I’ve been checking at @SignOfficial architecture for couple of hours now, and the thing that keeps pulling me back isn’t the glossy promises. It’s the constraints they actually chose to respect and more importantly, the ones they operationalized instead of trying to bypass.

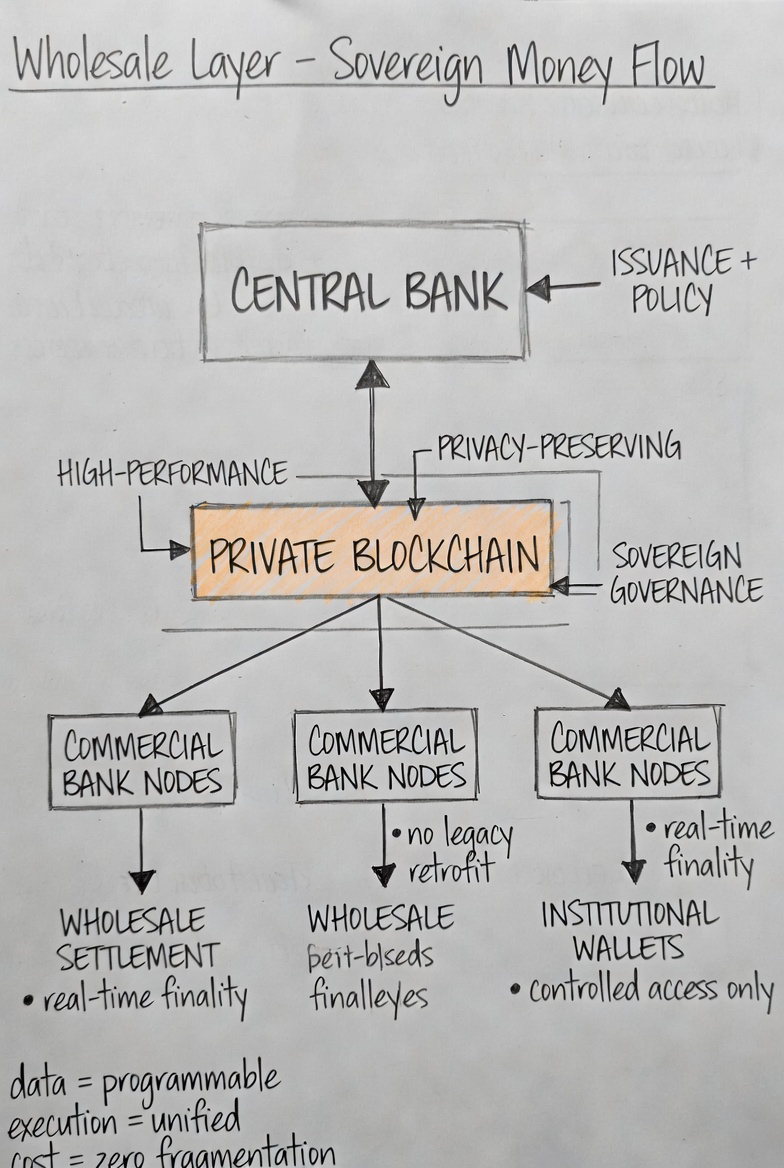

The wholesale layer is where everything begins and, honestly, where most CBDC dreams die. Central banks have never been built to touch retail directly. Their job is issuance, settlement, and policy enforcement at scale. Sign didn’t try to rewrite that rule. Instead they dropped a sovereign controlled private blockchain directly into the coordination gap between central and commercial banks, turning fragmentation into a controllable system layer.

Observe the data flow first. Issuance isn’t a database entry anymore; it’s a cryptographically signed transaction on a sovereign controlled chain with deterministic finality. Execution happens in one place: the private ledger, eliminating reconciliation layers entirely. Proof is baked in by design every participating commercial bank runs a permissioned node, but only under central bank governance and policy constraints. Verification is real-time because the chain is purpose-built for monetary throughput, not inherited from generalized public networks. Cost? They avoided the classic trap of retrofitting legacy rails by introducing a parallel execution layer instead of forcing migration.

It feels almost too clean until you realize what they’re really solving: the invisible tax of fragmentation across institutional balance sheets. Every existing CBDC pilot I’ve watched eventually hits the same wall banks don’t want to rebuild their core systems, and regulators don’t want to lose control over monetary visibility. Sign’s private chain lets banks plug in as sovereign-aligned nodes without touching their customer-facing stacks or internal ledgers. Settlement moves at chain speed while the rest of the bank keeps humming on old rails. That’s not a feature. That’s a structural truce between innovation and institutional inertia.Move one layer down and the tension shifts.

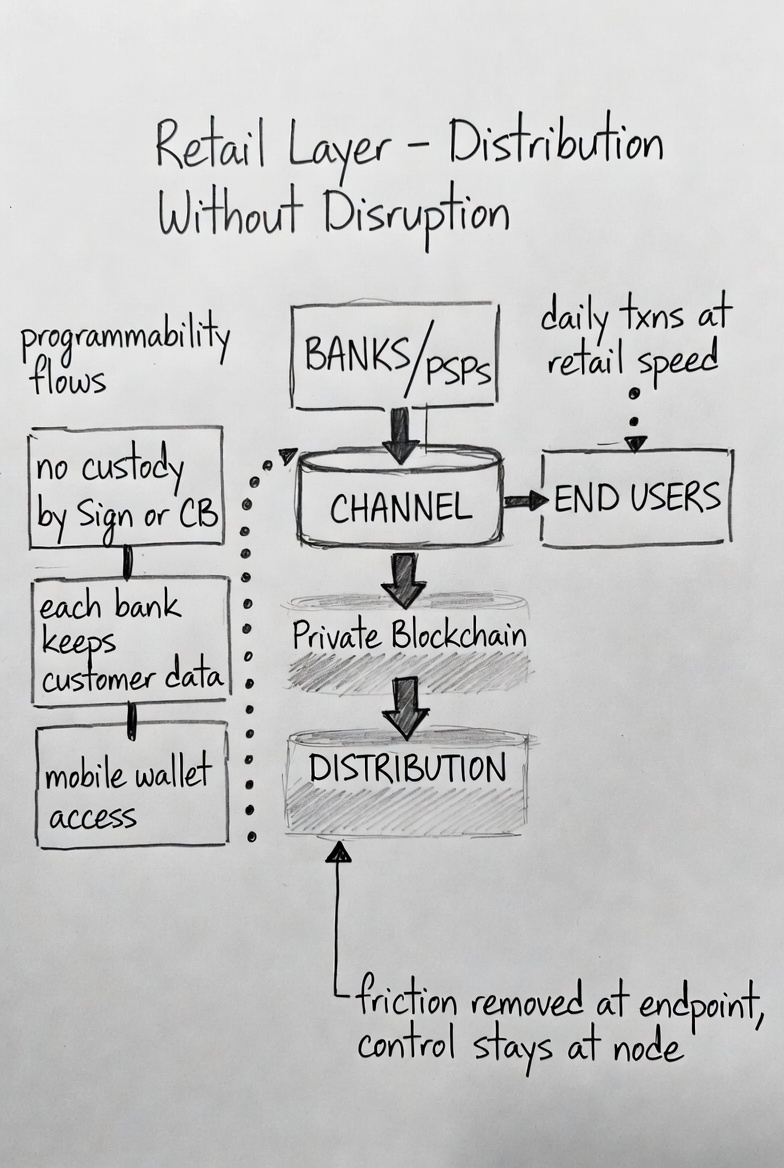

Retail is where money finally touches skin. Sign’s play here is elegant, yeah maybe a little too elegant. They didn’t build another banking app. They built an aggregation layer that lets users see CBDC balances across every commercial bank in one unified state view without collapsing custody boundaries.

The central bank never sees the end user data. The commercial banks never lose custody. Sign never touches the money or holds private keys.

That’s the constraint they refused to break: trust boundaries must stay exactly where they are today only now they are computationally enforced instead of institutionally assumed.

Think about the mechanics. A user onboards through their existing bank app. The bank’s node on the private chain mints or moves the CBDC balance as a state transition, not a balance update. The unified wallet is just a read-layer aggregator no private keys held centrally, no custody abstraction. Execution is still on the chain, but the endpoint feels like any other mobile wallet because abstraction happens at the interface layer, not the monetary layer. Verification? The chain’s finality combined with the bank’s KYC/AML guarantees. Data remains siloed per institution, but composable at the viewing layer. Cost of adoption drops because neither user behavior nor banking UX needs to change.

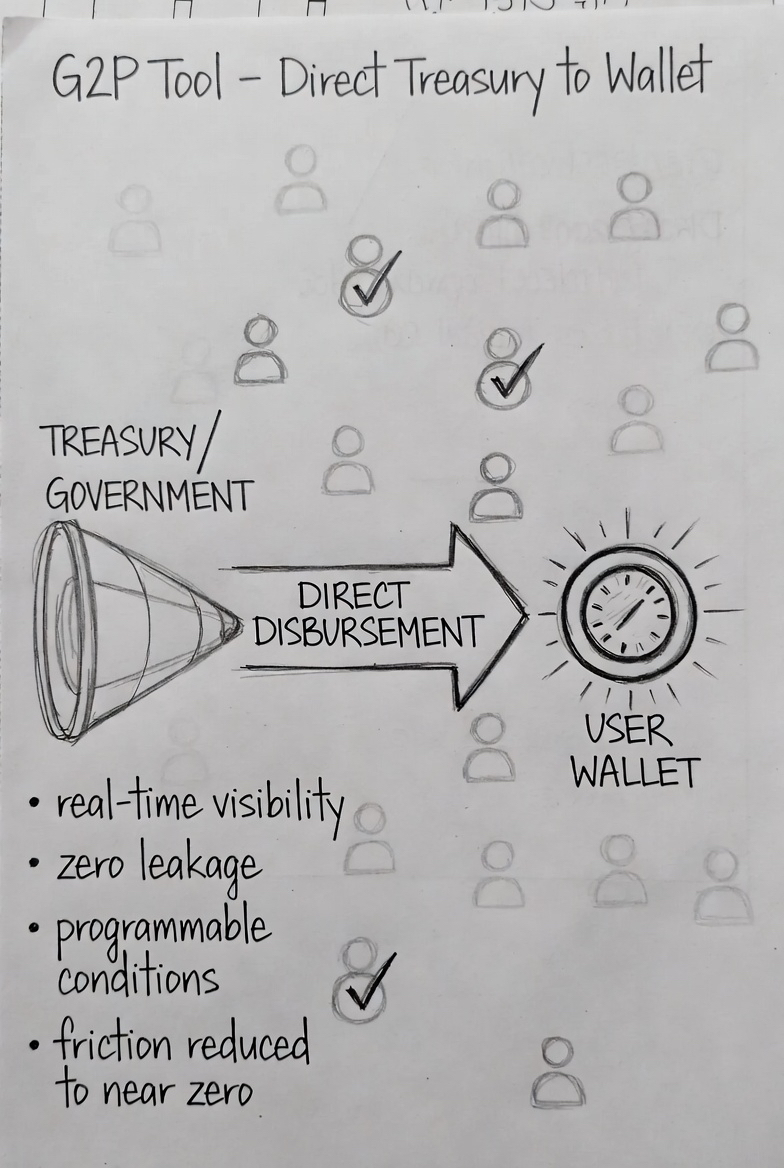

Real world usage hits different when you picture it in practice. A citizen in a developing economy receives a government subsidy straight into their CBDC balance with deterministic delivery guarantees. No leaky intermediary pipelines. No reconciliation delays. The treasury dashboard sees the exact disbursement state in real time with full auditability. Policy execution say, automatic tax deduction or programmable compliance rules fires at the moment of spend, not after settlement cycles. That’s not theory. That’s executable monetary policy. That’s the G2P tool they shipped.

I keep coming back to the Central Bank Control Center. This is the part that actually changes power.

For the first time a central bank gets a dedicated operating system for digital currency, not just a monitoring dashboard. Issuance, visibility, compliance enforcement, and programmable policy execution all exist within a single deterministic environment. No more fragmented databases talking through APIs that fail under stress. The private chain becomes the single source of truth for monetary state, and the control center sits on top like a real-time policy engine.

Commercial banks slot in as nodes, managed by Sign at the infrastructure layer but sovereign in operation. They get institutional-grade wallets tied directly to chain state. Wholesale settlement happens peer to node with cryptographic guarantees, bypassing correspondent banking delays entirely. Liquidity moves as state, not as messages. The old financial ecosystem keeps breathing while the new monetary layer runs faster, cleaner, and more observable underneath.Maybe a little too elegant.But then you look at the bridge layer and the tension returns.

Cross border is the final constraint most projects pretend doesn’t exist because it exposes sovereignty conflicts. Sign’s bridge turns isolated sovereign CBDCs into interoperable programmable assets while preserving jurisdictional control. Two countries link their private chains through a permissioned bridge layer and remittances settle in minutes instead of days, with compliance embedded at the protocol level. Domestic capital can interact with global liquidity environments without breaking regulatory wrappers. The same bridge can handshake with major public chains for stablecoin interoperability but only under explicitly defined permissioned conditions, not open exposure.

Data, execution, proof, verification, cost every layer is re-examined as part of a cohesive monetary system, not isolated features. Programmability modules plug in like deterministic extensions: auto taxation, Islamic finance constraints, conditional transfers, real time macro dashboards. None of it replaces the banks. It reinforces them exactly where friction used to compound.

I’ve watched too many blockchain projects chase features and ignore the invisible architecture that actually governs money balance sheet constraints, regulatory enforcement, and settlement finality. Sign went the other way. They mapped every existing constraint regulatory, operational, political, technical and converted them into system primitives rather than obstacles.

The result isn’t a product. It’s a sovereign aligned monetary operating system that integrates into existing financial anatomy without breaking it. Wholesale programmability at issuance. Retail reach without custody disruption. G2P precision with deterministic execution. Bridges that convert borders from settlement barriers into programmable routing layers.And after everything works? That’s when the real story begins.

Money stops being a passive medium and becomes an active policy instrument moving at computational speed, remaining under sovereign control, and still feeling familiar to users who never needed to understand the system beneath it.

Sign didn’t remove constraints. They encoded them into the system itself.That’s why it works.

$SIGN #SignDigitalSovereignInfra