First of all, I am not bearish on $CRCL. I have also stated multiple times that CRCL is on my buying list; I just do not plan to buy CRCL at 80+ USD. Recently, I have been considering gradually rebuilding my position, which is the premise.

Many partners have seen Circle's financial report, and the answer provided for the fourth quarter is still quite good. Some partners even said that it is impressive for Circle to perform this well during a rate-cutting cycle. While this statement is not incorrect, it is not entirely correct either.

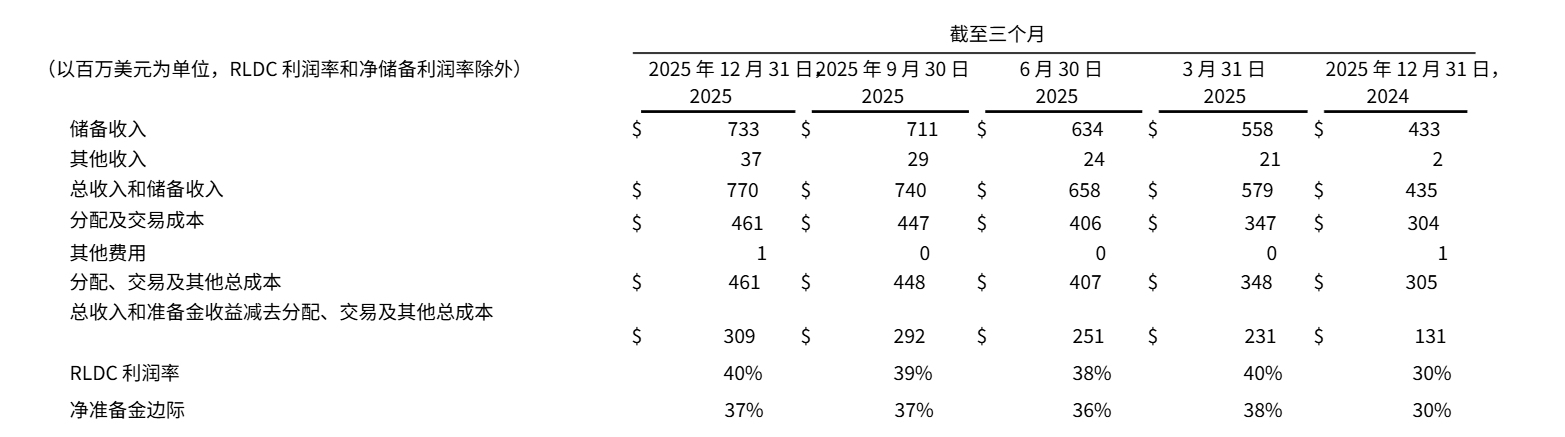

Indeed, Circle's fourth quarter financial report for 2025 shows a 77% increase in total revenue compared to the same period in 2024, reaching 770 million USD. The earnings per share (EPS) reached 0.43 USD, significantly exceeding market expectations, with a net profit of approximately 133 million USD, which is undoubtedly positive.

However, from the detailed data, Circle's achievement is not due to its business income or an increase in transaction fees, but rather the increase in interest, which comes from the increase in USDC issuance.

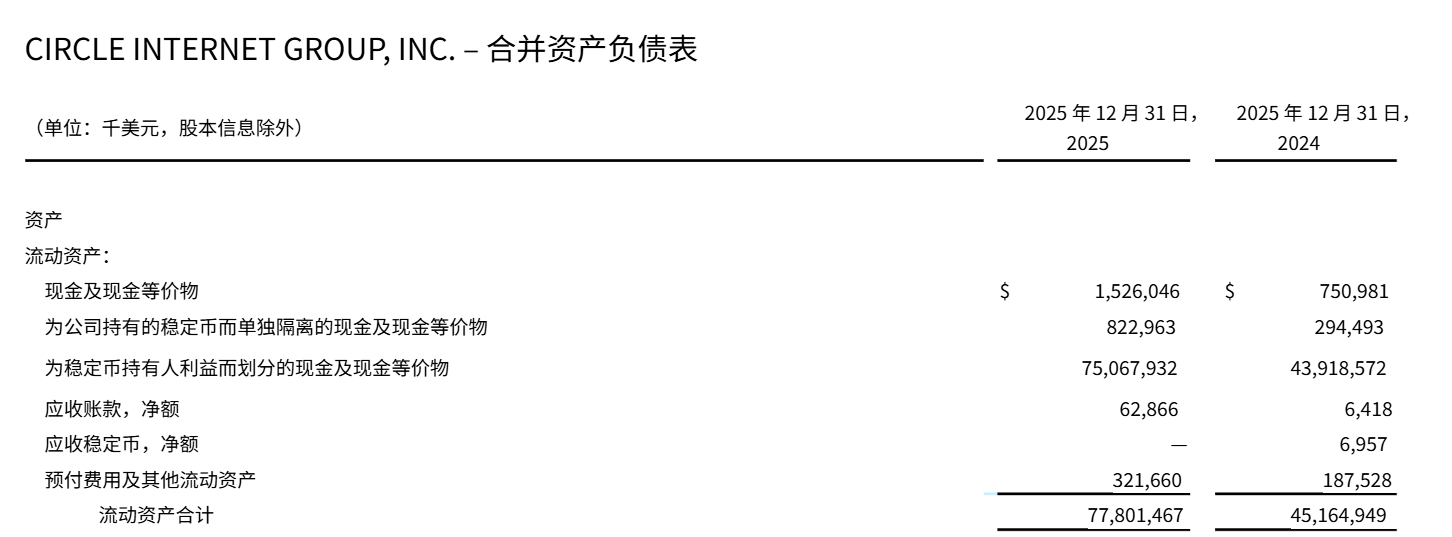

As of December 2024, Circle's total issuance of USDC is 43.92 billion dollars.

By December 2025, the total issuance of USDC had reached 75.49 billion U.S. dollars, with an increase of 71.88%.

Therefore, the main increase in $CRCL's revenue is attributed to the significant increase in the issuance of USDC, which leads to higher interest income.

The financial report clearly states that the main source of revenue comes from reserve income, and although other income from reserves is also increasing, by December 2025, other income is only 37 million dollars, merely 1/20 of reserve income. As is well known, even Circle itself admits that the decline in federal funds rate will directly impact revenue structure.

So when facing a rate-cutting cycle, if other income cannot see explosive growth, Circle will need to continue issuing a large amount of USDC to maintain good revenue expectations.

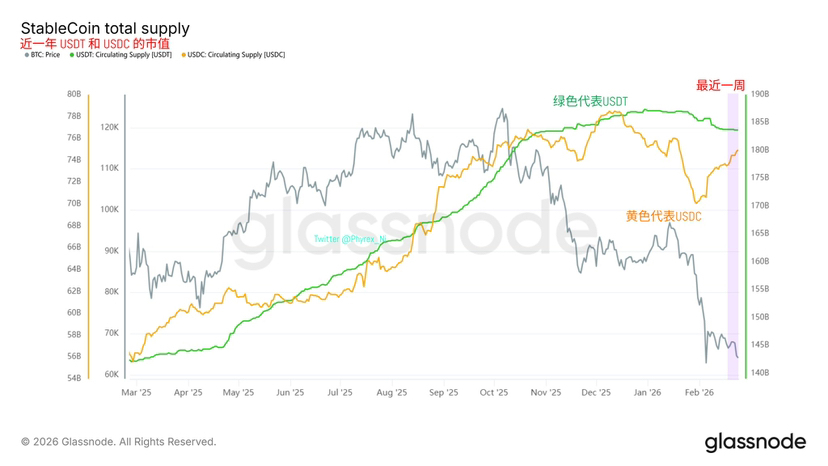

Recently, USDC's market capitalization has declined due to the sluggish cryptocurrency industry, but it is believed that as the market warms up, USDC's market will gradually rise. However, whether it can double again in about a month (during the first quarter 2026 financial report) seems very difficult. Moreover, once entering a substantial rapid rate-cutting cycle, the profitability per USDC will definitely be compressed.

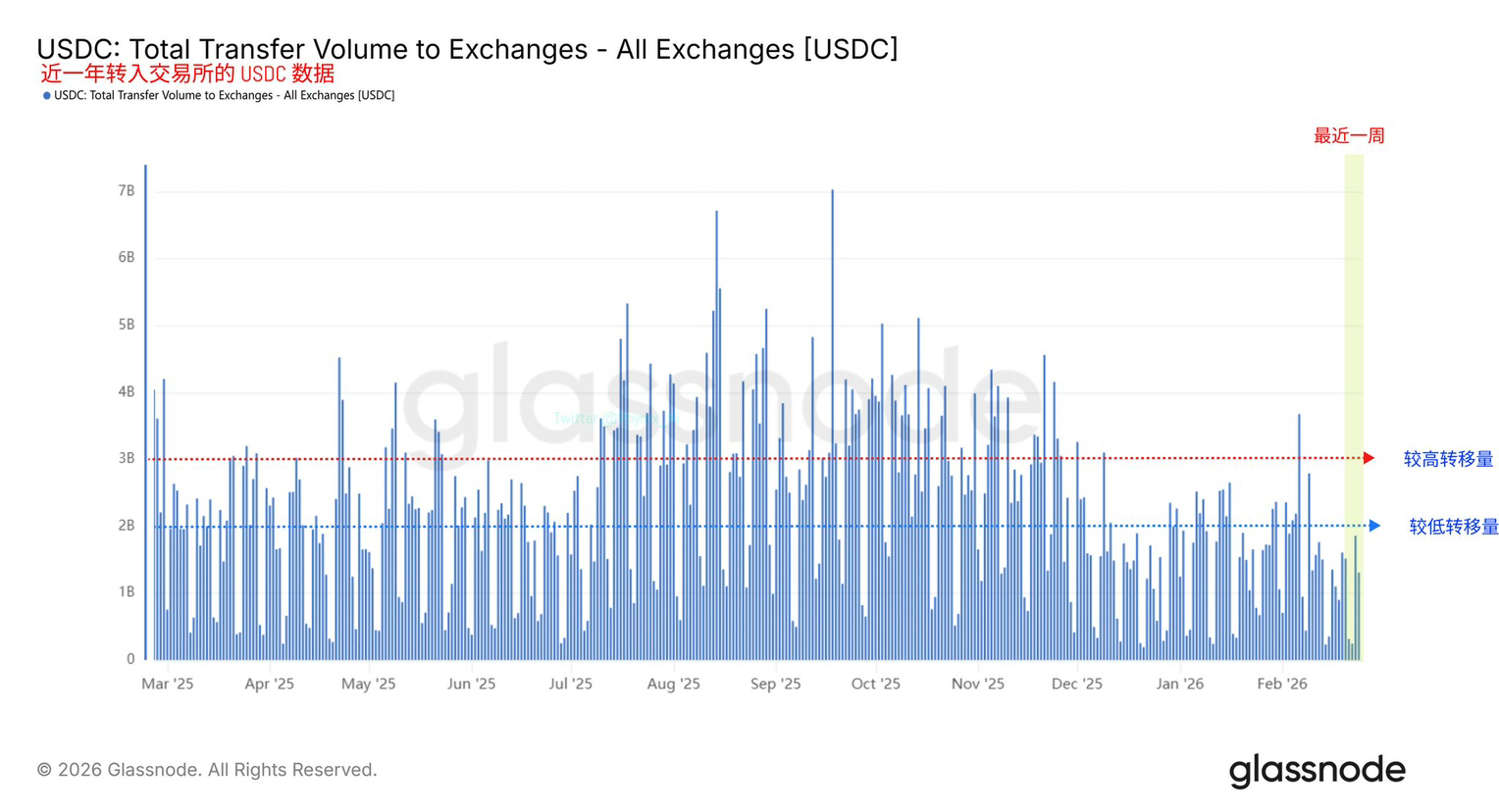

Of course, the rebound in USDC's market capitalization is also one of the reasons I am preparing to build positions. Funds are often seen as a leading indicator of the market, and the continuous recovery of USDC's market capitalization is likely preparing for investors to increase their bottom-fishing attempts, although there is currently no trend of these funds transferring to exchanges.

But I believe these newly issued USDC are either prepared to support transactions or to support payments. Regardless of which, it is beneficial for the development of $CRCL. Of course, when this benefit will materialize is uncertain, so starting to build positions with small amounts now may not be a mistake.

Additionally, it is important to note that Circle's distribution costs are very, very high, especially the fees paid to Coinbase. The financial report shows that in the fourth quarter of 2025, the 'total distribution, transaction, and other costs for CRCL amounted to 461 million dollars, an increase of 52% year-on-year, due to increased distribution payments,' and operating expenses have also reached 254 million dollars, a year-on-year increase of 95%.

High channel costs and operating costs are also one of the reasons limiting CRCL.

Of course, CRCL also performed well:

1. The Arc public testnet has launched, with over 100 participating parties, covering banking, capital markets, digital assets, payments, and technology sectors. Based on data from the past 30 days as of February 20, 2026, the average daily transaction volume is 2.3 million. Since the launch of the testnet, the total number of transactions has exceeded 166 million. Arc is scheduled to launch its mainnet this year.

2. Circle Payments Network (CPN) has expanded, with 55 financial institutions connected as of February 20, 2026, and another 74 undergoing qualification reviews. The annualized transaction volume is 5.7 billion dollars.

3. The circulating EURC at year-end was 310 million euros, a year-on-year increase of 284%, with a quarter-on-quarter increase of 44%. The USYC assets at year-end amounted to 1.5 billion dollars, a quarter-on-quarter increase of 111%.

4. Visa announced that U.S. issuing banks and acquiring banks can now use USDC to complete full settlements with Visa, enabling continuous settlements outside traditional banking hours.

5. Intuit has launched a multi-year strategic partnership to integrate USDC and Circle's supportive infrastructure into its platform.

6. Established a partnership with the world's largest prediction market, Polymarket, to promote the use of USDC as the core collateral and settlement asset in its market.

7. The Bermuda government announced plans to become the world's first fully on-chain national economy, supported by Circle's digital asset infrastructure.

8. In December, Circle received conditional approval from the Office of the Comptroller of the Currency to establish a national trust bank, further strengthening USDC infrastructure.

That's about it. Overall, $CRCL, as the first stock of U.S. stablecoins and currently the only one, still has imagination and potential. This strong financial report mainly relies on the increase in USDC's market capitalization, but maintaining such strength in the first quarter 2026 financial report or even in future reports will be very difficult.

Gradually starting to build positions, buying on dips should be considered by those with ample funds. Moreover, due to the currently low other income from CRCL, it has a significant correlation with the overall rise and fall of the cryptocurrency market. If the overall cryptocurrency market is not doing well, CRCL may find it difficult to rise independently.