The conflict with Iran may go down in history as a turning point for the petrodollar — this conclusion is contained in a report by the Deutsche Bank Research Institute dated March 24, 2026, prepared by bank analyst Mallika Sachdeva.

Petrodollar: the history of the deal

The dollar remains the world's reserve currency for one simple reason: the world pays for global goods and services in dollars and is willing to hold accumulated surpluses in dollar assets. Until 1971, the dollar was backed by gold — under the Bretton Woods system, central banks could exchange $35 for an ounce of gold at the Fed. After the U.S. abandoned the gold standard, the dollar transitioned to a fiat currency, relying on the creditworthiness of the American government.

The key anchor of the system has been the petrodollar. In 1974, Saudi Arabia agreed with Washington: oil is quoted in dollars, surpluses are invested in U.S. government bonds—in exchange for military security guarantees. The entire Gulf Cooperation Council (GCC) followed this model. Since oil is a basic resource for the global industry and transportation, global supply chains had a natural incentive to switch to the dollar, and global savings began to accumulate in U.S. currency.

Cracks that appeared before the war

The system had been experiencing failures even before the conflict between the U.S., Israel, and Iran began. Deutsche Bank highlights four key shifts:

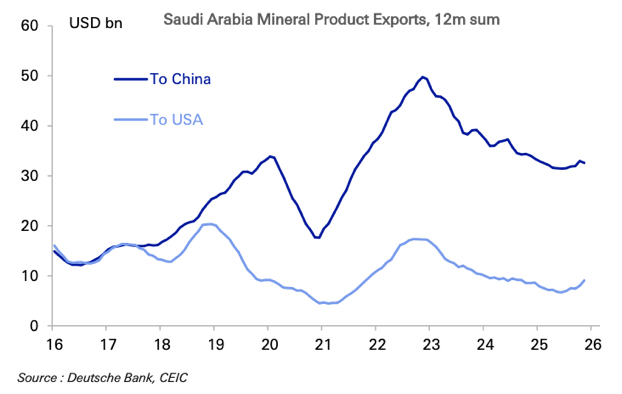

The U.S. has ceased to be the largest buyer of Middle Eastern oil. Thanks to the shale revolution, America has achieved energy independence, and Saudi Arabia has begun selling China four times more oil than the U.S. Today, 85% of Middle Eastern crude oil goes to Asia, and Beijing is increasingly insisting on switching transactions to yuan.

Riyadh is pursuing the localization of its defense industry. As part of 'Vision 2030', Saudi Arabia has set a goal to increase the share of domestic production in military expenditures to 50%, reducing dependence on imported weapons.

Saudi Arabia joined the mBridge project and signed swap lines with China. The mBridge project is a blockchain-based infrastructure that allows payments in the digital currencies of the central banks of participating countries without using the dollar correspondent network and SWIFT. The infrastructure for settlements bypassing the dollar has already been built.

Sanctions against Russia and Iran have pushed a significant part of the oil trade outside the dollar system. Transactions were conducted in rubles, yuan, and rupees using alternative payment mechanisms.

What the current conflict has added

The war has exposed new vulnerabilities of the petrodollar in several directions.

First, the American 'security umbrella'—a central element of the 1974 agreement—has been openly tested: U.S. military bases and oil infrastructure in the Persian Gulf have come under attack in a war that began with an American military operation in the region.

Secondly, the passage of oil tankers through the Strait of Hormuz was ensured not by American naval protection but by bilateral diplomacy. Some vessels heading to China, India, and Japan received passage rights precisely through direct negotiations.

Thirdly—and this is perhaps the most significant—reports are coming in that Iran is negotiating with eight states to grant passage through the Strait of Hormuz in exchange for payment for oil in yuan. If this scheme solidifies, the conflict could become a catalyst for weakening the dominance of the petrodollar and the beginning of the era of oil in yuan.

Mitigating factors

The authors of the report acknowledge that the dollar has protective mechanisms. The U.S., having lost the status of the largest buyer of Middle Eastern oil, could take the place of the world's main supplier. If Washington establishes control over the oil resources of the Western Hemisphere—directly or through allies—American reserves will exceed OPEC's stocks, allowing the U.S. to dictate the terms of global hydrocarbon trade.

In an optimistic scenario, the dollar retains its dominance in oil transactions provided that the U.S. controls a large part of the global supply. In a pessimistic scenario—fragmentation occurs: Middle Eastern oil, passing through Hormuz to Asia, is quoted in yuan, while oil from the Western Hemisphere remains in dollars.

The countries of the Gulf Cooperation Council remain deeply integrated into the dollar system: they have pegged their currencies to the dollar and hold vast reserves in U.S. currency. Any signs of a departure from dollar revenues could provoke attacks on these pegs. However, the war itself may force Gulf states to use dollar reserves domestically: damage to oil and civil infrastructure will require domestic investments. According to Global SWF, the Middle East and North Africa (MENA) region has approximately $2 trillion in central bank reserves and around $6 trillion in sovereign funds—but if these funds begin to be redirected to domestic needs, the barrier for currency changes will decrease.

Moving away from oil is a risk no less significant

Deutsche Bank sees the greatest long-term threat to the petrodollar not in a change of the currency of transactions, but in a possible global rejection of tradable fossil fuels. The parallels with the 1970s are obvious: the current conflict is already the second major energy shock of the decade after the start of the Ukrainian conflict in 2022. The oil embargo of 1973 pushed Western economies to diversify energy sources, create strategic oil reserves, and make initial investments in renewable and nuclear energy.

Regions dependent on imported energy resources—Europe, Asia, and the Global South—today have three paths: increasing production of their own fossil fuels, accelerating the transition to renewable energy, and betting on nuclear energy. The latter option, according to the authors, is the only one that provides genuine energy independence—even if it requires years of investment. China, which produces 80% of the world's solar panels, 70% of wind turbines, and 70% of lithium batteries, has already taken a strategic position in this market.

The U.S., having become energy independent, will suffer less from such a shift and will likely maintain its focus on fossil fuels. However, if the rest of the world reduces its dependence on global hydrocarbon trade, it will open up space for pricing goods and services in other currencies.

Conclusion: long-term losses for the dollar

In the short term, U.S. energy independence provides the dollar with a certain 'safe haven' premium. However, rising military expenditures, as well as the sale of U.S. government bonds by Asian and Middle Eastern players to protect their own currencies, negate this advantage—the dollar has hardly strengthened even in the acute phase of the crisis.

The long-term consequences will be more significant. A world striving for self-sufficiency in defense and energy will hold fewer dollar reserves. The strategic role of the Middle East for the dollar's status as the world's reserve currency is immeasurable—and this is what makes the current conflict a particularly serious test for the entire petrodollar system.

#war #iran #usa #dollar #Write2Earn