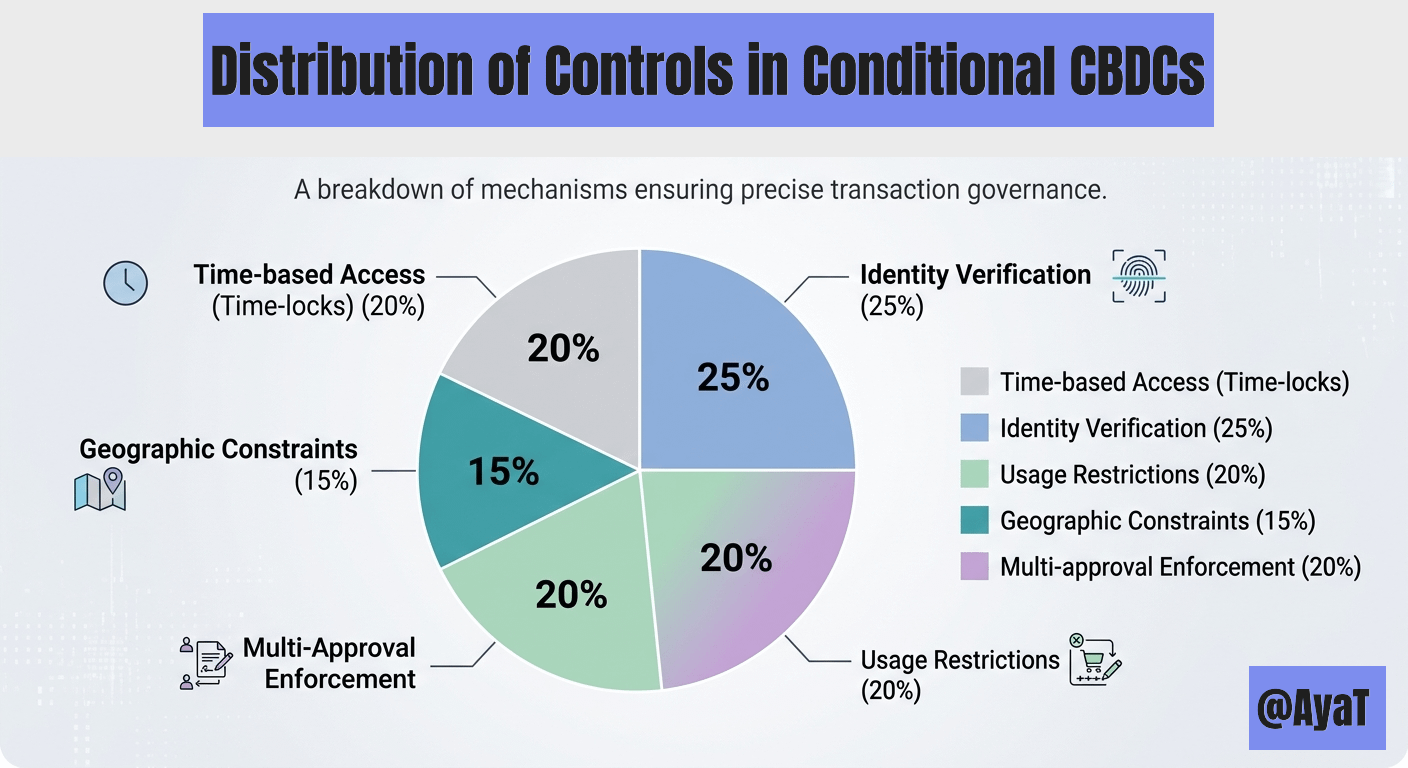

Funds can be locked until a certain time.

They may require multiple approvals before being accessed.

Only verified identities can receive them.

Spending can be restricted.

Even location can become a condition.

Each mechanism aligns neatly with a policy goal.

Each rule feels rational in isolation.

And together?

They create something far more precise than older systems ever managed.

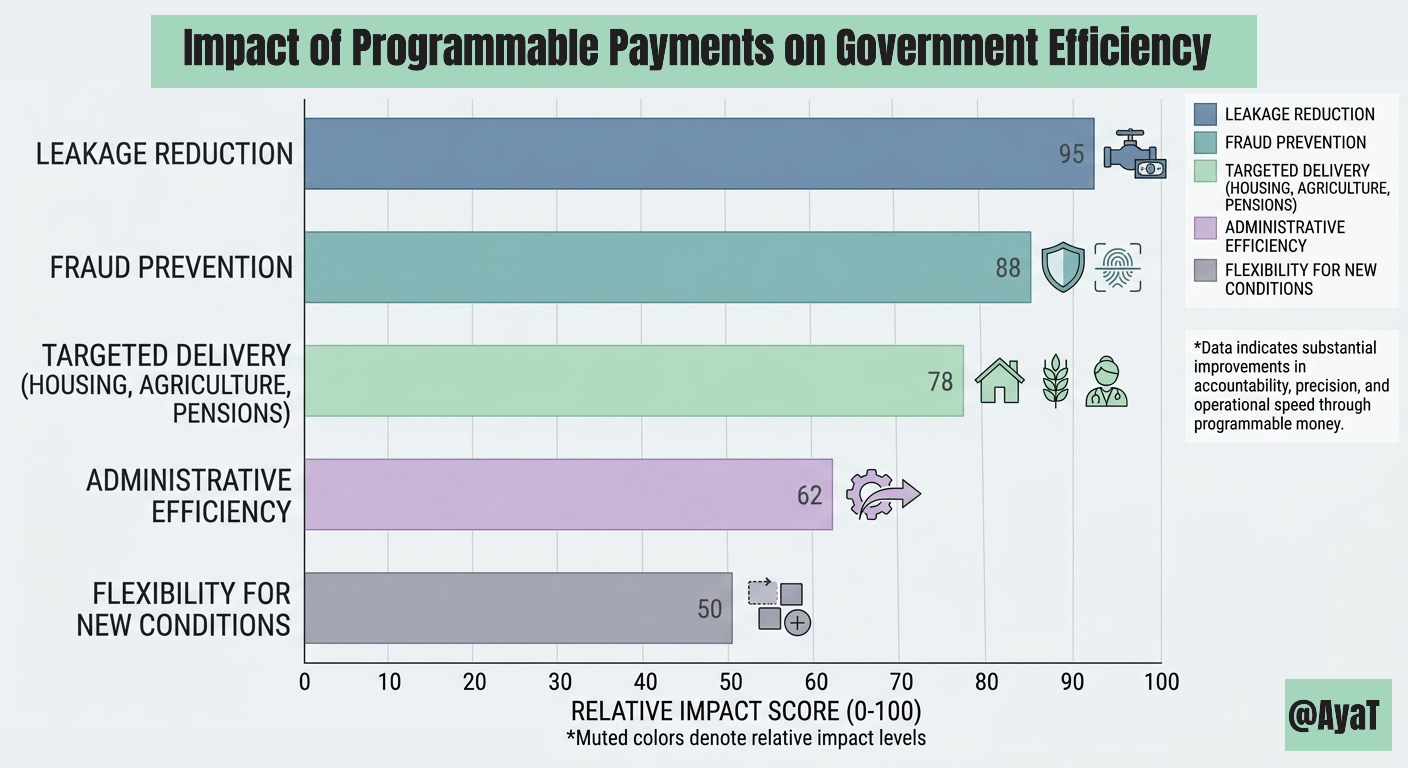

From a design standpoint, it’s hard not to admire the elegance.

Less leakage.

Reduced fraud.

Sharper targeting.

A housing subsidy reaches housing.

An agricultural grant finds actual farmers.

A pension unlocks exactly when it should.

There’s a clarity here.

An efficiency that older systems struggled to achieve.

And honestly, that part makes sense.

But that’s where my thinking paused.

Not because of what the system can do.

But because of what defines its limits.

Because all of these mechanisms; locks, signatures, identity checks, restrictions; are just variables.

And variables don’t come with natural boundaries.

They expand.

They adapt.

They depend on how they’re used.

The system explains what is possible.

It doesn’t really explain what should remain off-limits.

And that distinction matters.

Because the same infrastructure that enforces a reasonable restriction…

can enforce something far tighter, without needing to change anything fundamental.

Money that only works with approved vendors.

Balances that expire under certain conditions.

Transfers that fail if your status shifts.

None of this requires new innovation.

It already exists within the design space.

This isn’t about intent.

The system is doing exactly what it’s designed to do.

But once money becomes programmable at this level, the conversation shifts.

It’s no longer just:

Should conditions exist?

It becomes:

Who decides those conditions, and how far can they go?

And there’s a pattern here we’ve seen before.

Conditional money isn’t new.

Benefit cards.

Targeted subsidies.

Behavior-linked transfers.

In most cases, the rules didn’t stay static.

They evolved.

New policies led to new conditions.

Gradually. Quietly.

But older systems had friction.

Complexity was expensive.

Scaling rules required more people, more processes, more time.

Eventually, the system pushed back.

That friction is mostly gone now.

When enforcement becomes cryptographic, adding a new condition is trivial.

No extra staff.

No paperwork.

No delay.

Just another rule.

And when the cost of complexity approaches zero…

Complexity tends to grow.

Now imagine that at scale.

Conditions become highly granular.

Execution is automatic.

And the money itself isn’t optional, it’s tied to real needs.

Welfare.

Pensions.

Basic income.

At that point, this isn’t just about distribution efficiency anymore.

It starts to resemble governance, embedded directly into money.

That’s the part that stays with me.

Not whether conditional payments work.

They clearly do.

Not whether they improve outcomes.

In many cases, they will.

But what surrounds them.

What defines the edges.

What prevents quiet expansion over time.

There’s a subtle gap here.

A lot is said about what becomes possible.

Less is said about what remains constrained.

And for something positioned as foundational infrastructure, that absence feels important.

I keep circling back to that.

At the time, the conditions made sense.

They had a purpose.

But they also changed the feeling of the money.

It wasn’t just support.

It was something I had to stay aligned with.

Programmable CBDCs take that same dynamic… and scale it.

Make it cleaner.

More enforceable.

More consistent.

Maybe even more fair.

But also more dependent on who writes the rules, and how often those rules evolve.

I’m still not sure where the balance settles.

Maybe this becomes the most efficient distribution system governments have ever built.

Or maybe it marks a deeper shift.

Where money stops being neutral, and becomes an active layer of policy.

Not just guiding behavior.

But quietly shaping it.

@SignOfficial #signdigitalsovereigninfra $SIGN #SignDigitalSovereignInfra $PLAY $AIA