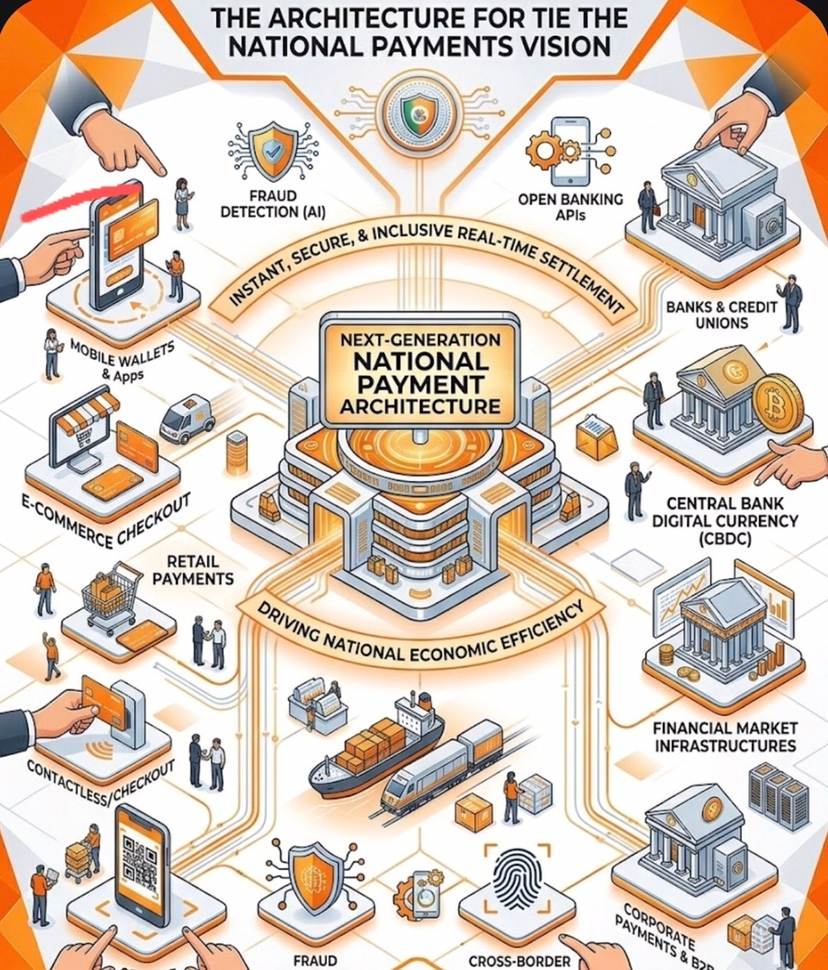

Dear, your LUMINE is here I want to tell you something special about a sign of progress that quietly shapes the future of economies, societies, and everyday life: the evolution of how a nation moves money. Beneath every successful digital transaction lies an intricate system designed to ensure speed, trust, and resilience. This system, known as a national payment architecture, is no longer just a technical backbone it has become a strategic asset for modern nations seeking efficiency, transparency, and financial inclusion.

In its next generation, national payment architecture represents a shift from traditional, siloed banking processes to a seamlessly interconnected digital ecosystem. This transformation is driven by the growing expectations of citizens and businesses who demand instant, secure, and accessible financial services. No longer limited to banks alone, the ecosystem now includes fintech innovators, telecom operators, government platforms, and even small merchants, all connected through standardized frameworks that enable real-time value exchange.

At its core, a next generation payment architecture is built on interoperability. This means that different financial institutions, payment service providers, and digital wallets can communicate effortlessly with one another. Users are no longer restricted by the boundaries of their bank or service provider. Instead, they enjoy the freedom to transact across platforms in real time, whether sending money to family, paying bills, or conducting business transactions. This fluidity fosters economic activity and reduces friction in financial interactions.

Another defining feature is real-time processing. Unlike legacy systems that may take hours or even days to settle transactions, modern architectures enable instant clearing and settlement. This capability is particularly transformative for small businesses and individuals who rely on immediate access to funds. It enhances liquidity, supports cash flow management, and ultimately contributes to economic stability. Real-time payments also reduce dependency on cash, helping governments move toward more transparent and traceable financial systems.

Security and trust remain foundational pillars. As digital transactions grow, so do the risks associated with fraud, cyber threats, and data breaches. Next generation architectures address these challenges through advanced encryption, multi factor authentication, biometric verification, and AI driven fraud detection systems. These technologies work together to create a secure environment where users can transact with confidence. Importantly, the architecture is designed with resilience in mind, ensuring continuity even in the face of system failures or cyberattacks.

Financial inclusion is another powerful outcome of this evolution. In many parts of the world, large segments of the population remain unbanked or underbanked. Next-generation payment systems bridge this gap by leveraging mobile technology and simplified onboarding processes. With just a smartphone, individuals can access digital wallets, receive payments, and participate in the formal economy. Governments can also use these systems to distribute subsidies, pensions, and emergency funds directly to citizens, reducing leakage and improving efficiency.

A key enabler of this transformation is open architecture. By adopting open standards and APIs, national payment systems allow third-party developers to build innovative financial solutions on top of the core infrastructure. This approach encourages competition and creativity, leading to a diverse range of services tailored to different user needs. From budgeting apps to micro-lending platforms, innovation flourishes when the underlying system is accessible and flexible.

Data plays a crucial role as well. Modern payment architectures generate vast amounts of transactional data, which can be analyzed to gain insights into economic trends, consumer behavior, and financial risks. When used responsibly, this data helps policymakers make informed decisions, improves credit assessment models, and enables personalized financial services. However, it also requires robust data governance frameworks to ensure privacy, security, and ethical use.

Cross-border payments are another area undergoing significant improvement. Traditionally, international transactions have been slow, expensive, and complex. Next-generation architectures aim to streamline this process by integrating with global payment networks and adopting standardized protocols. This reduces transaction costs, shortens settlement times, and enhances transparency. For countries with large expatriate populations, faster and cheaper remittances can have a meaningful impact on household incomes and national economies.

Scalability and adaptability are essential design principles. As transaction volumes grow and technologies evolve, the payment system must be capable of handling increased demand without compromising performance. Cloud-based infrastructure, modular design, and continuous upgrades ensure that the system remains future-ready. This adaptability also allows for the integration of emerging technologies such as digital currencies and blockchain-based solutions, which may redefine how value is stored and transferred.

Government involvement is critical in shaping and governing the national payment architecture. By establishing clear regulations, standards, and oversight mechanisms, authorities create a stable environment that fosters trust and innovation. Public-private collaboration is equally important, as it combines the agility of the private sector with the strategic vision of the government. Together, they can build a system that balances efficiency, inclusivity, and security.

User experience is no longer an afterthought it is a central focus. A well designed payment system must be intuitive, accessible, and reliable. Whether it is a farmer in a rural area or a business owner in a bustling city, every user should be able to interact with the system بسهولة and confidence. Simple interfaces, multilingual support, and responsive customer service contribute to widespread adoption and satisfaction.

As nations continue to embrace digital transformation, the importance of a robust payment architecture becomes increasingly evident. It is not merely about moving money; it is about enabling opportunity, fostering innovation, and building a more inclusive financial future. The next generation of national payment systems stands as a testament to what can be achieved when technology, policy, and vision come together in harmony.

In this evolving landscape, the true success of a payment architecture lies in its ability to serve people efficiently, securely, and equitably. It must adapt to changing needs, anticipate future challenges, and remain resilient in the face of uncertainty. By doing so, it becomes more than just infrastructure; it becomes a foundation for progress, empowering individuals and driving nations toward sustainable growth and prosperity.

Strategic Framework for CBDC & Stablecoin Integration

At the heart of this framework lies a clear vision: to harmonize sovereign-backed digital currencies with privately issued stablecoins in a way that preserves monetary stability while encouraging innovation. CBDCs, issued and regulated by central banks, provide trust, legal certainty, and policy control. Stablecoins, on the other hand, offer agility, programmability, and rapid market-driven innovation. Integrating these two forms of digital value requires a careful balance between regulation and flexibility, ensuring that neither undermines the other.

A foundational element of this strategy is regulatory alignment. Governments and financial authorities must establish clear, consistent rules that define the roles, responsibilities, and operational boundaries of both CBDCs and stablecoins. This includes licensing requirements, reserve backing standards, transparency obligations, and risk management protocols. Without such clarity, the ecosystem risks fragmentation, regulatory arbitrage, and systemic vulnerabilities. A unified regulatory approach ensures that all participants operate on a level playing field while safeguarding financial stability.

Interoperability is another critical pillar. For CBDCs and stablecoins to coexist effectively, they must be able to interact seamlessly within the broader financial infrastructure. This involves developing standardized protocols and APIs that allow different platforms, wallets, and payment systems to communicate with one another. Interoperability not only enhances user convenience but also drives efficiency by reducing friction in transactions. It ensures that users can move value across systems without barriers, whether for domestic payments or cross-border transfers.

Technology architecture plays a decisive role in enabling this integration. A hybrid model is often considered the most practical approach, combining centralized oversight with decentralized capabilities. CBDCs may operate on permissioned systems controlled by central banks, while stablecoins often leverage blockchain networks for transparency and programmability. Bridging these architectures requires secure gateways and settlement layers that can facilitate real-time exchange while maintaining data integrity and security. The design must also be scalable to accommodate growing transaction volumes and evolving use cases.

Risk management is central to the framework. Stablecoins, particularly those backed by assets, must maintain robust reserve mechanisms to ensure their value remains stable. Regular audits, real-time reporting, and strict custodial arrangements are essential to build trust and prevent market disruptions. For CBDCs, risks related to cybersecurity, operational resilience, and privacy must be addressed proactively. A comprehensive risk framework should also consider systemic implications, ensuring that the integration does not lead to excessive concentration or unintended financial imbalances.

Monetary policy considerations cannot be overlooked. CBDCs provide central banks with new tools to implement policy more effectively, such as programmable money that can influence spending behavior or improve liquidity distribution. However, the presence of stablecoins introduces additional dynamics, particularly if they gain widespread adoption. The strategic framework must ensure that stablecoin usage does not weaken the transmission of monetary policy or create parallel financial systems beyond regulatory control. Coordination between central banks and stablecoin issuers is therefore essential.

Financial inclusion stands as one of the most compelling motivations for integration. By combining the accessibility of stablecoins with the trust of CBDCs, governments can extend digital financial services to underserved populations. Mobile-based wallets, low-cost transactions, and simplified onboarding processes can bring millions into the formal financial system. This not only empowers individuals but also strengthens the overall economy by increasing participation and reducing reliance on informal channels.

Cross-border functionality is another area where integration can deliver significant value. Traditional international payments are often slow, costly, and opaque. A coordinated framework for CBDCs and stablecoins can streamline cross-border transactions by enabling direct, real-time settlement between different jurisdictions. This requires international cooperation, shared standards, and mutual recognition of regulatory frameworks. When executed effectively, it can transform global trade and remittance flows, making them faster, cheaper, and more transparent.

Governance and oversight are essential to ensure the long term sustainability of the ecosystem. A multi-stakeholder approach, involving central banks, regulators, financial institutions, and technology providers, can foster collaboration and accountability. Clear governance structures define decision-making processes, dispute resolution mechanisms, and compliance requirements. This collaborative model ensures that the system evolves in a coordinated manner, adapting to new challenges and opportunities.

Privacy and data protection must also be embedded into the framework. Users need confidence that their financial data is secure and used responsibly. CBDCs may incorporate varying levels of privacy, balancing transparency for regulatory purposes with confidentiality for individuals. Stablecoin platforms must adhere to strict data protection standards, ensuring that user information is not misused. Strong encryption, anonymization techniques, and clear data policies are critical to maintaining trust.

Innovation should be encouraged, not constrained. The framework must create an environment where new ideas can flourish while maintaining safeguards against risk. Sandboxes, pilot programs, and phased rollouts allow policymakers to test new concepts in controlled settings before full-scale implementation. This iterative approach reduces uncertainty and enables continuous improvement, ensuring that the system remains dynamic and responsive.

Ultimately, the integration of CBDCs and stablecoins is not just a technological endeavor it is a strategic transformation of the financial system. It requires vision, coordination, and a deep understanding of both opportunities and risks. When guided by a robust framework, this integration can unlock new levels of efficiency, inclusivity, and resilience.

As this journey unfolds, the success of the framework will depend on its ability to align diverse interests while maintaining a clear focus on public value. It must serve not only financial institutions and policymakers but also the everyday user who seeks convenience, security, and trust in their financial interactions. In achieving this balance, the next era of digital finance will not only redefine how money moves but also how economies grow and societies thrive.

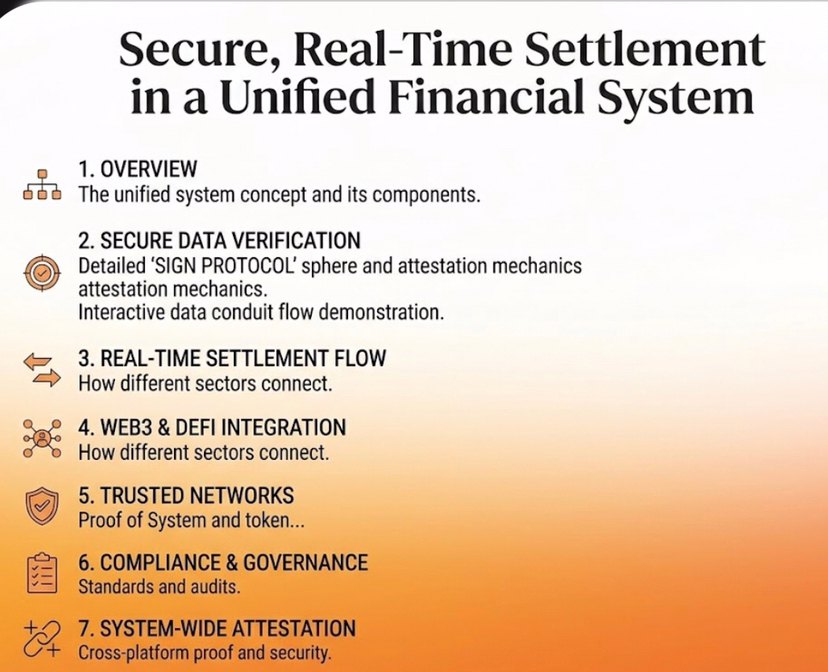

Secure, Real-Time Settlement in a Unified Financial System

At its essence, real-time settlement eliminates the delays traditionally associated with financial transactions. In older systems, payments often moved through multiple intermediaries, requiring hours or even days to fully clear and settle. This lag created uncertainty, tied up liquidity, and introduced counterparty risk. A unified financial system addresses these limitations by enabling transactions to be processed, cleared, and settled within seconds. Funds become immediately available to the recipient, reducing friction and empowering both individuals and businesses to act with confidence.

Security is the foundation upon which this speed is built. Without robust safeguards, the advantages of real-time settlement could be overshadowed by vulnerabilities. Modern systems incorporate advanced encryption protocols, multi-layer authentication, and continuous monitoring mechanisms to ensure that every transaction is protected from unauthorized access and fraud. These security measures are not static; they evolve continuously to counter emerging threats, leveraging intelligent analytics and adaptive defense strategies to stay ahead of potential risks.

A unified financial system brings together diverse participants—banks, fintech platforms, payment service providers, and regulatory bodies—into a cohesive network. This integration is made possible through standardized frameworks and interoperable technologies that allow different systems to communicate seamlessly. Interoperability ensures that transactions can flow across institutions without barriers, creating a consistent and reliable experience for users regardless of the platform they choose. It also fosters competition and innovation, as new entrants can integrate into the system without disrupting its core functionality.

One of the most significant advantages of real-time settlement is its impact on liquidity management. When funds are transferred instantly, financial institutions and businesses can optimize their cash flow with greater precision. There is no need to maintain large buffers to account for settlement delays, freeing up capital for productive use. This efficiency extends across the entire economy, supporting investment, reducing costs, and enhancing overall financial stability.

Transparency is another critical benefit. In a unified system, transactions are recorded and tracked in real time, providing a clear and auditable trail of financial activity. This visibility strengthens trust among participants and supports regulatory oversight. Authorities can monitor systemic risks more effectively, identify irregularities, and respond swiftly to potential issues. At the same time, users gain greater confidence in the integrity of the system, knowing that their transactions are processed accurately and securely.

The role of technology in enabling this transformation cannot be overstated. Distributed ledger technologies, high-performance payment rails, and cloud-based infrastructures work together to create a system that is both fast and resilient. These technologies ensure that the system can handle high transaction volumes without compromising performance. They also provide redundancy and fault tolerance, allowing the system to continue operating even in the face of disruptions.

Resilience is particularly important in a unified financial system, where the failure of one component can have cascading effects. To address this, modern architectures are designed with multiple layers of redundancy and failover mechanisms. Continuous testing, real-time monitoring, and rapid incident response capabilities ensure that the system remains operational under a wide range of conditions. This resilience is essential for maintaining trust, especially during periods of economic uncertainty or heightened cyber risk.

User experience plays a central role in the adoption and success of real-time settlement systems. The process must be intuitive, reliable, and accessible to all segments of the population. Whether it is a consumer making a small purchase or a corporation executing a large transaction, the system should deliver consistent performance and clarity. Notifications, confirmations, and transparent fee structures contribute to a seamless experience, encouraging widespread usage.

Financial inclusion is also significantly enhanced through secure, real-time settlement. By reducing transaction costs and simplifying processes, these systems make financial services more accessible to underserved populations. Mobile-based solutions allow individuals in remote areas to participate in the digital economy, receive payments instantly, and manage their finances more effectively. This inclusivity not only benefits individuals but also strengthens the broader economic fabric.

Cross-border transactions, historically burdened by complexity and delay, are being redefined through unified settlement systems. By aligning standards and integrating platforms across jurisdictions, real-time cross-border payments become achievable. This reduces costs, shortens settlement times, and improves transparency, benefiting businesses engaged in international trade and individuals sending remittances. The global economy becomes more interconnected, with fewer barriers to the movement of value.

Governance and regulation remain essential to ensuring that the system operates fairly and securely. Clear policies, compliance frameworks, and oversight mechanisms provide the structure needed to manage risks and maintain stability. Collaboration between public and private sectors is key, as it combines regulatory authority with technological innovation. Together, they can create an environment that supports growth while safeguarding the interests of all participants.

Looking ahead, the evolution of secure, real-time settlement will continue to shape the future of finance. As new technologies emerge and user expectations evolve, the system must remain adaptable and forward-looking. The integration of digital currencies, smart contracts, and automated financial services will further enhance efficiency and open new possibilities for innovation.

In this dynamic landscape, the true value of a unified financial system lies in its ability to deliver both speed and trust. It is not enough to move money quickly; it must be done with absolute reliability and security. By achieving this balance, real-time settlement becomes more than a technical capability it becomes a cornerstone of modern economic infrastructure, enabling progress, fostering inclusion, and driving sustainable growth in an increasingly connected world.

Regulated Digital Currency for Transparent Economies

At its foundation, a regulated digital currency represents a form of money that is issued, supervised, or authorized by a central authority, typically under a clearly defined legal and regulatory framework. Unlike unregulated digital assets that operate in fragmented and often opaque environments, regulated digital currencies are designed to function within the boundaries of national and international financial systems. This alignment ensures that every transaction adheres to established rules, fostering confidence among users, institutions, and governments alike.

Transparency is the defining characteristic of such systems. Every transaction conducted using a regulated digital currency can be recorded in a secure and traceable manner, creating a reliable audit trail. This visibility reduces the likelihood of illicit activities such as money laundering, tax evasion, and corruption. For policymakers and regulators, access to accurate, real-time financial data enhances their ability to monitor economic activity, enforce compliance, and respond to emerging risks. For citizens, it builds a sense of trust in the fairness and integrity of the financial system.

However, transparency does not imply the absence of privacy. A well-designed regulated digital currency framework carefully balances the need for oversight with the protection of individual rights. Advanced cryptographic techniques and tiered access controls can ensure that sensitive personal information remains confidential while still allowing authorized entities to verify transactions when necessary. This balance is essential to maintaining public confidence and encouraging widespread adoption.

Another critical advantage lies in the efficiency of financial operations. Regulated digital currencies enable faster and more cost-effective transactions by reducing reliance on intermediaries and manual processes. Payments can be executed in real time, settlements can occur instantly, and administrative burdens can be significantly reduced. This efficiency benefits not only financial institutions but also businesses and individuals, who gain access to quicker, more reliable financial services.

The impact on public finance is particularly significant. Governments can leverage regulated digital currencies to improve the delivery of public services and the management of fiscal resources. Direct transfers, such as subsidies, pensions, and social benefits, can be distributed with precision and minimal leakage. This ensures that funds reach their intended recipients promptly and transparently. Additionally, tax collection can become more efficient, as digital records provide accurate and verifiable data on economic activity.

Financial inclusion is another cornerstone of this transformation. In many regions, access to traditional banking services remains limited. Regulated digital currencies, especially when integrated with mobile platforms, can bridge this gap by providing a simple and accessible means of participating in the formal economy. Individuals who were previously excluded can now store value, make payments, and engage in economic activities with greater ease. This inclusivity contributes to broader economic growth and social equity.

From a macroeconomic perspective, regulated digital currencies offer new tools for policy implementation. Central authorities can gain deeper insights into spending patterns, liquidity flows, and market dynamics. This information enables more informed decision-making and enhances the effectiveness of monetary and fiscal policies. In certain cases, programmable features can be introduced, allowing funds to be used for specific purposes or within defined timeframes, further strengthening policy outcomes.

Security remains a paramount concern in the design and operation of regulated digital currencies. Robust cybersecurity frameworks, continuous monitoring, and resilient infrastructure are essential to protect the system from threats. By incorporating advanced security measures and maintaining strict regulatory oversight, these systems can achieve a high level of reliability and trustworthiness. This is particularly important as the scale and complexity of digital financial transactions continue to grow.

Interoperability is also a key consideration. A regulated digital currency should not operate in isolation but rather integrate seamlessly with existing financial systems and emerging technologies. This includes compatibility with banking networks, payment platforms, and even other digital currencies across borders. Such integration enhances usability and ensures that the system remains relevant in an increasingly interconnected global economy.

The role of governance cannot be overstated. A clear and transparent governance structure defines how the currency is issued, managed, and regulated. It establishes accountability, ensures compliance with legal standards, and provides mechanisms for resolving disputes. Effective governance fosters stability and confidence, encouraging both domestic and international stakeholders to engage with the system.

As the global financial landscape continues to evolve, the adoption of regulated digital currencies represents a strategic move toward more transparent and accountable economies. It reflects a commitment to modernizing financial infrastructure while upholding the principles of trust, security, and inclusivity. By embracing this approach, nations can strengthen their economic foundations and position themselves for sustainable growth in the digital age.

In the end, the true value of a regulated digital currency lies not only in its technological capabilities but in its ability to reinforce the relationship between institutions and the people they serve. It creates a financial environment where transparency is not an obligation but a built-in feature, where efficiency is not an aspiration but a reality, and where trust is not assumed but continuously earned.