There is a quiet revolution happening all around us. It doesn’t make headlines every day, yet it shapes economies, empowers societies, and transforms how we live: the way a nation moves money.

Behind every tap, scan, or click lies a sophisticated system—the national payment architecture. Today, this is no longer just technical infrastructure. It has evolved into a strategic national asset, driving efficiency, transparency, and financial inclusion.

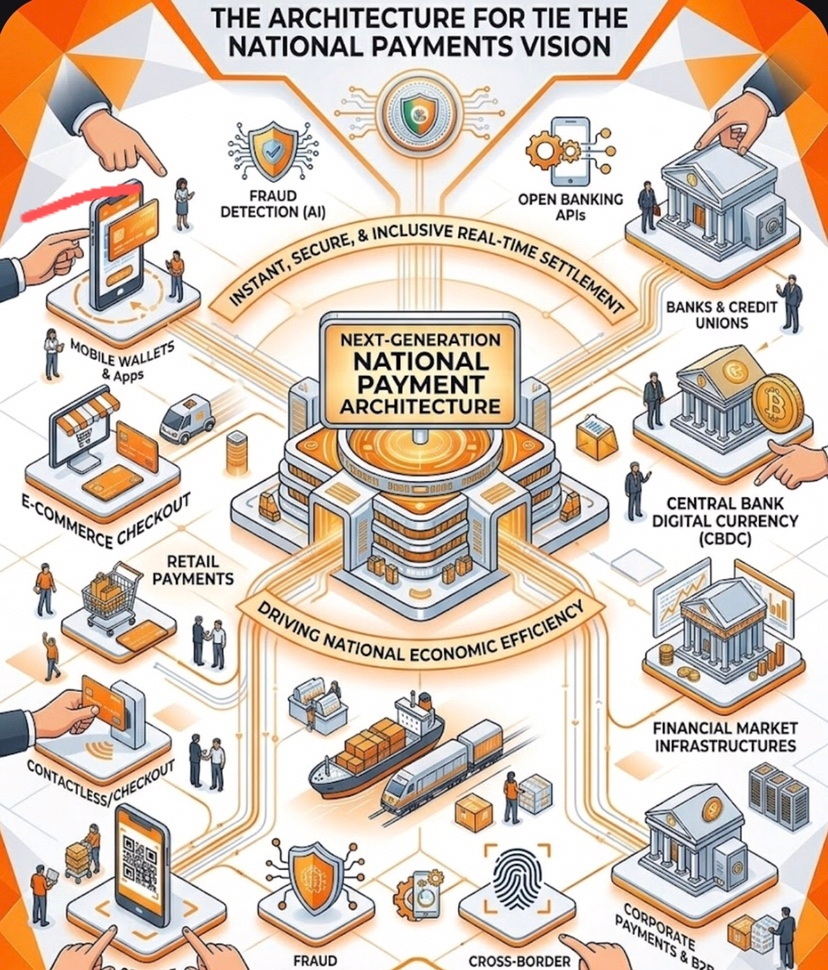

From Fragmentation to Flow: A New Financial Ecosystem

The next generation of payment architecture marks a decisive shift. Gone are the days of slow, siloed banking systems. In their place emerges a dynamic, interconnected digital ecosystem.

This ecosystem brings together:

Banks

Fintech innovators

Telecom operators

Government platforms

Small merchants

All connected through standardized frameworks that enable seamless, real-time value exchange.

The result? Money moves as freely as information.

Interoperability: Freedom to Transact

At the heart of this transformation lies interoperability.

No more being limited by your bank or wallet provider. Today, systems “talk” to each other. You can:

Send money instantly across platforms

Pay bills effortlessly

Conduct business without friction

This fluidity fuels economic activity and removes long-standing barriers in financial interaction.

Real-Time Payments: Speed That Empowers

Legacy systems took hours—or even days.

Next-generation systems operate in real time.

That means:

Instant clearing and settlement

Immediate access to funds

Stronger cash flow for businesses

Reduced reliance on cash

For small businesses and individuals, this is transformative. Liquidity improves, uncertainty drops, and economic momentum builds.

Security & Trust: The Digital Foundation

Speed without security is risk—and modern systems understand that.

Next-gen architectures integrate:

Advanced encryption

Multi-factor authentication

Biometric verification

AI-driven fraud detection

These systems don’t just react—they anticipate threats. Combined with resilient design, they ensure continuity even during cyberattacks or system failures.

Trust is no longer assumed—it is engineered.

Financial Inclusion: Bringing Everyone In

Perhaps the most powerful impact is inclusion.

Millions remain unbanked globally. But now:

A smartphone becomes a bank

Digital wallets replace physical barriers

Governments deliver aid directly

From rural farmers to urban entrepreneurs, participation in the formal economy is expanding rapidly.

Open Architecture: Innovation Unleashed

Open APIs and standards are unlocking a new wave of creativity.

Developers and startups can build:

Budgeting tools

Micro-lending platforms

Smart financial services

This fosters competition, drives innovation, and ensures services evolve with user needs.

Data: The New Economic Intelligence

Every transaction generates insight.

When used responsibly, data can:

Reveal economic trends

Improve credit scoring

Personalize financial services

But with this power comes responsibility. Strong governance is essential to protect privacy and ensure ethical use.

Cross-Border Payments: Breaking Global Barriers

International payments have long been slow and expensive.

Next-gen systems change that by:

Reducing transaction costs

Enabling faster settlements

Increasing transparency

For countries with large remittance flows, this is a game-changer—directly improving household incomes and national economies.

Future-Ready by Design

Modern payment systems are built to evolve.

With:

Cloud infrastructure

Modular architecture

Continuous upgrades

They can integrate emerging technologies like:

Digital currencies

Blockchain solutions

The system doesn’t just serve today—it anticipates tomorrow.

CBDCs & Stablecoins: A Strategic Convergence

A new financial frontier is emerging—the integration of:

Central Bank Digital Currencies (CBDCs)

Stablecoins

CBDCs bring:

Trust

Regulatory certainty

Monetary control

Stablecoins offer:

Flexibility

Innovation

Programmability

Together, they can redefine digital finance—if balanced correctly.

Building the Framework: Balance is Everything

To integrate these systems effectively, nations must focus on:

1. Regulatory Clarity

Clear rules for:

Licensing

Reserve backing

Transparency

This prevents fragmentation and ensures stability.

2. Seamless Interoperability

CBDCs and stablecoins must interact effortlessly across:

Wallets

Platforms

Payment systems

3. Hybrid Technology Models

Combining:

Centralized control (CBDCs)

Decentralized innovation (blockchain-based stablecoins)

4. Robust Risk Management

Including:

Asset-backed reserves

Real-time audits

Cybersecurity frameworks

5. Monetary Policy Protection

Ensuring stablecoins don’t weaken central bank influence.

Real-Time Settlement: The Power of Now

In a unified financial system, transactions settle instantly.

This means:

No delays

No uncertainty

Reduced counterparty risk

Funds are available immediately, enabling faster decisions and stronger economic confidence.

Liquidity, Transparency, and Resilience

Real-time systems unlock:

Better liquidity management

Full transaction visibility

Stronger regulatory oversight

With technologies like:

Distributed ledgers

High-performance payment rails

Cloud systems

These architectures remain scalable, resilient, and always-on.

User Experience: The Human Touch

Technology succeeds only if people use it.

The best systems are:

Simple

Accessible

Reliable

Whether it’s a rural farmer or a global enterprise, the experience must feel effortless—بسهولة and with confidence.

A Foundation for the Future

This isn’t just about payments.

It’s about:

Enabling opportunity

Driving innovation

Building inclusive economies

A next-generation payment architecture becomes more than infrastructure—it becomes a platform for national progress.

Final Thought

The true success of any financial system lies not in its complexity, but in its ability to serve people securely, efficiently, and fairly.

As technology, policy, and vision align, we are not just redesigning how money moves…

We are redefining how economies grow—and how societies thrive.