The market value of USDT today exceeds $186 billion, accounting for about 62% of the total market value of stablecoins. The on-chain settlement volume for the entire year of 2025 is approximately $13.3 trillion, making it the largest and most widely used 'on-chain dollar' at present.

From a business model perspective, Tether connects the issuance, redemption, and reserve management of USDT on one end, and large-scale dollar asset allocation and earning interest rate spreads on the other. In 2025, the net profit is expected to exceed $10 billion, with exposure to U.S. Treasuries and related assets of approximately $141 billion, ranking among the top global institutions holding U.S. Treasuries. The reserves also include billions of dollars in physical gold, which has contributed significant paper gains against the backdrop of strong gold price increases in recent years. It serves as both an 'on-chain central bank' providing base currency for the entire industry and a highly profitable dollar asset management bank, with the principal mainly coming from users' almost interest-free liabilities, while most interest income remains on its own books. A rough estimate using traditional banking valuation methods suggests that such profits and asset scale are sufficient to benchmark against a number of leading global financial institutions.

It is precisely because this is one of the few, highly closed-loop profit-making machines in the blockchain industry that USDT is often referred to as 'the best business model' and 'a commercial miracle.' This history is worth sorting out because it directly relates to three questions:

Why must stablecoins inevitably emerge?

How did USDT grow into infrastructure amidst controversy?

Where does the trust in on-chain USD come from, and what are its boundaries?

Next, we will respond step by step to the three questions above from the perspectives of how demand has grown, how USDT has been forced to evolve into its current form under real constraints, and its position within the trust structure and global payment system.

1. Origin: Why does blockchain need stablecoins?

USDT did not appear out of thin air, but as a response to a type of rigid demand. Without clarifying the demand, one cannot understand its birth impetus, its explosion during the bank cut-off, and its deep binding with 'exchange-market maker-multi-chain.'

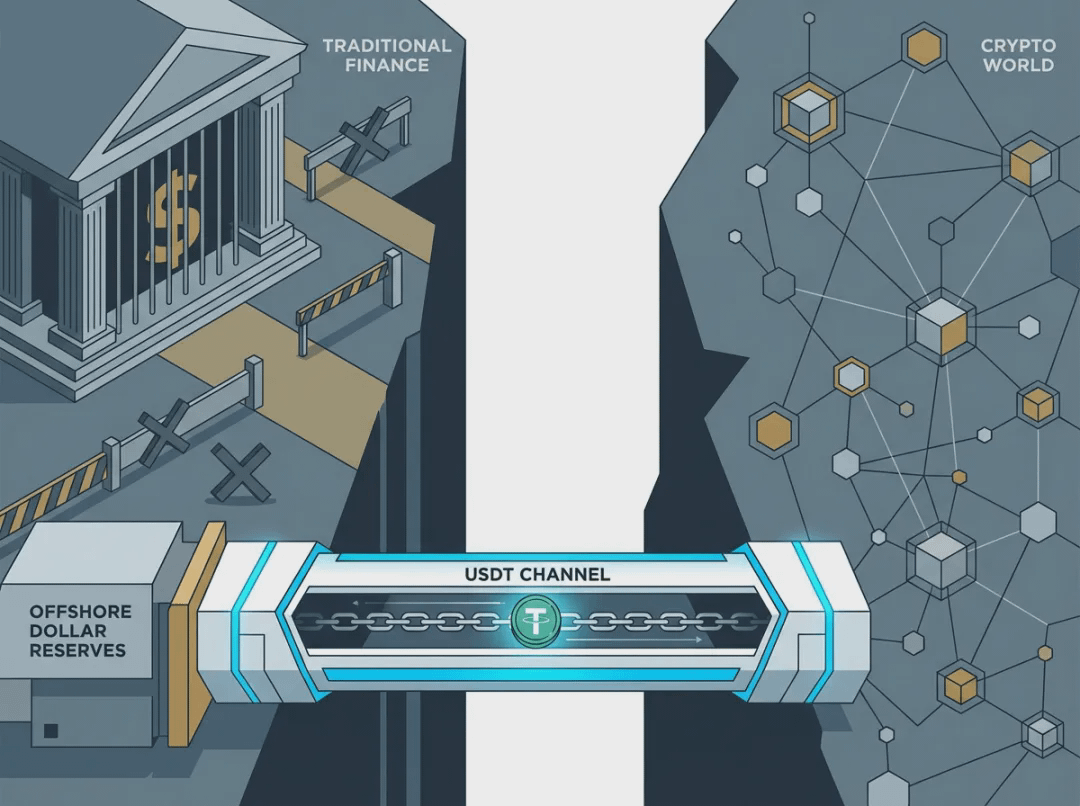

From the perspective of currency functions, Bitcoin and most crypto assets exhibit extreme price volatility, making them unable to serve as a measure of value and pricing unit. If the on-chain economy only has volatile assets, it cannot form stable pricing, lending, settlement, and long-term contracts. Stablecoins complete this monetary loop: they are the stable anchor for pricing, settlement, and storage in the crypto economy; without stablecoins, the blockchain economy cannot have real pricing. Meanwhile, global cryptocurrency exchanges (especially offshore and non-U.S. licensed institutions) have long faced fragile fiat channels: inflows and outflows depend on a few banks and agents, and once cut off, everything comes to a halt. This creates a rigid demand for a USD equivalent on-chain, capable of 24/7 circulation, cross-exchange arbitrage, and substituting frozen fiat channels when banks are unwilling or unable to serve.

The pricing gap and the breakdown of fiat channels overlapped, providing leverage for the birth and subsequent explosion of USDT. Next, let's look at how this demand was turned into products and architecture, and why it is referred to as a 'commercial miracle.'

2. Birth: The launch of USDT

Around 2014, offshore exchanges (represented by Bitfinex) had already become important liquidity nodes globally, but fiat currency inflows relied heavily on banks in places like Taiwan for USD wire transfers; if a bank or intermediary cut the line, user deposits and withdrawals would stop, directly crippling the exchange's business. The initial idea of Realcoin (later renamed Tether) was to create a USD-pegged asset on-chain to satisfy the need for a 'USD-denominated tool in the crypto world'; only after being tied to Bitfinex and exposing bank channel issues did it truly become a tool to resolve this pain point. Tether Holdings Limited is registered in the British Virgin Islands, and Bitfinex executives are co-founders, both part of the iFinex system. Bitfinex became the first application scenario and main outlet for USDT: exchanges needed stablecoins to solve fiat channel issues, and Tether needed exchanges for distribution and flow back, forming a closed loop. The first USDT was minted on Omni (Bitcoin layer) in 2014, and in 2015, Bitfinex officially supported USDT deposits, withdrawals, and trading, transforming USDT from an experimental product into a usable tool. The early design was clear: 1 USDT = 1 USD, promising a 1:1 reserve, redeemable at any time; the technical carrier was Omni Layer, which was slow to confirm and had high fees; the main distribution targets were institutions and large holders exchanging fiat ↔ USDT through Bitfinex, with circulation in the millions to tens of millions of dollars.

In an era when traditional banks generally do not serve the crypto industry, on-chain tokens and offshore reserves have forcefully rebuilt a 'USD channel'; it follows the path of first meeting real needs, then iterating in controversy, rather than obtaining regulatory approval before taking action. Understanding this starting point helps explain why the suspension of fiat channels leads to USDT's explosion and why it can be pulled back after decoupling.

3. Growth and constraints: What do the four phases answer?

With this starting point, the next decade can basically be seen as a process of USDT repeatedly 'refining' this demand under various real constraints. Below, we will break this down into four phases: can it survive, can it replace fiat channels, can it exist under regulation and transparency, and can it become the global settlement layer.

Phase 1 (2014–2016): Can we survive?

At this stage, USDT primarily validated the concept with limited circulation. In 2016, Bitfinex suffered a hack, losing about 119,700 BTC, imposing a roughly 36% 'haircut' on users and issuing BFX debt-to-equity tokens for accounting and compensation; this crisis primarily relied on BFX to back it up, not USDT, but from that moment on, external parties began seriously questioning the financial boundaries and reserve independence of Tether and Bitfinex. That year, Tether launched EURT, expanding its product line from 'only USD'. The outcome of this phase was: USDT survived but with limited scale; externally, it only stated '100% USD reserves,' with no third-party audits and no disclosure of asset composition, relying almost entirely on Bitfinex for distribution. Trust was entirely based on 'commitment + single outlet'; if banks cut off channels or reserves were questioned, the peg would be the first to fall. In fact, the next phase was triggered in this way.

Phase 2 (2017–2018): Can we replace fiat channels?

In 2017, Wells Fargo cut off Bitfinex's USD wire transfers through multiple banks in Taiwan, leaving about $180 million in client funds unable to be normally deposited or withdrawn. After the fiat channel broke down, USDT transitioned from an optional choice to a de facto alternative USD channel: users and market makers rapidly shifted to using USDT for on-chain transfers and cross-exchange arbitrage, with circulation quickly climbing from tens of millions to over $2.2 billion by the end of 2017. The New York Attorney General (NYAG) later disclosed that Tether had only about $61.5 million in cash held by lawyers, which created a gap with the issued USDT amount, leading to long-standing questions of 'insufficient reserves.' In the same year, the ERC-20 version of USDT launched on Ethereum, allowing entry into smart contracts and DeFi; later, Tether's treasury was hacked, resulting in over $30 million in stolen USDT. Tether introduced freezing capabilities through an Omni hard fork, creating a precedent for 'freezable' centralized stablecoins. In 2018, Tether and auditor Friedman ended their cooperation, leading to years without a complete audit; subsequently, the TRC-20 USDT was launched; Tether established a relationship with Bahamas' Deltec Bank, disclosing over $1.8 billion in reserves, temporarily alleviating the public pressure of 'no bank,' but Bitfinex withdrew hundreds of millions from Tether's Deltec account, once again putting their financial transactions under regulatory scrutiny. The cut-off of fiat channels forced the industry to use USDT as a substitute, leading to an explosive demand; multi-chain and freezing mechanisms were implemented, but reserve transparency and audit issues became long-term themes, setting the stage for several serious decouplings that followed. The upcoming challenge became: regulation and transparency.

Phase 3 (2019–2021): Can we continue to exist under regulatory and transparency pressures?

In 2019, Tether modified its service terms and website statements: from 'each 1 USDT is backed by traditional currency 1:1' to '100% backed by reserves, which may include cash equivalents, other assets, and loans to third parties (including related parties),' opening legal space for reserve diversification and related party transactions. NYAG accused Bitfinex and Tether of concealing losses and commingling funds, using Tether reserves to fill Bitfinex's approximately $850 million gap (related to Crypto Capital), issuing an investigation and injunction. In 2021, Bitfinex/Tether reached a settlement with NYAG: paying a $18.5 million fine, ceasing to offer USDT trading to New York users, etc., without admitting wrongdoing. Tether first disclosed its reserve composition: commercial paper accounted for the majority (about 65.39%), with cash and bank deposits, U.S. Treasuries, reverse repos, etc., making up the rest, marking the first time the industry saw that USDT's backing was not entirely 'bank deposits.' The U.S. CFTC fined Tether $41 million for previously falsely claiming USDT was fully backed by USD. Reserves shifted from 'verbal 1:1 cash' to 'written cash equivalents + commercial paper + others'; regulation concluded with fines and settlements, while USDT's scale continued to expand (by 2020, circulation had exceeded 14 billion units). Under transparency and regulatory pressure, the path taken was one of 'iteration,' not 'exit.'

Phase 4 (2022 to present): Can it become the default global settlement layer?

In 2022, Tether fully cleared commercial paper, replacing about $30 billion with U.S. Treasuries and others, with reserves over 81% being cash and cash equivalents, and exposure to U.S. Treasuries exceeding $39 billion; it introduced third parties like BDO for quarterly verification and established excess reserves (approximately $6.3 billion by the end of 2025), forming 'strength-based trust.' From 2023 to the end of 2025, USDT's market value surpassed $100 billion, $150 billion, and by the end of 2025, it was approximately $186 billion, accounting for about 62% of the total market value of stablecoins; daily settlement volumes often reached the hundreds of billions, handling approximately $13.3 trillion in transactions for the year; multi-chain became the default 'on-chain dollar,' widely adopted in cross-border trade and remittances in BRICS and emerging markets. Reserves shifted from high-yield, high-controversy commercial paper to low-risk, high-liquidity Treasuries and cash equivalents; distribution expanded from a few exchanges and market makers to a global multi-chain, multi-scenario (CeFi + DeFi + payments); USDT evolved from 'growing up in controversy' to 'volume equals trust' as the global settlement layer.

The entire narrative can be summarized as: demand drives form, form invites questioning, questioning pushes for transparency and conservatism, and transparency and conservatism in turn support scale and trust. Reserves and distribution are the two most sensitive lines in this narrative, meriting separate examination regarding where trust comes from and at which nodes it is questioned and reconstructed.

4. The two legs of trust: the evolution of reserves and distribution.

Reserves answer 'is there money for redemption', distribution answers 'who gets USDT and how, and how is risk spread'; only when the two are combined can the boundaries of trust be drawn. Here we mainly discuss how trust is built, questioned, and then reconstructed.

The evolution of reserves is a clear trajectory.

Initially (2014–2016): The external statement was '100% USD reserves,' with no third-party audits, no asset composition disclosed, and blurred boundaries with Bitfinex's funds.

2017–2018: NYAG revealed that only about $61.5 million in cash was held by lawyers, which created a gap with the circulating amount at that time; later partnered with Deltec, disclosing over $1.8 billion in account balances in 2018, still without asset composition disclosure.

In 2019, the terms were changed to allow reserves to include cash equivalents, other assets, and loans to third parties (including related parties).

In 2021, the first reserve composition was disclosed, with commercial paper making up the highest percentage (about 65%+), raising industry concerns about liquidity and transparency.

By 2022, commercial paper was cleared, reserves shifted to U.S. Treasuries, money market funds, reverse repos, and a very small amount of cash; by the end of 2022, approximately 81%+ of the reserves were cash and cash equivalents, with exposure to U.S. Treasuries exceeding $39 billion.

According to BDO verification from 2025 to 2026: U.S. Treasuries account for about 82%, money market funds about 10%, reverse repos about 5%, and cash about 0.5%; additionally, allocations include Bitcoin (about $9.9 billion), gold (about $12.9 billion), etc., with gold positions also becoming a profit source during the recent gold price increase cycle; excess reserves are about $6.3 billion, with a reserve ratio above 100%. Each change has been accompanied by controversy or regulatory pressure, ultimately converging into a conservative allocation dominated by safe assets. Trust has thus shifted from 'commitment' to 'verifiable asset composition + excess buffer'; as we will see when discussing decoupling, once reserves are verifiable and redemptions are inspectable, decouplings tend to be temporary and reversible.

The evolution of distribution is the process of 'who gets USDT, how they get it' evolving from a single outlet to multiple chains and scenarios.

Early (2015–2016): Mainly through Bitfinex, deposit USD → mint USDT on Omni → issue to users, redemption is the reverse; the issuance mechanism is still in use today, following four phases: Authorized → Issued (only counted in circulation upon receipt of fiat or equivalent collateral) → Redeemed → Destroyed, institutionally avoiding reserve-less issuance.

After 2017, ERC-20 and TRC-20 were launched, expanding distribution chains to Ethereum and Tron; market makers and exchanges bulk-purchased USDT from Tether, then provided liquidity to retail and DeFi, shifting distribution targets from 'centered on Bitfinex' to 'multiple exchanges + multiple market makers + multiple chains.'

After 2020, DeFi exploded, and USDT entered the on-chain ecosystem through liquidity pools, lending, and cross-chain bridges; Tether continued to expand across multiple chains, with distribution logic evolving into multi-chain, multiple entry points, and multiple scenarios.

Currently, official support extends to over 15 chains, with approximately 78% of on-chain transfers using TRC-20 and about 3% using ERC-20. Behind this is actually a typical 'chains and stablecoins mutually benefitting' scenario: USDT brought real payment and transfer needs to Tron, turning a public chain originally focused on performance into the busiest 'USDT route' globally; Tron then used low fees and high concurrency to push USDT from the exchange's internal market to cross-border remittances, small payments, and C-end wallets, which in turn heightened USDT's appeal to other chains and assets. Functionally, Tether connects issuance, redemption, and reserve management, resembling a 'central bank' in the blockchain industry; yet it also has to manage asset allocation, earn interest differentials, and cater to large clients, carrying a strong commercial bank flavor, which is one reason for its importance and controversy in distribution and trust structure. Trust derives not only from reserves but also from 'whether USDT can be accessed and redeemed on any chain and in any scenario when needed'; the networked distribution not only scales up but also brings liquidity distribution and centralized freezing to the forefront of trust discussions. Reserves and distribution together support 'strength-based trust', which is also why decoupling may be triggered under certain conditions.

This leads us to the next part: challenges and decoupling, testing where the boundaries of trust are.

5. Challenges and decoupling: Testing the boundaries of trust.

Audits, banks, regulation, and external shocks put pressure on USDT, combined with several serious decouplings, marking the 'boundaries of trust': under what circumstances will the market and regulators question the peg, and under what circumstances will they accept its restoration? The question is why there has not yet been an irreversible run on the bank, and what the realistic boundary of 'fiat reserve-based' trust is.

Audits, banks, and regulation are three ongoing pressure lines. Regarding reserve transparency and audits: early on, there were no complete audits, only lawyer custodians or account snapshots; after parting ways with Friedman, there were years without audits; starting in 2022, BDO began quarterly verifications, and excess reserves were established, transitioning from 'controversy' to 'strength-based trust.' In terms of bank relations, Wells Fargo's cut-off (2017), and the termination of cooperation with Noble Bank alleviated but did not eliminate 'de-bankization' risks with the coexistence of Deltec and multiple banks in the offshore structure. On the regulatory and legal front, the NYAG investigation and the 2021 settlement, and the CFTC fines pushed for more transparency in terms and reserve disclosures. External shocks repeatedly validated the same issue: during exchange failures (like FTX) and the collapse of UST, USDT experienced several brief decouplings but was pulled back; market fear of non-reserve-based stablecoins deepened reliance on USDT and USDC, with several crises objectively consolidating the position of leading fiat reserve-based stablecoins.

Several serious decouplings occurred, each with different sources of pressure, but all directly marked trust boundaries.

In 2018: The lack of transparency in reserves, the breakup with Friedman, and strained bank relationships coincided, causing USDT on some exchanges to drop to about $0.87 or even around $0.50 against the dollar, marking the first large-scale decoupling; it did not lead to a systemic run, as Tether temporarily stabilized expectations by disclosing Deltec's reserves (over $1.8 billion that year). The underlying logic is simple: a lack of transparency in reserves and reliance on banks will directly impact the peg, prompting the market to 'demand visible reserves.'

2020: Under the impact of the pandemic, some exchanges briefly deviated from USDT's peg of 1 dollar, mostly driven by liquidity and sentiment, with limited amplitude and duration. This indicates that stablecoins will absorb short-term pricing pressure during extreme market conditions, but as long as their redemption ability is not questioned, the price will quickly return.

In 2022 (after FTX collapsed): After FTX's collapse, associated market makers heavily sold USDT in DeFi, causing some platforms to drop to about $0.93; Tether processed about $700 million in redemptions within days, with smooth redemptions, and the price quickly returned above $0.99. Whether it can stabilize during panic hinges on whether reserves are sufficient and whether redemptions keep pace; simultaneously, it also shows that once USDT's share in DeFi pools is disproportionately high, it will amplify short-term price discrepancies.

In 2023 (long-term weakness + freezing): DeFi liquidity from Curve and exchange supply and demand mixed together, causing USDT to remain below 1 dollar for a while, with most platforms at a discount; that year, Tether was required by U.S. law enforcement to freeze multiple USDT transactions (including approximately $225 million related to human trafficking and 'pig butchering' scams, accumulating approximately $435 million thereafter); once the freezing news broke, the market worried about 'centralized control' and liquidity, leading to a brief decoupling. It is evident that besides reserves and redemptions, liquidity distribution and centralized freezes can also emotionally impact the peg; after decoupling, everything recovered, indicating that the market still prioritizes 'effectiveness' over 'compliance/transparency.'

The triggers for decoupling are mostly due to questioning reserves, problems with banks/audits, failures in exchanges or DeFi, and significant freezes; recovery relies on redemption capabilities, reserve disclosures, and market-making arbitrage. Decoupling did not lead to irreversible runs; each recovery instead reinforced the perception that 'fiat reserve-based stablecoins can still be redeemed in crises,' contrasting with the collapse of algorithmic stablecoins like UST.

The realistic boundaries of trust are roughly: reserves must be verifiable, redemptions executable, liquidity distribution and centralized control partially accepted by the market; the stablecoin (3) - who to trust? The monetary order of USDT, USDC, DAI emphasizes 'effectiveness first' as a logical framework.

6. Ecological Impact: From Pricing Unit to Settlement Layer

The previous sections focused more on whether USDT can survive and maintain trust; this section shifts perspective to examine what specific changes it has brought to the industry, how it has evolved from a pricing unit within exchanges to the current global multi-chain, multi-scenario settlement layer.

In centralized exchanges, the vast majority of cryptocurrency transactions are priced and settled in USDT; about 74% of cryptocurrency transactions use stablecoin quotes, with USDT holding the largest share, and its liquidity depth supports price discovery and arbitrage in the global crypto market. In DeFi, USDT serves as an important collateral and benchmark asset across chains for lending, liquidity pools, and derivatives; although its share on DEXs is not as high as USDC, it still accounts for about 33% of stablecoin trading, making it a core part of the on-chain 'USD layer.' In regions with poor banking services and large fiat currency fluctuations (Latin America, Southeast Asia, Africa, etc.), USDT is used as a digital dollar: for remittances, trade settlements, and storage; stablecoin liquidity in Latin America and the Caribbean is about 7.7% relative to GDP, with approximately 71% of stablecoin activities and cross-border payments in Latin America related to USDT, which has already extended USD credit into on-chain and offshore scenarios.

These three elements together support the term 'settlement layer': pricing and quotes in CeFi, on-chain credit and liquidity in DeFi, and cross-border payments and storage. From the 'pricing unit of exchanges' to the 'global settlement layer', USDT has a tangible impact on the blockchain and payment landscape.

7. How do we understand this history today?

By the end of 2025, USDT's market value will be approximately $186 billion, accounting for about 62% of the total market value of stablecoins, with daily settlement volumes leading the way; official support extends to over 15 chains, with reserves primarily consisting of U.S. Treasuries (about 82%) and excess reserves of about $6.3 billion, with a reserve ratio above 100%. The numbers are results, but the key still goes back to the three questions at the beginning.

Why must stablecoins inevitably emerge? The on-chain economy needs a stable measure of value and a contractual pricing unit; exchanges and users need a USD channel that does not rely on single-point banks, which gives rise to the demand for stablecoins (1): the essence of currency and the inevitability of stablecoins speak to the same issue.

How did USDT grow into infrastructure amidst controversy? When banks cut off channels, it stepped up as a replacement; when reserve and regulatory pressures arose, it utilized flexible terms, transparent reserves, cleared commercial paper, and excess reserves to iteratively transform 'commitments' into 'verifiable conservative configurations'; several instances of decoupling validated its redemption capability, and crises instead strengthened trust in 'fiat reserve-based' models. Constraints and tests shaped its current form.

Where does the trust in 'on-chain USD' come from, and what are its boundaries? It comes from verifiable reserves, executable redemptions, and a distribution network with multiple chains and scenarios; the boundaries lie in reserve transparency, liquidity distribution, centralized freezing, and regulatory compliance. To this day, the market still prioritizes 'effectiveness' over 'compliance,' so USDT is not the most compliant, but it is the most 'effective' in terms of liquidity, network effects, and multi-chain coverage, which concludes the monetary order of stablecoins (3) - who to trust? USDT, USDC, and DAI.

The competition of stablecoins is essentially a competition of monetary trust models; from a business perspective, it is 'who can turn this trust model into a sustainable cash flow machine.' USDT's history demonstrates that in areas where real demand and institutional gaps coexist, first meeting the demand and then gradually building transparency and robustness under controversy and regulatory pressure is a path that has been successfully navigated by the market.

Reassessing this history, the significance lies not in remembering specific years and months, but in understanding how 'on-chain USD' grew from nothing to something, from the margins to infrastructure, and how USD credit continues to extend into the digital age through stablecoins; this matter is not over.