You are sitting at a poker table.

You have a good hand and are contemplating your next bidding strategy. But just a second before you play your card, the dealer sitting diagonally across from you quietly turns over your cards for everyone to see, then quickly flips them back and continues the game as if nothing happened.

Your opponents know your hole cards in advance but pretend that nothing has happened. And everyone at this table, including the dealer, refers to this as "part of the rules."

This is not a fictional story.

This is the reality that every user participating in Ethereum DeFi is experiencing today, though most of them are unaware. This phenomenon has a specific term: Maximal Extractable Value, or MEV.

Your transactions, their gold mine

To understand MEV, one must first understand Ethereum's transaction mechanism.

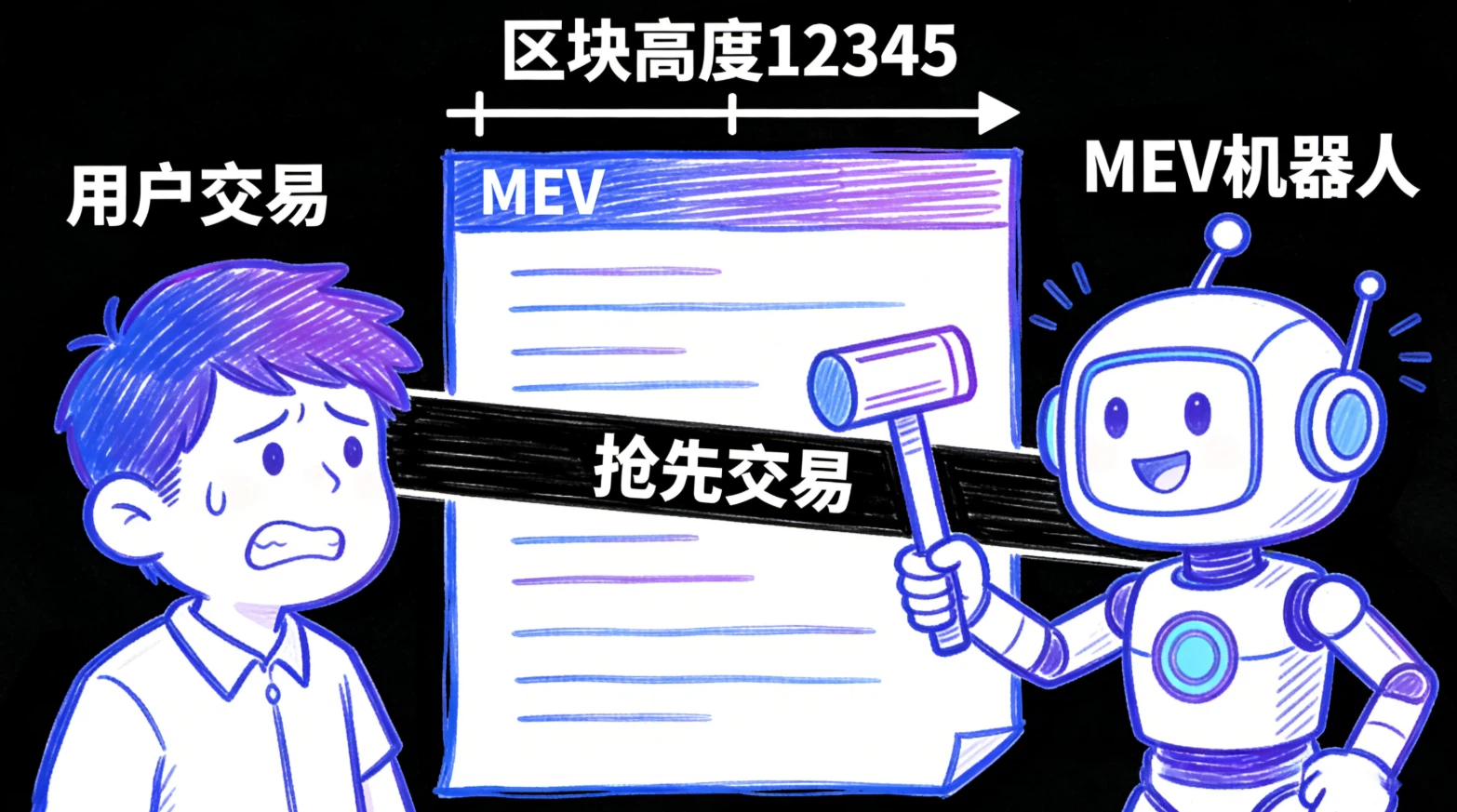

When you initiate a transaction on Ethereum, whether it's buying a token, providing liquidity to Uniswap, or liquidating an under-collateralized loan position, that transaction will not be immediately packed into the blockchain. It will first enter a waiting area called the 'memory pool' (mempool), where it waits for miners or validators to select it and include it in the next block.

The problem is that this memory pool is completely public. Anyone can view all pending transactions in real-time, including the initiator, target address, amount, and the transaction fees. For ordinary users, this is just a technical detail. But for those running dedicated listening programs known as 'arbitrage bots', this is a gold mine.

When an arbitrage bot detects a large pending buy order in the memory pool, such as your intention to buy a token with $10,000 on Uniswap, it will immediately initiate a transaction with a higher fee to buy that token in the same liquidity pool ahead of you. This front-running trade will drive up the token price, and when your buy order is executed, you will receive fewer tokens than expected at a higher price than anticipated. The bot then sells, pocketing the difference. The entire process occurs within the same block, smoothly and precisely, making it hard to detect.

This strategy is known in the industry as a 'sandwich attack' or 'front-running.' Data from Flashbots Research shows that in 2021 alone, Ethereum users paid over $700 million extra due to MEV. This money was not evaporated; it was transferred from ordinary users' pockets to the accounts of bot operators.

The Achilles' heel of transparent chains

The root of the MEV problem is fundamentally the structural flaw of transparent chains. When all transaction information is publicly visible, it inevitably creates opportunities for asymmetric information. Those with faster computing power and more sophisticated programs can exploit this information advantage to extract value from ordinary users.

The Ethereum community has proposed various mitigation solutions. Flashbots has built a private trading channel that allows users to submit transactions directly to validators, bypassing the public memory pool and avoiding detection by bots. The EIP-1559 fee reform changed the way transaction fees are calculated, reducing the generation of certain types of MEV to some extent. The Ethereum 2.0 PBS (Proposer-Builder Separation) mechanism aims to reduce the space for generating MEV from the underlying logic of block construction.

These solutions have had some effect, but they all share a common limitation: they are patching within the framework of transparent chains and do not fundamentally address the issue of information disclosure. As long as transaction information is visible before being packed into a block, there will always be a risk of front-running, just with differing probabilities and costs.

The idea of Midnight: Flip the table

@MidnightNetwork chose a completely different solution path: making transaction information in the memory pool invisible to the outside.

On the Midnight network, the contents of transactions submitted by users are encrypted to external observers until they are finally confirmed. Through the Kachina zero-knowledge proof system, the network can verify the legitimacy of a transaction, such as whether the trading party has sufficient balance, without exposing any specific transaction details. Arbitrage bots cannot listen to a pending buy order, and therefore cannot initiate front-running trades.

The practical significance of this design for DeFi users is quantifiable. Early testing data from ZSwap indicates that token swaps conducted on Midnight have reduced slippage by about 30% to 50% compared to equivalent Ethereum transactions. This means users are effectively paying less in fees and obtaining better execution prices.

This is not a small improvement but a structural upgrade to the DeFi user experience.

Who will be the biggest beneficiary

The impact of the MEV issue on ordinary retail investors is relatively limited, with each transaction potentially incurring extra costs of dozens to hundreds of dollars. But for institutional traders, the scale of this issue is entirely different. A market maker executing thousands of trades daily on DeFi could accumulate MEV costs amounting to millions of dollars.

This also explains why institutional users are much more interested in privacy chains like Midnight than retail investors. It is not because institutions care more about the concept of privacy, but because the cost savings from MEV protection have direct financial implications for institutions. When a trading institution discovers it can execute the same trading strategy on Midnight while paying 30% less in slippage costs, that is a purely commercial motivation.

The MEV crisis is the catalyst for Midnight

From the perspective of industry trends, the MEV crisis is a strong external catalyst driving the demand for privacy chains. It has transformed privacy needs from a 'conceptual appeal' into a 'rigid demand backed by concrete financial losses.'

Midnight's positioning in this context is more advantageous than many realize. It is not just a 'privacy protection' project; it is also an infrastructure that can address the actual financial pain points of DeFi users. The issue of MEV will not completely disappear due to Ethereum's fixes, as those solutions do not address the fundamental problem of information transparency.

At this poker table, the dealer has flipped your cards too many times.

What Midnight offers is the opportunity to change the table.