95% of revenue depends on interest income, the Federal Reserve is still lowering interest rates, why did Circle's stock price surge by 20%? The answer is not in the profit statement: the market is not pricing the interest differential, but rather the cross-border settlement network and fee rights built around USDC. Whoever controls the standards and settlement rights of the channel between fiat currency and on-chain dollars can collect tolls; what Circle is betting on is this matter.

On February 25, 2026, Circle (NYSE: CRCL) released its financial report for the fourth quarter and the whole year of 2025: Q4 revenue was $770 million, of which about 95% came from reserve interest; annual revenue was $2.7 billion, a year-on-year increase of 64%. At the end of the year, the circulation of USDC was $75.3 billion, and Q4 on-chain transaction volume was $11.9 trillion. After the financial report was released, the stock price initially rose nearly 20% in pre-market trading.

Breaking it down, Circle's revenue essence is:

User dollars → Buy US Treasuries → Earn interest.

The financial report disclosed that the growth of reserve income in Q4 mainly came from the doubling of average USDC circulation, partially offset by the decline in reserve yield, meaning growth relied on scale expansion rather than single-coin yield enhancement. From the reserve composition, Circle's USDC reserves are highly concentrated in highly liquid dollar assets, with over 70% related to U.S. government instruments (such as Treasury repurchase agreements, Treasury securities, etc.).

Essentially, what Circle is doing is similar to large money market funds: using on-chain dollars to allocate equivalent fiat currency into short-term U.S. Treasuries and cash-like assets, earning the spread between reserve yields and user zero-interest holdings. If it were just a 'U.S. Treasury agent' (issuing USDC, investing reserves in Treasuries, relying on interest spreads), under the Federal Reserve's entry into a rate-cutting cycle, with a declining interest rate center and compressed reserve yields, the future income curve is likely to trend downward, and it would be difficult to support the current valuation based solely on this.

Therefore, stock prices reflect not only current profits but also the market's expectations for Circle's stablecoin payment network and the toll fees it will earn. Management has repeatedly emphasized in financial reports and public occasions the shift from earning interest spreads to infrastructures like the Arc blockchain and Circle Payments Network (CPN), and has provided a guidance of $150–170 million in non-interest income for FY 2026, which implies to the market that the bigger business in the future will be earning gas fees and network usage fees, rather than interest spreads. This road has already rewritten bank settlements in some scenarios: a global payment network based on stablecoins is beginning to replace or supplement traditional banks and SWIFT/agents. The following will first look at where it has taken over the traditional settlement tasks, and then explain what this infrastructure is, how it operates, and who the pricing rights might ultimately fall to.

SWIFT is not dead, but this new road has already been nibbling away at its market.

Traditional cross-border payments rely on the SWIFT messaging + agent bank clearing system: the paying bank sends messages to the agent bank via SWIFT, which then transfers through multiple levels of agent networks before completing the crediting, during which several structural issues exist.

Delay: It often takes several days from initiation to receipt, with weekends and holidays extending the timeframe.

Cost: Each time you go through an intermediary, there is a layer of fees, plus implicit currency exchange markups, the overall cost of cross-border remittances can reach several percentage points.

Time is uncontrollable: unable to settle 24/7, which is unfriendly to businesses and individuals needing real-time fund aggregation or urgent payments.

Opacity and lack of traceability: funds circulate between multiple bank ledgers, and the end-to-end status is opaque. These pain points are repeatedly amplified in scenarios such as cross-border B2B, remittances, corporate fund aggregation, subscriptions, and payroll disbursements.

Stablecoins unify information and settlement. Funds move on the blockchain and settlement is completed: atomic settlement, with no intermediate state where funds are deducted but not received by the other party. Settlement is nearly real-time (depending on the chain's confirmation time, which can range from seconds to minutes), costs are extremely low (mainly on-chain gas fees), and can operate 24/7. Therefore, in regions with cross-border, B2B, high time sensitivity, high cost sensitivity, and inadequate coverage by traditional bank services, stablecoins have effectively replaced or supplemented traditional bank settlements. SWIFT is not dead, but stablecoins are already nibbling away at its market.

Data can testify. Circle disclosed that since 2018, USDC has facilitated over $28 trillion in cumulative on-chain settlements; by 2025, the scale of stablecoin on-chain settlements is expected to be in the hundreds of trillions, comparable to the payment settlement systems of major sovereign nations. Traditional giants are already connecting: Visa has allowed U.S. issuing banks and acquiring banks to use USDC for settlements with Visa, achieving continuous settlements outside of bank closing hours, with annual stablecoin settlement volumes reaching tens of billions. The practice of replacing SWIFT has already scaled: platforms like Conduit process about $10 billion in cross-border funds annually, covering over 130 markets, using compliance and bank collaborations for B2B and remittances, proving that stablecoin payment networks are not merely concepts but scalable infrastructures. In regions like Latin America, stablecoin activities are highly tied to cross-border payments (about 71% are cross-border related), indicating that partial replacement is already occurring in reality.

It is important to emphasize that the replacement is partial. It is not an overnight substitution of all bank settlements, but rather first occurring in regions with cross-border, B2B, high time sensitivity, high cost sensitivity, and inadequate coverage by traditional banks; traditional banks and stablecoins will coexist in the long term, with shares and scenarios shifting back and forth. The speed of replacement depends on the maturity of stablecoin payment infrastructure, the willingness of traditional institutions to connect, and the regulatory recognition of stablecoin payment channels.

How to connect the money in the bank with the money on the chain?

Having stablecoins alone is not enough. Stablecoins are on-chain dollar certificates, but the vast majority of businesses and individuals still have their funds sitting in bank accounts in fiat form. To scale on-chain dollars into a global payment network, an old problem must be solved: how to seamlessly convert fiat in banks into on-chain stablecoins and complete payments. This requires a layer of payment infrastructure: capable of moving fiat onto the chain (turning into stablecoins), and moving on-chain stablecoins back to local fiat, while unifying compliance (KYC/AML, Travel Rule, sanction screening, etc.) and settlement standards. This infrastructure can be understood as consisting of two parts.

First part: Coordination layer: Toll booths, entrances, and logistics centers for fiat currency ↔ on-chain stablecoins.

In simple terms, the coordination layer is responsible for solving how to get fiat onto the chain and how to get it off: who exchanges fiat for stablecoins at what location, who exchanges stablecoins back to fiat at what location, how to reconcile in-between, and how to meet regulatory requirements in different countries. A typical representative is the Circle Payments Network (CPN). CPN does not directly manage user funds but connects banks and payment institutions from various countries into a network through API: one end is the initiating institution that helps customers collect fiat and exchange it for USDC and other stablecoins, while the other end is the receiving institution that receives stablecoins, exchanges them for local fiat, and deposits them into bank accounts or wallets. Settlement is completed nearly in real-time on a public chain, operating 24/7, and includes compliance checks and other enterprise-level features. Those who want to use compliant fiat ↔ stablecoin channels or want to access 24/7 stablecoin settlements must connect through networks like CPN. Therefore, CPN is more like the toll booth and entrance on this road: it does not issue coins but determines who can get on and off where.

Second part: Settlement chain: A dedicated track for stablecoins.

The coordination layer solves entry and exit, while the settlement chain addresses how to run faster, cheaper, and more predictably on the road. The gas fees of traditional public chains (like the Ethereum mainnet) are priced in native tokens, with large price fluctuations and slow confirmations, which are not friendly for payments. The dedicated settlement chain for stablecoins treats stablecoins themselves as gas or core assets, achieving low rates, stable pricing, and second-level confirmations, making it more suitable for large-scale payments and settlements. Circle's Arc and Tether's Stable and Plasma are essentially paving a highway specifically for USDC/USDT: allowing funds to run on-chain while being both cost-effective and predictable, while transforming gas fees into a business line independent of interest spreads. The coordination layer is responsible for entrances and exits, while the settlement chain handles the tracks; only by combining both can stablecoins have the opportunity to evolve from mere assets into the infrastructure of a global payment network.

A payment network covering multiple countries.

Based on this infrastructure, the global payment network of stablecoins is already running, rather than just written in white papers.

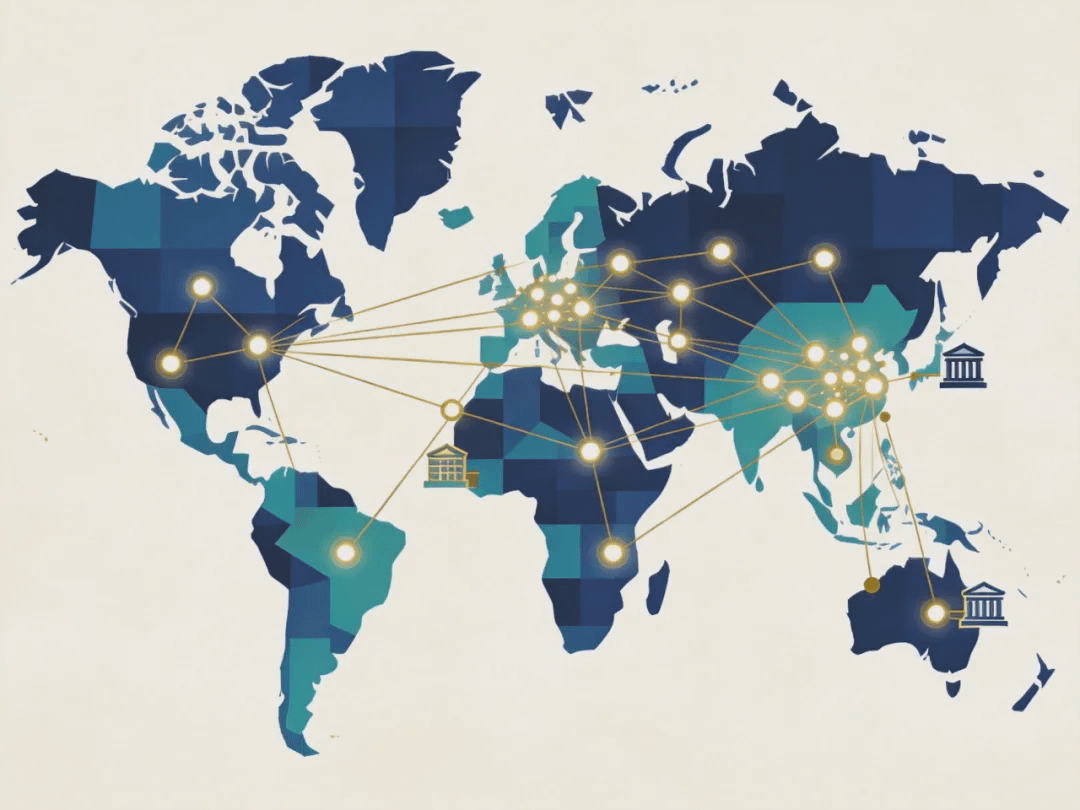

The corridor is expanding. Through CPN, Brazil, China, Colombia, Hong Kong, Nigeria, and some Latin American markets have already connected local fiat currency, the next step will extend to India, the Philippines, Singapore, the UAE, Europe, and other places. For financial institutions, only a unified API and protocol are needed to facilitate multi-country fiat currency entry and exit, without having to find a separate local payment provider for each country. Product capabilities are also advancing: RFI, automatic corrections, Travel Rule pre-checks, self-service Consoles, and subsequent native integration with Arc, moving more payment processes on-chain, creating a closed loop for entrances and tracks.

Scale and cases are speaking. USDC's cumulative on-chain settlement has exceeded $28 trillion, Visa uses USDC to settle with partner banks, and Conduit processes about $10 billion in cross-border funds annually; institutions like Alfred Pay, Tazapay, RedotPay, and Conduit have already been running real transactions on CPN. These data indicate that a payment network covering multiple countries has taken shape: coordination layer + settlement chain is transforming cross-border payments between fiat currency, stablecoins, and fiat currency into a repeatable infrastructure.

Circle and Tether are competing for the same road.

Who is paving this road? Circle and Tether are competing for the same one: the payment infrastructure between fiat currency and on-chain dollars. The focus of competition is no longer on who has more coins or higher interest rates, but on who stabilizes their position in the payment and settlement infrastructure first; they can earn tolls and gas fees long-term beyond interest spreads.

Circle: Using CPN (coordination layer) + Arc (settlement chain) to build a network that is onshore, compliant, and oriented towards institutions and banks, connecting companies, financial institutions, and banks from various countries through API, using USDC as the underlying track for cross-border settlements and payments.

Tether: Using Stable + Plasma to create an offshore, multi-chain dedicated chain for stablecoins, turning USDT into universal fuel for cross-border payments, e-commerce, DeFi, and institutional fund flows.

The differences between the two companies lie in compliance routes, service targets, and coverage areas, but the common point is that both regard payment infrastructure as the main battlefield for the next phase. The reason is straightforward: today’s issuers still primarily rely on reserve interest, and the Federal Reserve's interest rate cuts will compress this part of the space; while toll fees, gas fees, and network usage fees are linked to network scale and transaction volume, not directly governed by interest rate cycles. Whoever paves this road first will have an additional business line that can make money long-term without relying on interest spreads.

Endgame: Whoever paves this road has a ticket to the future.

The payment infrastructure of stablecoins is key to building a global payment network, partially replacing traditional bank settlements. On this infrastructure, stablecoins are forming a global payment network, and in scenarios such as cross-border, B2B, and 24/7, they are partially replacing traditional banks and SWIFT/agents. Whoever operates this infrastructure has the pricing power and network effects of toll booths, entrances, and logistics centers: toll fees, gas fees, API and compliance service fees will concentrate to the operator.

Observable signals include: whether the corridor continues to expand, whether traditional giants like Visa/banks are increasing access, whether Circle's income from on-chain sources is rising, Tether's on-chain income from Stable/Plasma and ecosystem scale, and the regulatory recognition of stablecoin payment channels. For ordinary businesses and individuals, this directly relates to the future costs, speeds, and predictability of cross-border payments and remittances.

The endgame of stablecoins is not just about who issues more, but rather who first repairs the payment highway between fiat currency and on-chain dollars, and stands at the toll booth.