ETH2,044.18+1.90%

ETH2,044.18+1.90%The largest private credit funds have frozen withdrawals, forcing investors to sell liquid assets — including Bitcoin and Ethereum.

The Fed meeting on March 17-18 intensifies pressure: Powell's hawkish tone may accelerate the flight from risk.

Institutional investors are actively hedging — open interest in put options on credit ETFs reached a record 11,5 million contracts.

The five largest private credit fund managers have frozen or restricted withdrawals since the end of February. Amid reduced liquidity, investors who cannot withdraw funds may begin to sell more liquid assets — including bitcoin (BTC) and Ethereum (ETH).

The situation is exacerbated by timelines — the Federal Open Market Committee (FOMC) meeting will take place on March 17–18. Bitcoin declined after seven of the eight FOMC meetings in 2025. The fear and greed index currently indicates an extreme level of fear, and crypto markets remain the weakest since 2022 — just before the week of the rate decision.

How closed credit funds reduce liquidity in the crypto market

The wave of withdrawal restrictions in private credit funds began with Blue Owl Capital and then affected BlackRock, HPS, Cliffwater, and Morgan Stanley.

Restrictions trigger a chain reaction: as soon as one fund blocks withdrawals, investors rush to withdraw funds from others — until they too implement similar measures.

The flagship fund Cliffwater worth $33 billion allowed only 7% to be withdrawn, although investors attempted to take out a record 14% for the quarter.

The fund satisfied only half of the requests. North Haven Private Income Fund from Morgan Stanley paid out only $169 million, which is about 45.8% of the requested amount — after the withdrawal limit was set at 5% of shares.

Those who cannot access their capital in such funds have to look for money in other assets. Bitcoin and Ethereum — the most liquid and risky instruments among those available to large participants — become the obvious choice for selling.

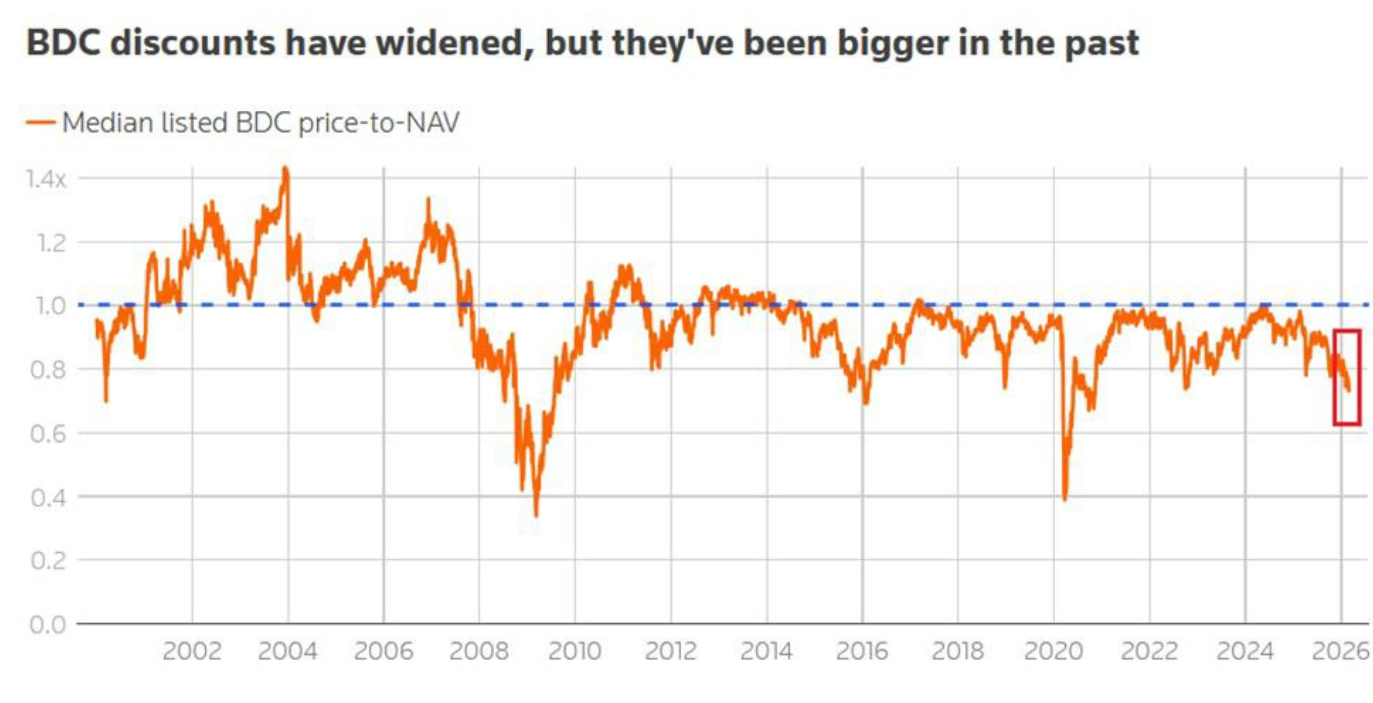

Debts of Business Development Companies (BDC), which lend to small and medium-sized businesses, are currently trading at about 0.73 times their net asset value.

BDCs are currently trading at about 0.73 times their net asset value — such a discount has not been seen since 2020. Source: MorningStar J Guilford

Discounts have reached their peak since 2020, indicating that investors are already reducing risks.

Unexpected decisions from the Fed and the influence of AI on the lending market

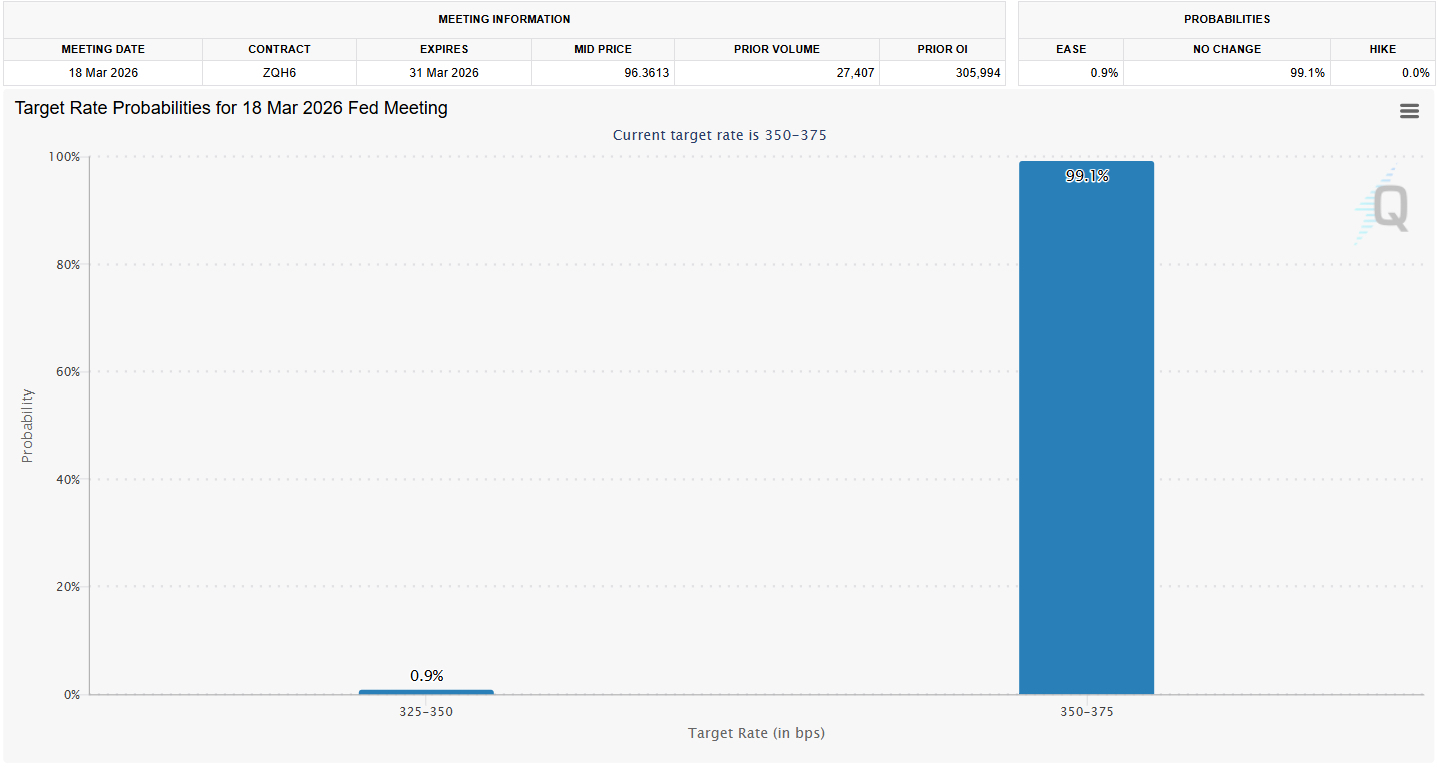

CME FedWatch Tool estimates the probability of maintaining the Fed's rate at 3.50–3.75% next week at over 99%. Such a scenario is already priced in.

Probabilities of changes in the Fed's rate. Source: CME FedWatch Tool

Probabilities of changes in the Fed's rate. Source: CME FedWatch Tool

For the crypto market, the tone of the speech will be critical. Any hawkish statements from Fed Chair Jerome Powell could amplify the already initiated process of risk aversion in the credit market and push bitcoin down.

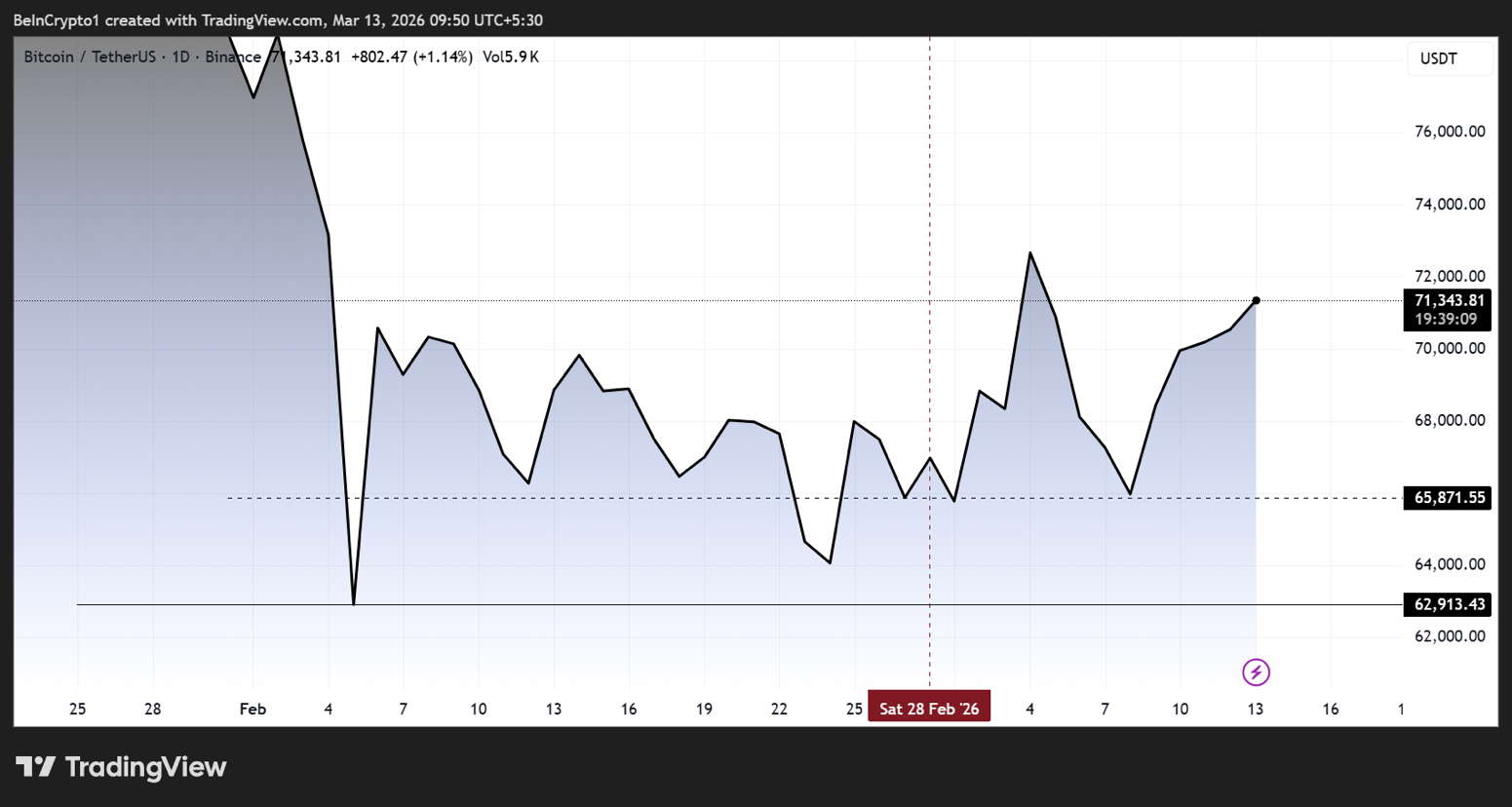

After the January Fed meeting, when the rate remained unchanged, bitcoin fell from $90,400 to $83,383 in 48 hours. If the situation repeats itself, and pressure on private credit continues, the support level at $62,300 will come under serious pressure.

Bitcoin price dynamics. Source: TradingView

Bitcoin price dynamics. Source: TradingView

Tension arises not only from requests for withdrawals. This week, Deutsche Bank reported that its portfolio of private loans grew to €25.9 billion ($30 billion), which is 6% more than in 2024.

Lending to technology companies increased by more than a third — to €15.8 billion ($18.3 billion), with a significant portion issued to software developers who are now under threat due to the development of AI.

Additionally, Deutsche Bank financed the construction of data centers worth billions of euros, and one of the top managers noted that the bank's investment division is betting on the development of artificial intelligence infrastructure.

As a result, a two-way risk is forming for markets related to the crypto industry: old loans to software developers may suffer due to competition with AI, while new lending for artificial intelligence may form a separate bubble.

Open interest in put options on the largest American credit ETFs, such as HYG, JNK, and LQD, reached a record 11.5 million contracts. Over the year, this figure has doubled and already exceeded levels from 2022. Spreads on high-yield credits in the technology sector have widened to 556 basis points — 195 points more compared to the broader high-yield bond market. Such metrics show how actively institutional investors are hedging against a crisis in the credit market.

The main intrigue for the crypto market next week is whether the market will be limited to a local pullback amid another Fed decision on the principle of 'sell the fact', or if there will be a mass exit from risky assets due to pressure from credit investors.

If the Fed opts for a wait-and-see tactic, and pressure on private credit continues, bitcoin may face a liquidity shortage from both sides.

\u003ct-99/\u003e\u003ct-100/\u003e