Anndy Lian

Why your portfolio is down: The Fed’s hawkish hold explained

The Federal Reserve delivered a sobering message that sent shockwaves through equities, cryptocurrencies, and commodities alike. Chair Jerome Powell and the Federal Open Market Committee kept interest rates steady at 3.50 per cent to 3.75 per cent, but simultaneously raised their 2026 inflation forecast to 2.7 per cent from the previous 2.4 per cent projection. This hawkish hold shattered hopes for aggressive monetary easing and forced investors to recalibrate their expectations for the remainder of the year.

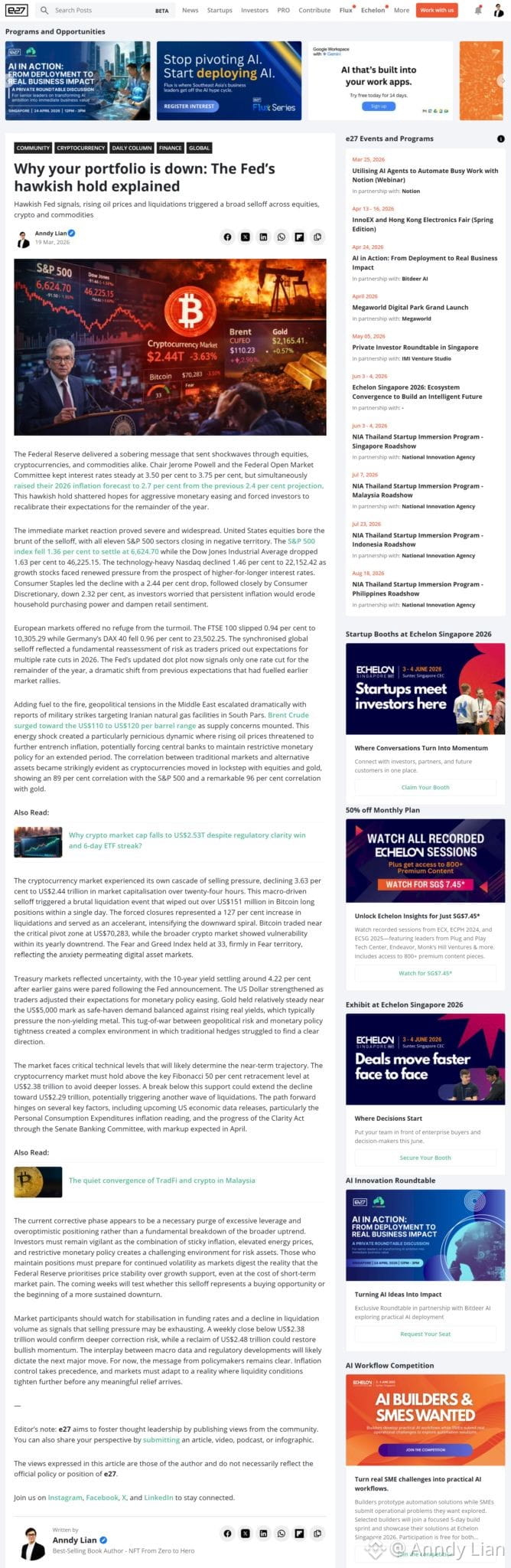

The immediate market reaction proved severe and widespread. United States equities bore the brunt of the selloff, with all eleven S&P 500 sectors closing in negative territory. The S&P 500 index fell 1.36 per cent to settle at 6,624.70 while the Dow Jones Industrial Average dropped 1.63 per cent to 46,225.15. The technology-heavy Nasdaq declined 1.46 per cent to 22,152.42 as growth stocks faced renewed pressure from the prospect of higher-for-longer interest rates. Consumer Staples led the decline with a 2.44 per cent drop, followed closely by Consumer Discretionary, down 2.32 per cent, as investors worried that persistent inflation would erode household purchasing power and dampen retail sentiment.

European markets offered no refuge from the turmoil. The FTSE 100 slipped 0.94 per cent to 10,305.29 while Germany’s DAX 40 fell 0.96 per cent to 23,502.25. The synchronised global selloff reflected a fundamental reassessment of risk as traders priced out expectations for multiple rate cuts in 2026. The Fed’s updated dot plot now signals only one rate cut for the remainder of the year, a dramatic shift from previous expectations that had fuelled earlier market rallies.

Adding fuel to the fire, geopolitical tensions in the Middle East escalated dramatically with reports of military strikes targeting Iranian natural gas facilities in South Pars. Brent Crude surged toward the US$110 to US$120 per barrel range as supply concerns mounted. This energy shock created a particularly pernicious dynamic where rising oil prices threatened to further entrench inflation, potentially forcing central banks to maintain restrictive monetary policy for an extended period. The correlation between traditional markets and alternative assets became strikingly evident as cryptocurrencies moved in lockstep with equities and gold, showing an 89 per cent correlation with the S&P 500 and a remarkable 96 per cent correlation with gold.

The cryptocurrency market experienced its own cascade of selling pressure, declining 3.63 per cent to US$2.44 trillion in market capitalisation over twenty-four hours. This macro-driven selloff triggered a brutal liquidation event that wiped out over US$151 million in Bitcoin long positions within a single day. The forced closures represented a 127 per cent increase in liquidations and served as an accelerant, intensifying the downward spiral. Bitcoin traded near the critical pivot zone at US$70,283, while the broader crypto market showed vulnerability within its yearly downtrend. The Fear and Greed Index held at 33, firmly in Fear territory, reflecting the anxiety permeating digital asset markets.

Treasury markets reflected uncertainty, with the 10-year yield settling around 4.22 per cent after earlier gains were pared following the Fed announcement. The US Dollar strengthened as traders adjusted their expectations for monetary policy easing. Gold held relatively steady near the US$5,000 mark as safe-haven demand balanced against rising real yields, which typically pressure the non-yielding metal. This tug-of-war between geopolitical risk and monetary policy tightness created a complex environment in which traditional hedges struggled to find a clear direction.

The market faces critical technical levels that will likely determine the near-term trajectory. The cryptocurrency market must hold above the key Fibonacci 50 per cent retracement level at US$2.38 trillion to avoid deeper losses. A break below this support could extend the decline toward US$2.29 trillion, potentially triggering another wave of liquidations. The path forward hinges on several key factors, including upcoming US economic data releases, particularly the Personal Consumption Expenditures inflation reading, and the progress of the Clarity Act through the Senate Banking Committee, with markup expected in April.

The current corrective phase appears to be a necessary purge of excessive leverage and overoptimistic positioning rather than a fundamental breakdown of the broader uptrend. Investors must remain vigilant as the combination of sticky inflation, elevated energy prices, and restrictive monetary policy creates a challenging environment for risk assets. Those who maintain positions must prepare for continued volatility as markets digest the reality that the Federal Reserve prioritises price stability over growth support, even at the cost of short-term market pain. The coming weeks will test whether this selloff represents a buying opportunity or the beginning of a more sustained downturn.

Market participants should watch for stabilisation in funding rates and a decline in liquidation volume as signals that selling pressure may be exhausting. A weekly close below US$2.38 trillion would confirm deeper correction risk, while a reclaim of US$2.48 trillion could restore bullish momentum. The interplay between macro data and regulatory developments will likely dictate the next major move. For now, the message from policymakers remains clear. Inflation control takes precedence, and markets must adapt to a reality where liquidity conditions tighten further before any meaningful relief arrives.

Source: https://e27.co/why-your-portfolio-is-down-the-feds-hawkish-hold-explained-20260319/

The post Why your portfolio is down: The Fed’s hawkish hold explained appeared first on Anndy Lian by Anndy Lian.