As South Africa looks to deepen financial inclusion, it doesn’t need to start from scratch. Across the Global South, countries like Brazil (with PIX) and India (with UPI) have already built powerful models for expanding access to financial services offering practical lessons in how policy, infrastructure, and innovation can work together to reach underserved populations.

South Africa (with PayShap), despite having one of the continent’s most advanced financial systems, still faces a paradox: high banking penetration on paper, but persistent exclusion in practice. Millions remain underserved due to uneven access to credit, connectivity, and affordable financial tools.

The question, then, is not whether inclusion is possible but how to build systems that truly scale.

Infrastructure First: India’s Digital Stack Model

India’s fintech transformation didn’t begin with apps – it began with infrastructure.

At the core is a government-backed digital public infrastructure (DPI) stack, anchored by systems like

Aadhaar (digital identity),

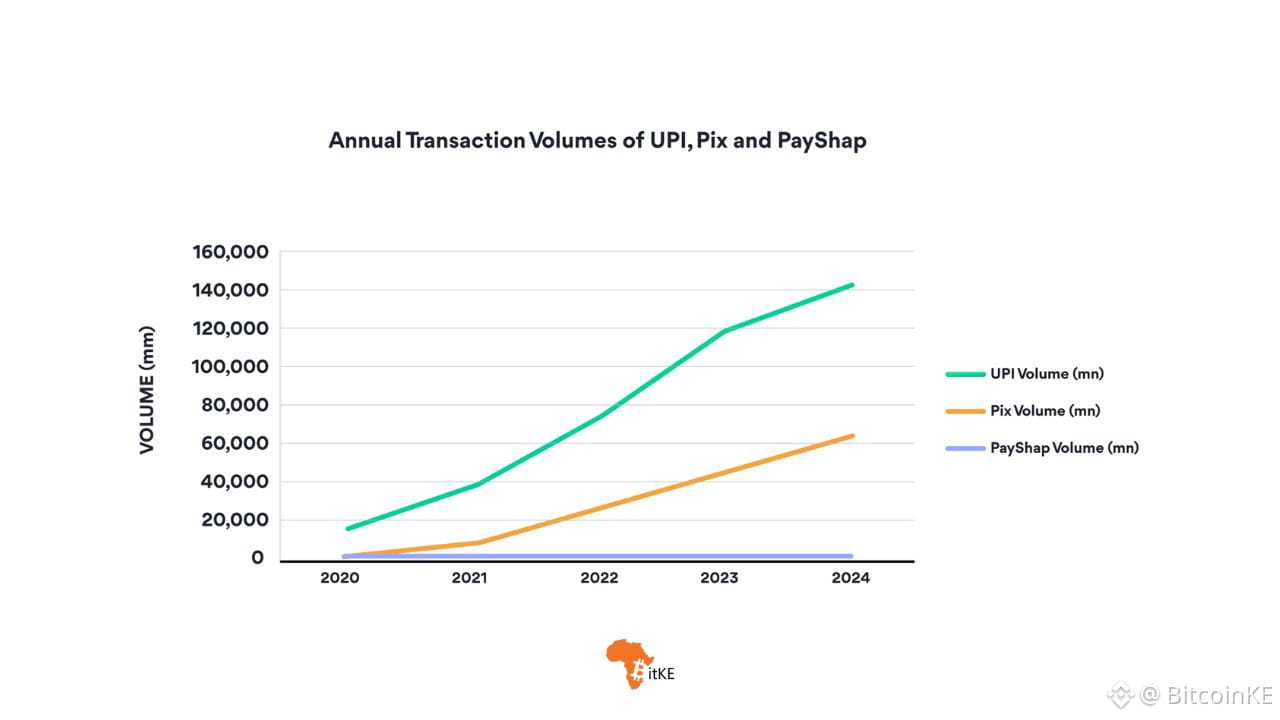

UPI (real-time payments), and

data-sharing frameworks.

Together, these layers reduced onboarding friction, lowered costs, and made financial services accessible to over a billion people.

The key insight: innovation thrives when the rails are already in place.

Rather than competing in silos, fintechs in India build on shared infrastructure – allowing startups to focus on products while the state ensures interoperability, identity verification, and trust. This dramatically accelerates inclusion and adoption.

For South Africa, where fragmented systems and high transaction costs still limit access, the lesson is clear: build interoperable public rails first, then let innovation flourish on top.

Brazil’s Playbook: Regulation as an Enabler

If India shows the power of infrastructure, Brazil demonstrates the importance of regulation done right.

Brazil’s central bank has taken a proactive role in shaping fintech innovation by rolling out instant payments (PIX), open banking frameworks, and clear licensing regimes. The result is a system where competition is encouraged, barriers are lowered, and consumers benefit from cheaper, faster services.

Crucially, regulation in Brazil is not reactive, it is coordinated, iterative, and designed to include new players from the outset.

This stands in contrast to many African markets where regulatory uncertainty can slow innovation or lock fintechs into legacy banking structures.

For South Africa, the takeaway is not deregulation, but smarter regulation – frameworks that balance risk with innovation while enabling non-bank players to participate meaningfully.

The Missing Middle: South Africa’s Opportunity

South Africa already has strong financial institutions, high mobile penetration, and a growing fintech ecosystem. But inclusion gaps persist because the system wasn’t originally designed for the digitally excluded.

Fintechs are beginning to fill that gap by building new payment rails, embedded finance solutions, and data-driven lending products tailored to underserved users.

Still, progress will depend on how well the broader ecosystem comes together.

Across Africa, the next phase of fintech growth will be driven less by individual startups and more by ecosystem collaboration – bringing together regulators, capital providers, telecoms, and technology platforms to create scalable, inclusive systems.

South Africa Reserve Bank Partners with Local Banks to Launch PayShap, a Low-Payments Mobile System

Three Lessons for South Africa

1.) Build shared infrastructure, not isolated solutions India’s success shows that digital identity, payments, and data frameworks should be public goods that everyone can build on.

2.) Treat regulation as a growth tool Brazil proves that clear, forward-looking regulation can unlock innovation rather than restrict it.

3.) Design for the underserved from day one Inclusion isn’t a byproduct—it must be intentional, with products tailored to real-world constraints like low connectivity, informal income, and limited credit history.

Financial inclusion is not just about access to banking – it’s about participation in the digital economy.

Fintech, when done right, becomes infrastructure: powering commerce, enabling entrepreneurship, and expanding opportunity at scale. Across Africa, it already serves as a bridge for millions who were previously excluded from formal financial systems.

South Africa has the building blocks. What Brazil and India offer is a blueprint – one that shows how coordination, infrastructure, and policy can turn potential into impact.

FINTECH AFRICA | How Digital Payment Systems Like PayShap Are Driving the Cashless Economy in South Africa

Stay tuned to BitKE for payment developments globally.

Join our WhatsApp channel here.

Follow us on X for the latest posts and updates

Join and interact with our Telegram community

_________________________________________