Everyone......You wake up in the morning and send money to your family across the border in seconds without high fees or waiting days for banks to clear it. Or you pay for your groceries using a digital token that holds its value steady no matter what happens in the markets. That future is not some far-off dream anymore. It is happening right now through a smart mix of central bank digital currencies known as CBDCs and regulated stablecoins running on both public and private blockchain rails.

This new money system blends the trusted power of governments with the fast innovative spirit of private companies. It promises quicker payments stronger security and more choices for ordinary people like you and me. I have been following these developments closely and I truly believe this combination can unlock huge opportunities while keeping things safe and fair. Let me walk you through it all in a simple friendly way so you can see why it matters and how it can benefit your daily life.

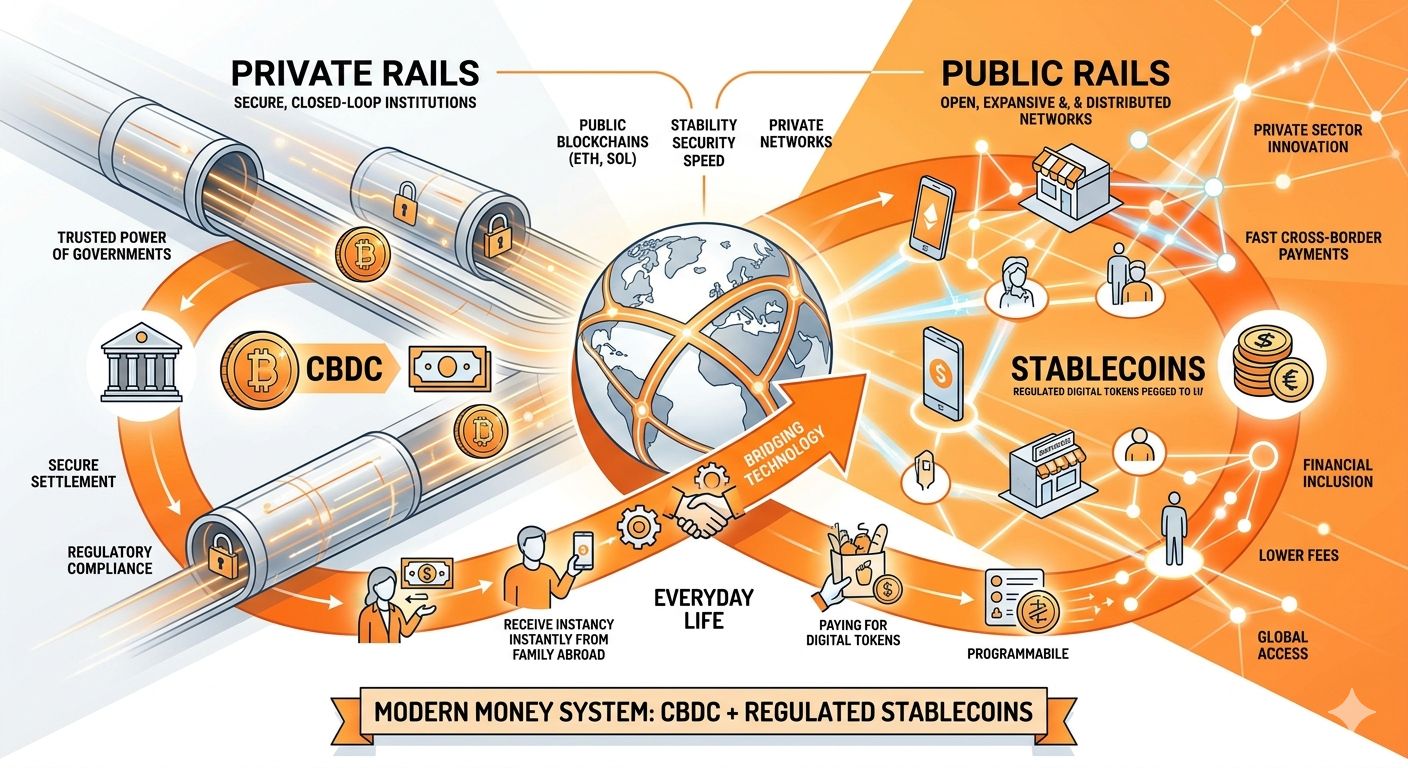

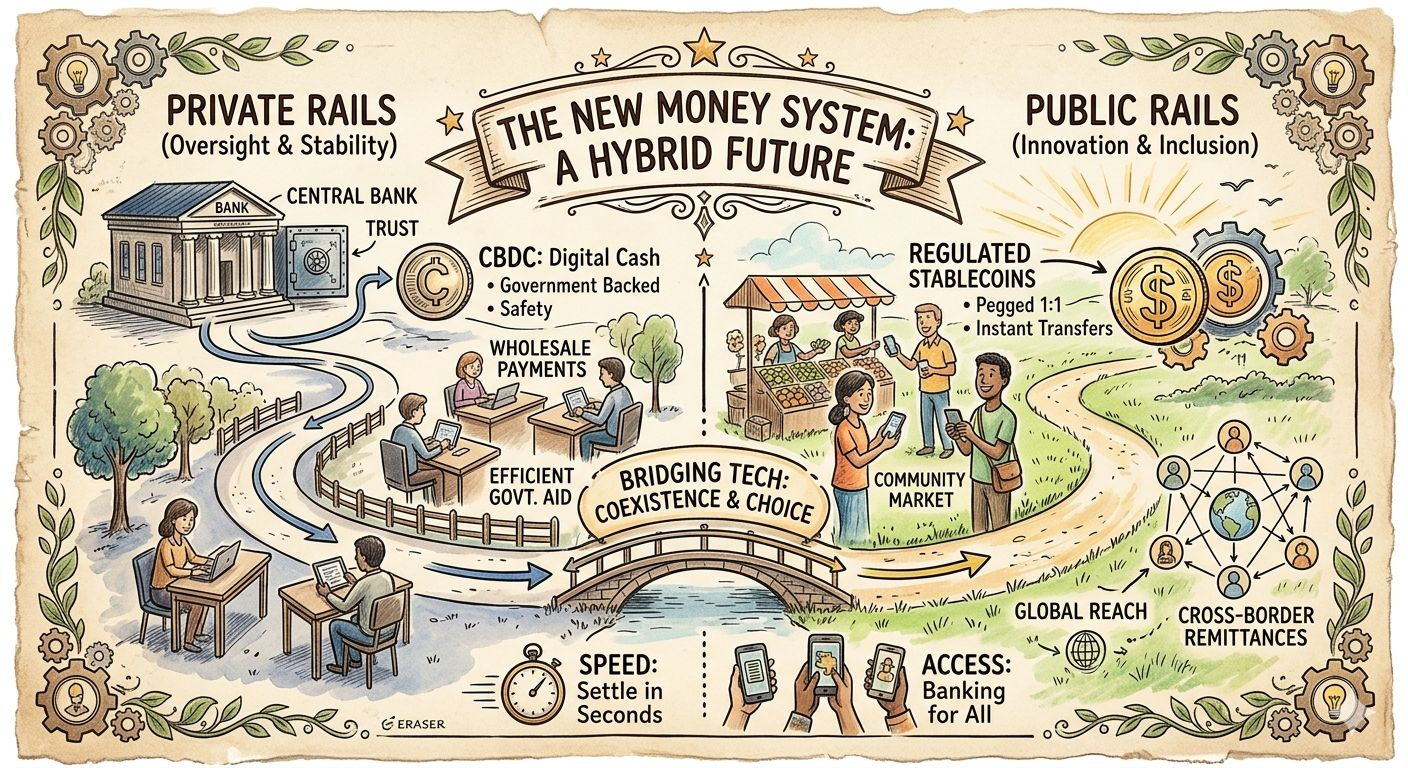

First let us understand what these terms really mean without any complicated jargon. A CBDC is basically digital cash issued directly by a country's central bank. Think of it as the electronic version of the physical notes and coins you carry in your wallet but with superpowers. It sits on the central bank's balance sheet so it carries the full trust and backing of the government. Many countries are testing or rolling out their own versions because they want to modernize payments and keep control over their currency in a digital world.

On the other side we have regulated stablecoins. These are digital tokens created by private companies but they are designed to hold a stable value usually pegged one-to-one with a real currency like the US dollar. The big ones like USDC from Circle or others backed by reserves in cash and safe government securities now operate under clear rules in places like the US and Europe. Regulation makes sure the issuers hold real assets to back every token so users do not have to worry about sudden crashes or losses.

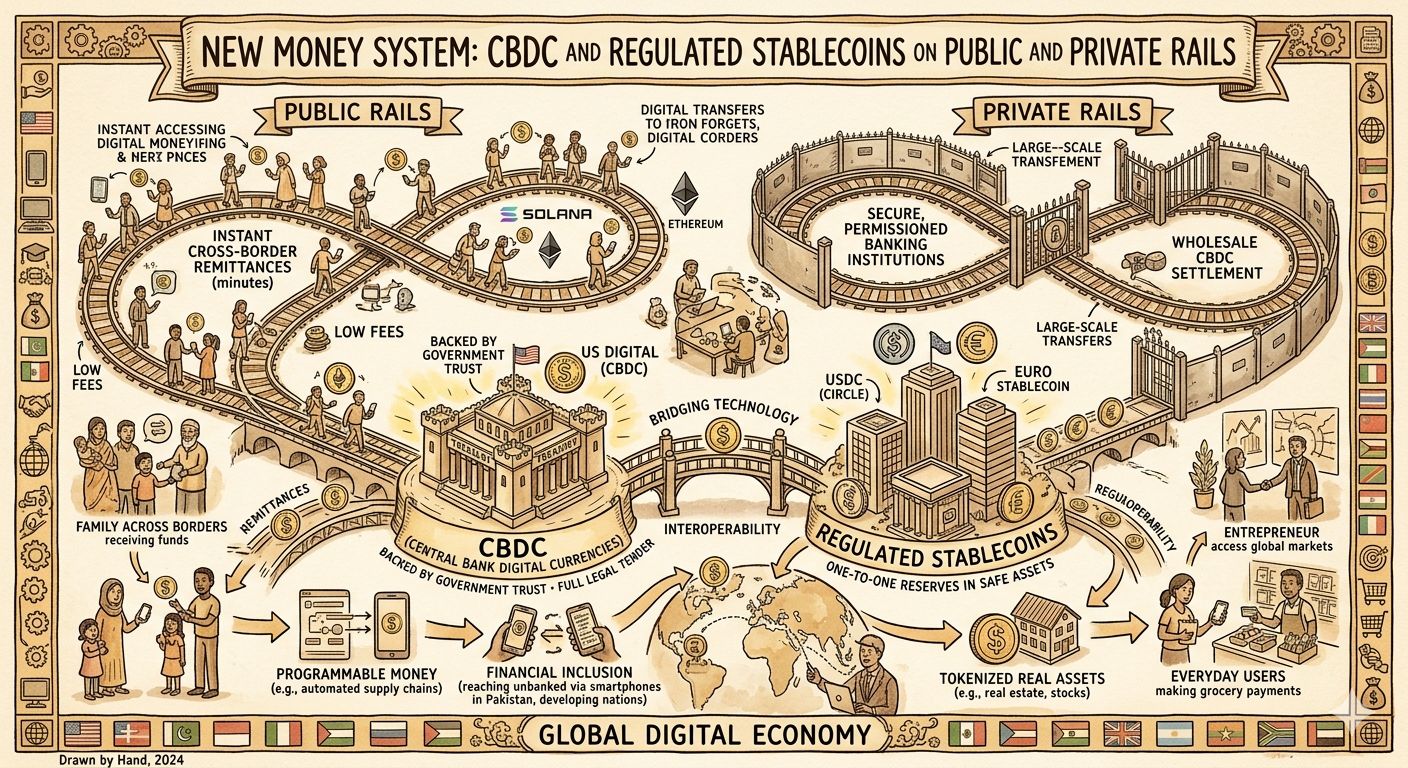

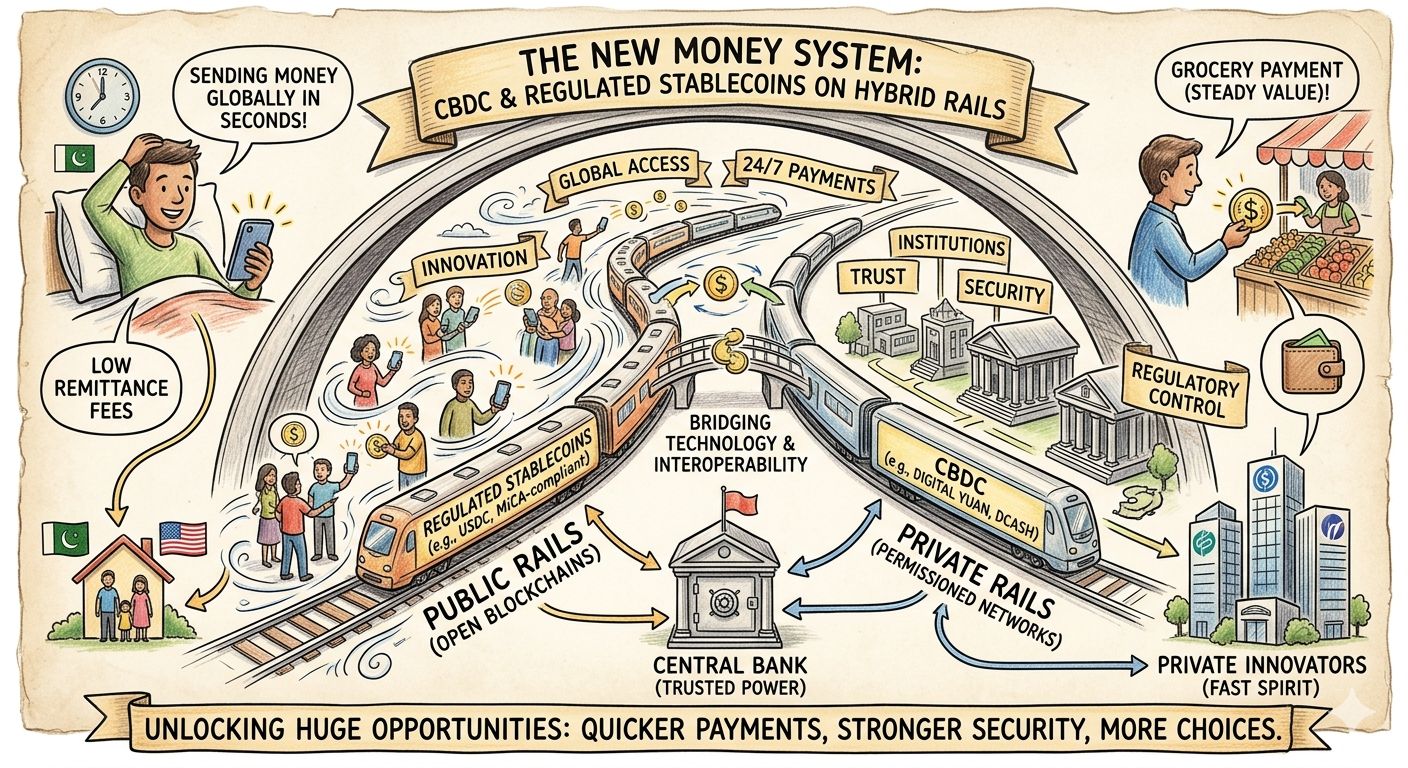

What makes this new system legendary is how it uses both public and private rails. Public rails mean open blockchains like Ethereum or Solana where anyone can join participate and build new things on top. These networks run 24 hours a day seven days a week and they allow lightning-fast transfers across borders with low costs. Private rails on the other hand are controlled networks often used by banks or governments for extra security and compliance. They keep sensitive transactions protected while still connecting smoothly to the public side.

Imagine a dual-path setup. You can send a regulated stablecoin on a public blockchain for everyday global use or settle big wholesale payments through a private CBDC rail for maximum safety. Bridging technology lets these two worlds talk to each other without friction. This hybrid approach gives the best of both worlds. Public rails bring innovation speed and inclusion while private rails add oversight stability and protection against risks.

Why does this matter so much for regular folks? Let me break it down with real benefits that touch your life directly. First comes speed. Traditional bank transfers especially international ones can take days and cost a lot in fees. With this new system payments settle in minutes or even seconds. Remittances to family back home become cheap and instant which is huge for millions of people in places like Pakistan or other developing countries.

Second is accessibility. Many people around the world still do not have bank accounts but almost everyone has a smartphone. CBDCs and stablecoins can reach them through simple digital wallets. Governments can distribute aid or subsidies directly into these wallets without middlemen leaking money away. Private stablecoins on public rails let small businesses accept payments from anywhere in the world without setting up complicated banking relationships.

Third comes programmability. This is where things get really powerful. Money can now have built-in rules. For example a company could program a stablecoin payment that only releases when certain conditions are met like delivery of goods in a supply chain. Or a government could design CBDC features for targeted support like food vouchers that only work at approved stores. This smart money reduces fraud and makes everything more efficient.

Fourth is stability and trust. Regulated stablecoins must hold real reserves and report them transparently so users know the value will not swing wildly. CBDCs go even further because they are direct claims on the central bank which is as safe as it gets. Together they reduce the risks we see in unregulated crypto while keeping the advantages of blockchain like transparency and immutability.

Let us look at some real-world examples to make this concrete. China has been a pioneer with its e-CNY digital yuan which is a retail CBDC used by millions for everyday payments. It runs on a hybrid system that allows controlled access while experimenting with programmability. In the Eastern Caribbean they launched DCash a CBDC that helps with financial inclusion across islands.

On the stablecoin side the US passed the GENIUS Act in 2025 which created clear federal rules for payment stablecoins. Issuers like Circle with USDC now follow strict guidelines on reserves audits and compliance. This has boosted confidence and growth with the stablecoin market already handling billions in daily transactions for trading remittances and even traditional finance settlements. Europe has its MiCA regulation that treats certain stablecoins like electronic money giving them a safe legal framework.

Banks are getting in on the action too. Big players like JP Morgan have tokenized deposits on their own private chains but some are exploring public networks for broader reach. Projects like mBridge bring central banks together to test cross-border CBDC settlements showing how public-private cooperation can make global trade smoother.

Now the beauty of running these on mixed rails is the flexibility. Stablecoins shine on public blockchains because they tap into a massive ecosystem of decentralized apps wallets and services. Anyone with an internet connection can use them without asking permission. CBDCs often prefer permissioned private rails for wholesale use among banks to ensure high security and regulatory control. But modern designs allow bridging so a user can start with a stablecoin payment on public rails and settle ultimately in central bank money on private rails if needed.

This setup also helps with tokenization of real assets. Think real estate stocks or bonds turned into digital tokens that trade 24/7 with instant settlement. Regulated stablecoins or CBDCs act as the reliable medium of exchange in these new markets cutting out delays and counterparty risks that plague old systems.

Of course no big change comes without challenges and it is important to talk about them honestly. Privacy is a hot topic. With CBDCs governments could in theory see more transaction data which raises concerns about surveillance. Good designs include privacy features like tiered anonymity where small payments stay private but large ones get monitored for compliance. Regulated stablecoins on public rails offer more pseudonymity but still follow anti-money laundering rules through issuers.

Another risk is financial stability. If stablecoins grow too fast without proper backing or if there is a sudden rush to redeem them it could strain reserves or linked banks. That is why regulation like requiring one-to-one high-quality assets and regular audits is so crucial. CBDCs avoid some of these issues because they are sovereign money but they need careful rollout to avoid disrupting commercial banks.

Cybersecurity matters too. Blockchains are generally secure but hacks on wallets or bridges have happened. The new system counters this with better standards multi-factor security and insurance options. Inclusion is key as well. We must make sure elderly people or those in remote areas can use these tools easily through user-friendly apps and education.

Cross-border issues add another layer. A world full of different CBDCs needs interoperability standards so they can talk to each other. Stablecoins especially dollar-pegged ones already provide a practical bridge but countries worry about losing monetary sovereignty if foreign stablecoins dominate locally. The solution seems to be coexistence with strong local options and international agreements.

Despite these hurdles the upsides look massive. Experts see stablecoins growing from hundreds of billions today toward trillions in the coming years thanks to regulation that builds trust. CBDC pilots continue in over a hundred countries focusing on better domestic payments and inclusion. When combined on hybrid rails they can modernize everything from government disbursements to corporate treasury management.

For businesses this means lower costs faster cash flow and new ways to innovate like programmable payroll or automated supplier payments. For governments it offers better tools to manage money supply fight inflation and reach citizens directly. For everyday people like us it means more freedom choice and efficiency in handling our finances.

I am genuinely optimistic because this is not about replacing old money but upgrading it for the digital age. Cash and bank accounts will still have their place but the new layers will handle what they do best. Public rails fuel creativity and global access while private rails protect stability and compliance. The regulated part ensures we avoid the wild west problems of early crypto.

Think about the impact in emerging markets. In places with high remittance needs or limited banking infrastructure a regulated stablecoin on public rails can bring instant low-cost transfers. A CBDC can then provide a safe local anchor. Together they reduce dollarization risks while still allowing global participation.

Even in developed economies the benefits shine. Faster settlement in capital markets means less trapped capital and more productive use of funds. Tokenized assets backed by stable digital money can open investment opportunities to more people with smaller amounts.

As this system evolves we will likely see more hybrid products. Maybe a stablecoin backed by a basket including CBDC reserves or private rails that connect seamlessly to public ones for retail use. Innovation will keep coming from both public institutions and private players working side by side.

What excites me most is the potential for true financial inclusion and empowerment. When money moves freely safely and cheaply more people can participate in the global economy. Small entrepreneurs can compete better. Families can support each other across distances without losing a big chunk to fees. Governments can deliver help more effectively during crises.

Of course success depends on smart balanced regulation that encourages innovation without stifling it. It also needs education so everyone understands how to use these tools securely. International cooperation will be important to set standards that prevent fragmentation while respecting national needs.

Looking ahead I see a monetary system that is more resilient adaptable and user-focused. CBDCs provide the trusted public foundation while regulated stablecoins add private sector agility on open rails. The combination on public and private infrastructure creates a robust network that serves everyone from individuals to giant institutions.

This is the new money system taking shape right before our eyes. It is friendly to users powerful in capability and full of promise for a better financial future. If we get the details right it can reduce poverty speed up growth and bring transparency where it is needed most.

I hope this overview has sparked your interest and shown you why this topic deserves attention. Whether you are an everyday saver a business owner or just curious about technology the changes ahead will affect us all. Stay informed experiment safely with small steps and keep an open mind. The rails are being built now and the journey looks incredibly exciting.

The future of money is here and it is being shaped by CBDC and regulated stablecoins working together on public and private rails. Embrace it wisely and it can open doors you never imagined. Let us watch this evolution unfold and make the most of the opportunities it brings for all of us.!!!