Last week, I had dinner with a lawyer friend who has been deeply engaged in the crypto compliance field in Singapore for 8 years. He said something that sent chills down my spine: “The attitude of Middle Eastern regulators towards @SignOfficial Sign now is almost identical to how the US SEC viewed Ripple in 2019. Both are stirring up compliance narratives with a pile of cooperation MOUs, and the market has inflated expectations to the sky, but the core regulatory qualitative issues of the tokens have been buried from the start.”

This statement awakened me. The crypto market has developed for more than a decade, and every bull market gives birth to a batch of projects that take off based on 'compliance narratives', but 90% of these projects ultimately fail on the road to realizing the narrative. From Ripple in 2017 to Chainlink in 2020, and now to Sign, the script of compliance narratives has never changed: opening up imagination through cooperation with traditional institutions/governments, using grand infrastructure narratives to drive up valuations, ultimately either realizing expectations into real performance and growing into industry giants, or becoming fleeting shadows in the market after the narrative collapses.

The current Sign stands at the crossroads of this cycle. Is it replicating Chainlink's path to success, or is it repeating Ripple's mistakes? I have gone through the rise and fall of all the leading projects in the compliance lane over the past decade, compared the core logic of the three, and finally see the true situation of Sign.

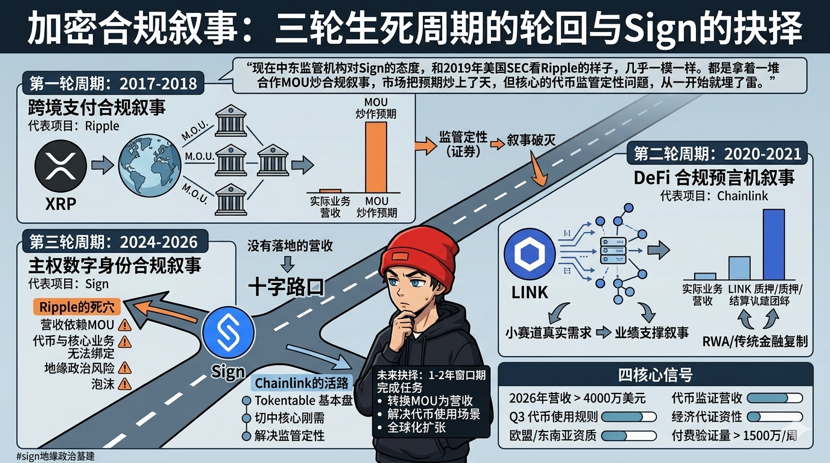

First, let's review the three rounds of life-and-death cycles of crypto compliance narratives to understand history before clarifying the present.

First round cycle: 2017-2018, cross-border payment compliance narrative, represented by Ripple. Back then, Ripple stirred its narrative of 'replacing SWIFT's cross-border payment infrastructure' to the extreme by signing cooperation MOUs with hundreds of banks worldwide. XRP rose from $0.006 to $3.84, with a market cap once reaching the second highest in the market. But ultimately, the bubble of the narrative burst: the vast majority of cooperation MOUs were merely intentions, with no substantial business landing, and annual revenue was less than 0.1% of market cap; more critically, the SEC directly classified XRP as a security, initiating a decade-long lawsuit, which completely collapsed the project's compliance foundation.

The lesson from Ripple has drawn a life-and-death line for all compliance narrative projects: without real landing revenue, no matter how grand the MOUs are, they are just waste paper; and no way to bypass the regulatory qualitative issues of tokens, no matter how perfect the narrative is, it is just a castle in the sand.

Second round cycle: 2020-2021, DeFi compliance oracle narrative, represented by Chainlink. Unlike Ripple, which stirs expectations with MOUs, Chainlink found genuine rigid demand from the very beginning: DeFi protocols need decentralized oracles to provide prices in order to function normally. It first established stable cash flow by landing its services in the narrow lane of DeFi, with a strong binding between the token and core business—nodes must provide oracle services and stake LINK as collateral, with service fees also settled in LINK, forming a perfect value loop.

After establishing a foothold in the DeFi lane, Chainlink replicated its compliance verification capabilities to RWA and traditional financial markets, securing collaborations with giants like BlackRock and Fidelity, growing from a DeFi price feeding tool to the compliance infrastructure of the global crypto market, with LINK rising from $0.8 to $52, still the industry leader today.

The success of Chainlink has pointed out the only way for compliance narrative projects to survive: first, establish real, profitable business in a small lane, create a closed loop of token value, and then replicate the capability to larger markets, supporting the narrative with performance rather than replacing performance with expectations.

Third round cycle: 2024-2026, sovereign digital identity compliance narrative, represented by the current Sign. The current Sign has shadows of both Ripple and Chainlink, half bubble and half hope.

It has three fatal similarities with Ripple back then: First, the core support for its valuation is the government cooperation MOUs, not the realized revenue. Currently, at a valuation of nearly $500 million for SIGN, at least 70% is based on expectations from Middle Eastern government projects, while the annual revenue contribution from government projects is less than 15% of total revenue, with the vast majority still at the intention stage, almost identical to Ripple's 'hundreds of bank MOUs' back then; Second, a strong binding between the token and core business, due to the inability to realize regulatory red lines. Government projects can only settle in fiat currency and dare not use SIGN for payments, fearing being regulated as securities, with the value support of the tokens relying solely on market expectations, without rigid use cases. This is also the most critical deadlock for Ripple back then; Third, business is highly concentrated in a single region, with extremely high geopolitical risks. Ripple's business back then was highly dependent on the US market, and a lawsuit from the SEC almost halted the project, while now 90% of Sign's compliance business is concentrated in the Middle East. Once geopolitical situations change or regulatory policies tighten, all collaborations could be instantly voided.

However, it has two critical similarities with Chainlink back then: First, it has a solid base that can make stable profits. Chainlink survived back then relying on DeFi oracles, while Sign is currently relying on Tokentable's token distribution business, which can secure $15 million in stable revenue each year, with a gross margin exceeding 70%. Even if all government collaborations fall through, it can survive on this base, unlike other vapor projects that would drop to zero immediately; Second, it addresses the core rigid demands of the crypto market. Chainlink hit the price feeding demand of DeFi, while Sign addresses the biggest pain point in the integration of the crypto market and the traditional world—compliance identity verification. Whether it is KYC for DeFi, asset confirmation for RWA, or compliance screening for cross-border trade, a set of identity solutions that balance privacy and compliance is needed. This market is at least ten times larger than the oracle market back then.

If you understand these, you will realize that the life and death of $SIGN is never determined by how many government MOUs it has, but by whether it can break out of the narrative trap of Ripple and successfully navigate the implementation path of Chainlink. It must accomplish three things within the 1-2 year narrative window: First, transform the compliance endorsement from government cooperation into a replicable SaaS product for cross-border trade and institutional compliance services, turning intended MOUs into stable, scalable revenue; Second, find a compliant way to complete the value loop of tokens and core business, resolving the regulatory qualitative deadlock; Third, break out of the narrow lane of the Middle East and open up the global markets of the EU and Southeast Asia, breaking the ceiling of geopolitical risks.

If it accomplishes one of these three things, it can survive; if it accomplishes two, it can grow into the industry leader; if it accomplishes all three, it can replicate Chainlink's hundredfold myth. But if it accomplishes none, it will end up like Ripple back then, becoming just another footnote in the narrative cycle of crypto compliance after the narrative collapses.

The four core signals I am currently focusing on are completely unrelated to PR press releases or price fluctuations: First, can annual revenue in 2026 exceed $40 million, with non-government business accounting for over 60%; Second, can the official announce rigid usage rules for compliant tokens before Q3, completing the value loop; Third, can compliance qualifications in the EU and Southeast Asia be established, with overseas revenue exceeding 20%; Fourth, can the effective paid verification volume across the entire chain stabilize at over 15 million per week. I will consider increasing my position if two out of the four signals exceed expectations; if all four fall short, I will wait until the August unlocking tide to make a decision.#BTC