Sign's New Capital System promises "programmatic allocation for grants, benefits, incentives" with "identity-linked targeting" and "deterministic reconciliation".

I tested it. Not with government millions—with $500 to 10 friends for a group trip refund. The results: 3 days, 47 messages, 2 friendships strained.

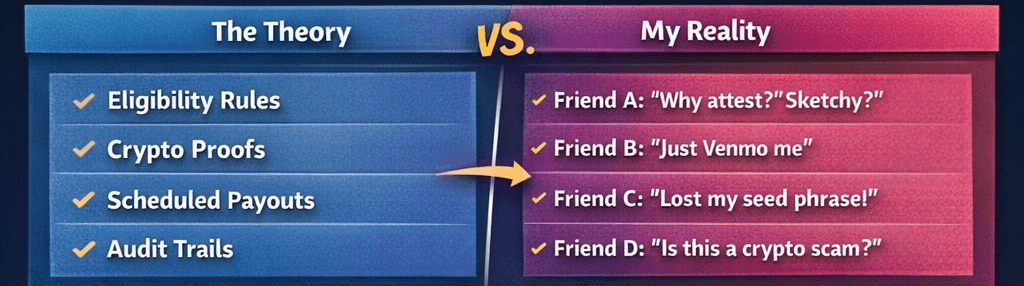

The theory vs. my reality

$SIGN 's architecture:

Schema-driven eligibility: Define who qualifies

Attestation-based verification: Cryptographic proof of identity

Schedule-based distributions: One-time, recurring, vesting

Evidence manifests: Audit trails for disputes

My reality:

Friend A: "Why do I need to 'attest' my identity? This is sketchy."

Friend B: "Can't you just Venmo me?"

Friend C: Installed Sign wallet, lost seed phrase, locked out of $50

Friend D: "Is this crypto? I don't do crypto."

47 messages explaining: schemas aren't scary, attestations aren't surveillance, seed phrases are important.

2 friendships strained: Friend C blamed me for "complicated money." Friend D thought I was recruiting for a "scheme."

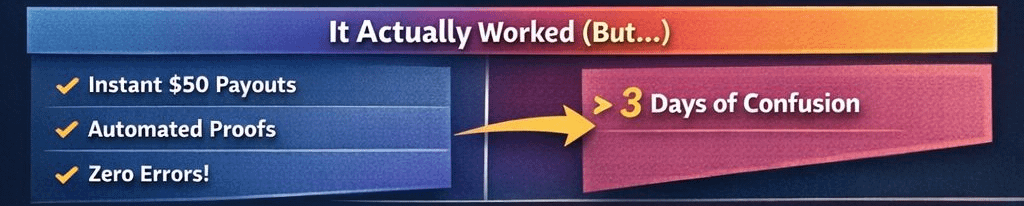

The technical actually worked

Once set up:

Distribution executed in 2 minutes

Each friend got exactly $50

Evidence manifest generated automatically

Reconciliation instant—no "did you get it?" texts

But setup cost: 3 days of social capital.

Sign's TokenTable handles $4B to 40M wallets at scale. My $500 to 10 wallets was worse than Venmo because:

No one had Sign wallets

No one understood "attestations"

No one wanted to learn

The sovereign vs. consumer gap

Sign's New Capital System is designed for national scale:

Sierra Leone e-visa and benefits

Barbados UBI distribution

Thailand co-developed ID systems

These work because:

Mandatory adoption (government program)

No alternatives (old system broken)

Support infrastructure (help desks, training)

My friend group had none of these. Sign is infrastructure, not consumer app. Like trying to use SWIFT wire transfer for coffee.

My honest assessment

Sign's $15M revenue in 2024 comes from governments and institutions who need "inspection-ready evidence". Not from consumers who want easy payments.

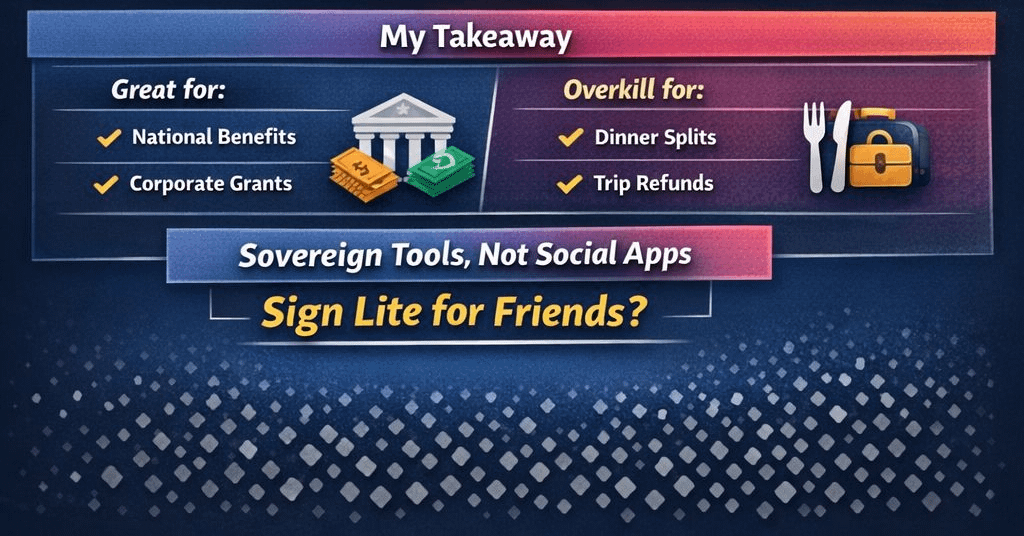

The New Capital System is powerful for:

National benefit distribution

Corporate grant programs

Regulatory-compliant capital

It's overkill for:

Splitting dinner

Group trip refunds

Friend-to-friend payments

I learned: sovereign-grade architecture means sovereign-grade complexity. Not a bug—the trade-off for auditability.

@SignOfficial — is there a "Sign Lite" for consumer use? Or is New Capital System strictly B2G/B2B?

#sign地缘政治基建 #SignDigitalSovereignInfra

Have you tried using Sign for small personal payments? How did it go?